Lana Stockman, Commissioner

Summer school in energy economics

Auckland University

Good morning everyone, and thank you very much for the opportunity to speak with you today.

Emil has already introduced me, but just briefly by way of context — I’m Lana Stockman, currently a Commissioner at the Australian Energy Market Commission.

I’ve worked across most parts of the energy sector in both Australia and New Zealand — wholesale trading, system operations, retail market development, regulatory policy, and increasingly the intersection between energy markets, technology change, and consumer outcomes.

I mention that background not as a CV exercise, but because it shapes how I think about energy policy. I’ve seen the sector from inside market operations, inside regulated businesses, and from the policy and governance side. And one consistent lesson from that experience is this — energy systems can be incredibly technical — but ultimately they exist for households and businesses.

If the system isn’t affordable, reliable and understandable to consumers, then we haven’t really succeeded.

So today I want to talk about how we think about 'price trends' in the context of the energy transition — not just electricity prices in isolation, but what the transition actually means for household energy costs, consumer decision‑making, and long‑term system confidence.

I am going to cover our Price Trends work — but instead of me speaking the entire time there will some opportunities for a brief discussion about key points.

Let me start with a bit of framing.

Historically, when regulators or market bodies talked about electricity price trends, we tended to unpack what people often call the “cost stack”. That means looking at network costs, wholesale energy costs, environmental policy costs, retail margins — essentially explaining which component of the system was pushing prices up or down.

That work served an important purpose. It improved transparency, helped policymakers understand cost drivers, and contributed to informed public debate. But over time, particularly as the energy transition accelerated, we realised something important.

Explaining price movements isn’t the same as helping people respond to them.

If a household hears that electricity prices are rising because of wholesale volatility, or network investment, that might be analytically correct — but it doesn’t necessarily give them a practical next step.

And when markets are undergoing structural change, short‑term price decomposition can actually miss bigger dynamics.

So we started reframing the work.

Instead of asking only, “What is happening to electricity prices?”, we began asking, “What will households actually spend on energy overall — and what choices influence that outcome?”

That shift sounds subtle, but it changes the entire conversation.

This is where the idea of the “household energy wallet” comes in.

Rather than focusing only on electricity bills, we look at the total energy spend for households. That includes electricity, gas where it’s still used, transport fuels like petrol, and increasingly the role of electrification — electric vehicles, electric appliances, rooftop solar, batteries, and demand‑side technologies.

Because from a household perspective, energy isn’t experienced in neat silos.

People don’t think:

“I’m optimising my electricity cost stack.”

They think:

“How much am I spending to keep the house warm, get to work, cook meals, and keep the lights on?”

And that broader lens leads to some quite different insights.

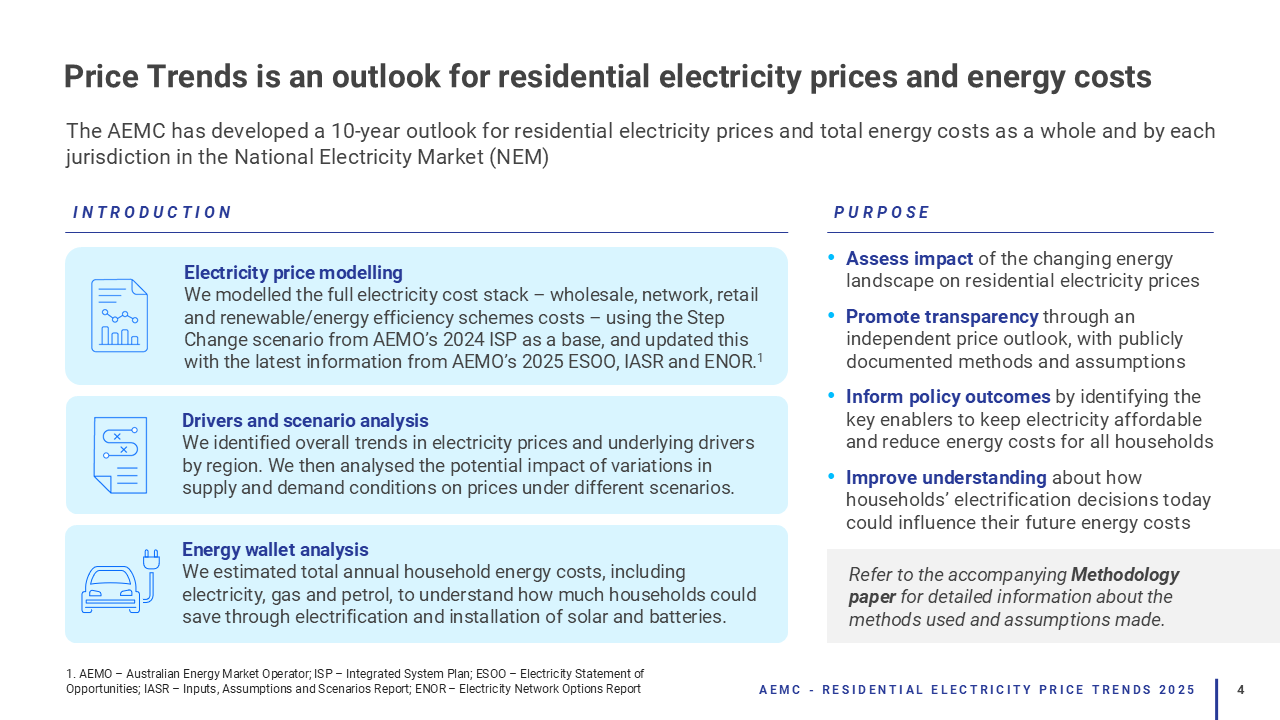

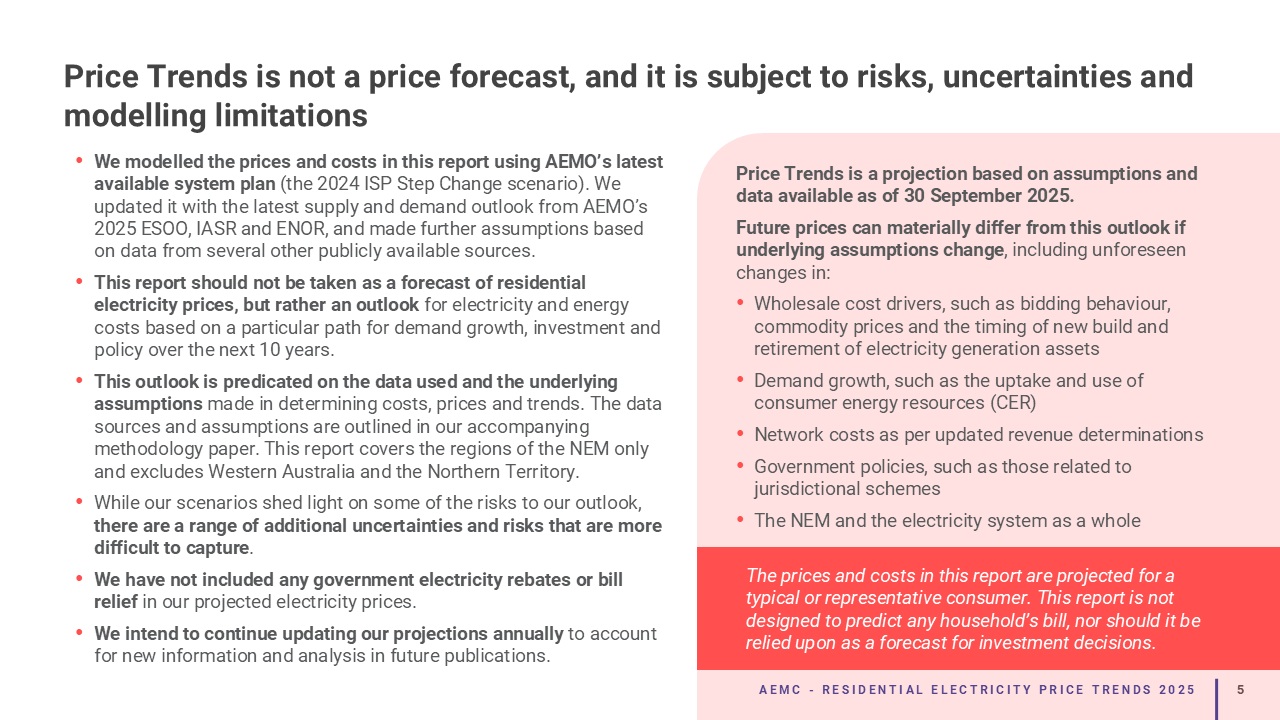

Before I go further, one important clarification — this work is not a point forecast.

We’re not trying to predict exactly what electricity prices will be in ten years. That would imply a level of certainty that simply doesn’t exist in a rapidly evolving energy system.

Instead, we use scenario analysis to explore plausible pathways. The goal is insight, not prediction. It’s about understanding drivers, trade‑offs and risks so policymakers, industry and consumers can make better decisions.

So what are we seeing?

One of the clearest themes is the importance of coordination across the energy transition.

Energy systems are deeply interconnected. Generation investment, network development, consumer technology uptake, market design, planning processes and policy frameworks all influence each other. When those pieces move together, the transition tends to be smoother and more affordable. When they don’t, cost pressures can emerge.

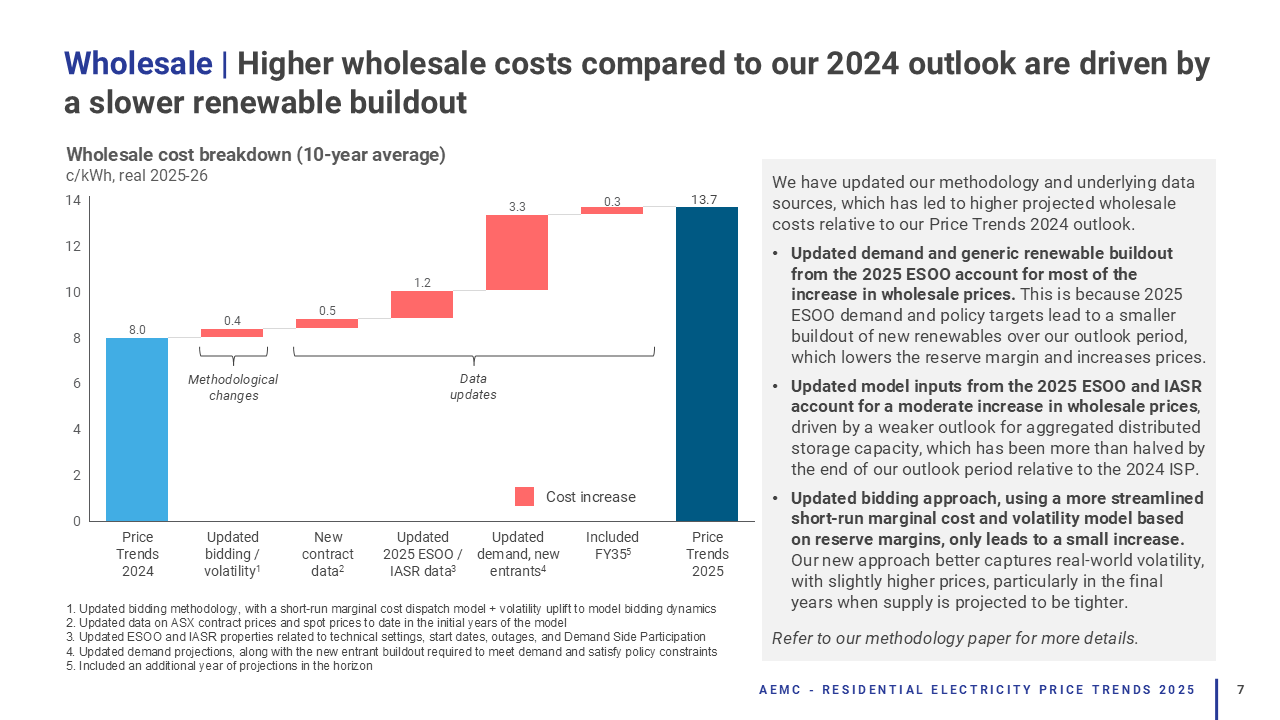

Wholesale markets provide a good example.

If renewable generation build‑out slows — whether due to connection delays, supply chain constraints, financing conditions or policy uncertainty — the system often relies more heavily on higher‑cost plant for longer. That can increase both average wholesale prices and price volatility.

And volatility matters.

Even if households don’t see wholesale price spikes directly, those risks flow through hedging costs, retail pricing strategies and ultimately household bills.

So stability of investment signals isn’t just an investor issue — it’s a consumer affordability issue.

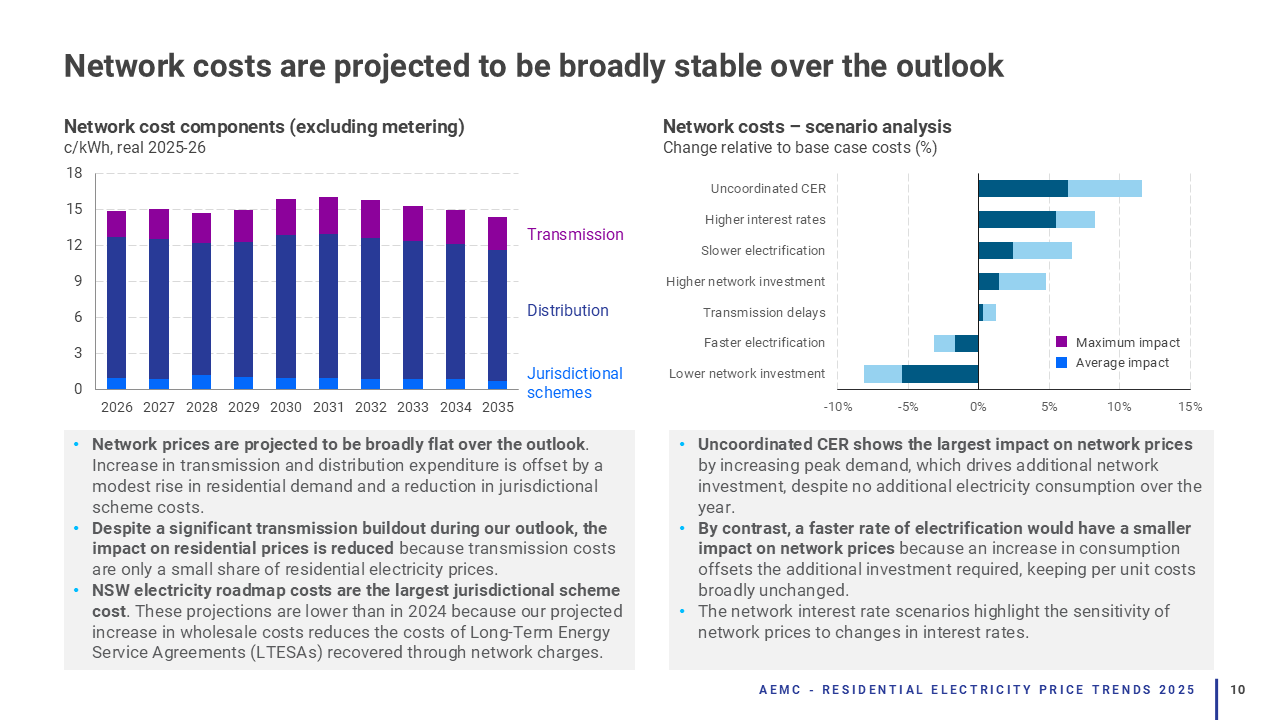

Network costs show a similar dynamic, although the story is a bit more nuanced.

Electrification increases electricity demand, but networks are built around peak demand, not average consumption.

So the critical question isn’t just:

“Are we using more electricity?”

It’s:

“When are we using it, and how concentrated is that demand?”

Uncoordinated electrification — for example clusters of EV charging during evening peaks combined with strong midday solar exports without storage — can increase peak demand and drive network investment needs.

But coordinated electrification can have the opposite effect.

Smart charging, storage integration, demand response and tariff design can improve network utilisation and help stabilise costs over time.

So electrification itself isn’t inherently cost‑increasing or cost‑reducing. Outcomes depend heavily on coordination, timing, infrastructure readiness and policy settings.

That’s an important message for policymakers.

Now let’s bring this back to households, because that’s really where the analysis becomes tangible.

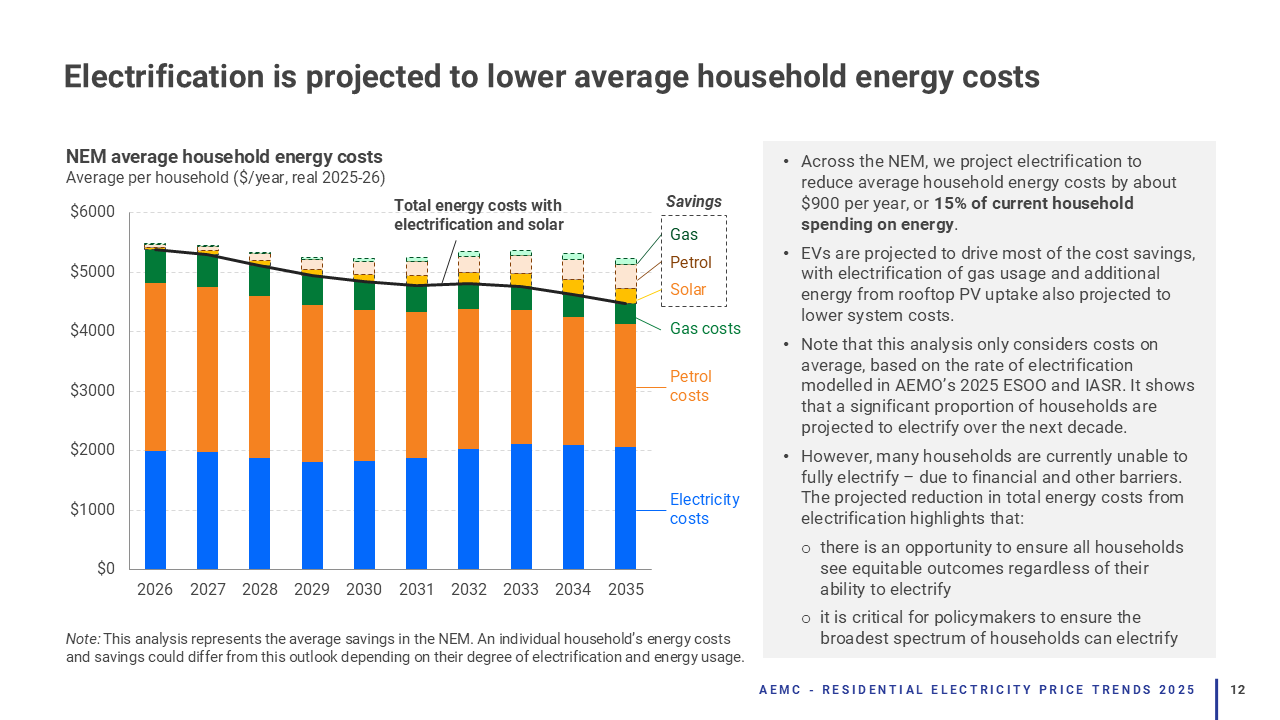

When we look at total household energy costs — not just electricity bills — a consistent picture emerges.

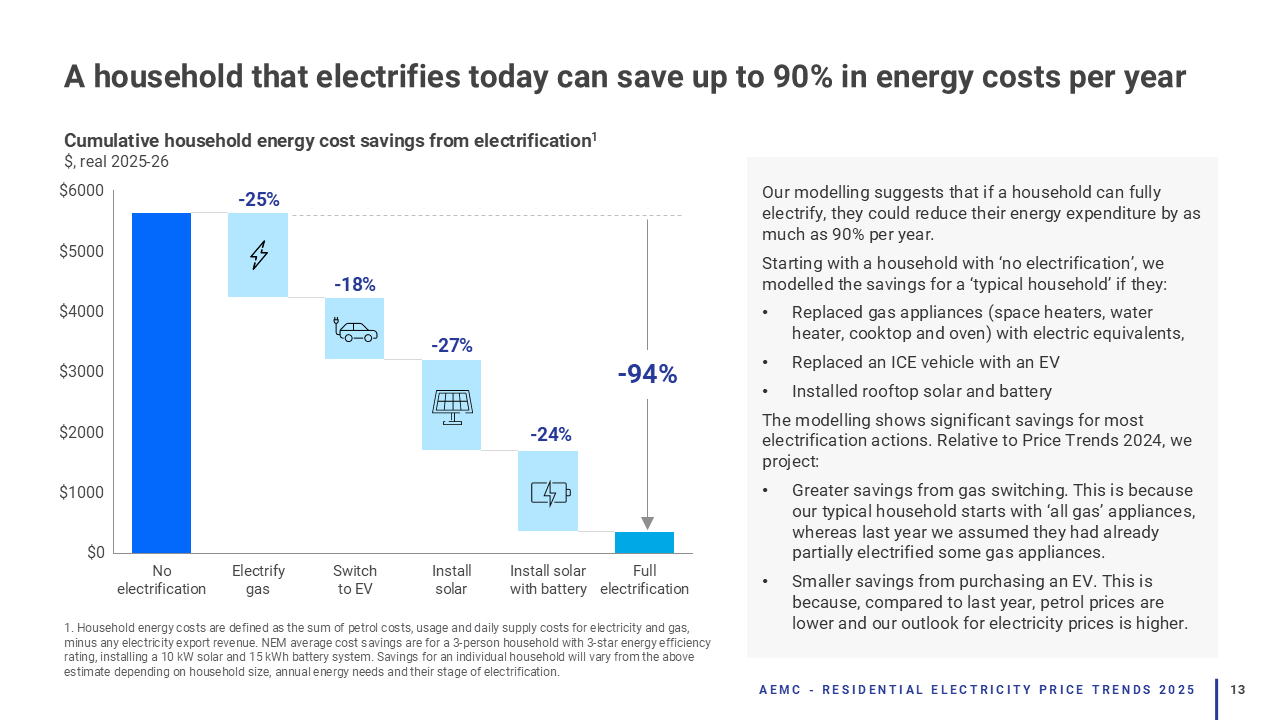

Electrification has the potential to reduce overall household energy spending over time.

Electric vehicles typically have lower running costs than petrol vehicles. Electric heating technologies like heat pumps are often more efficient than gas heating. Rooftop solar reduces grid consumption. Batteries allow households to shift energy use and capture more value from their own generation.

Taken together, these changes can deliver meaningful savings.

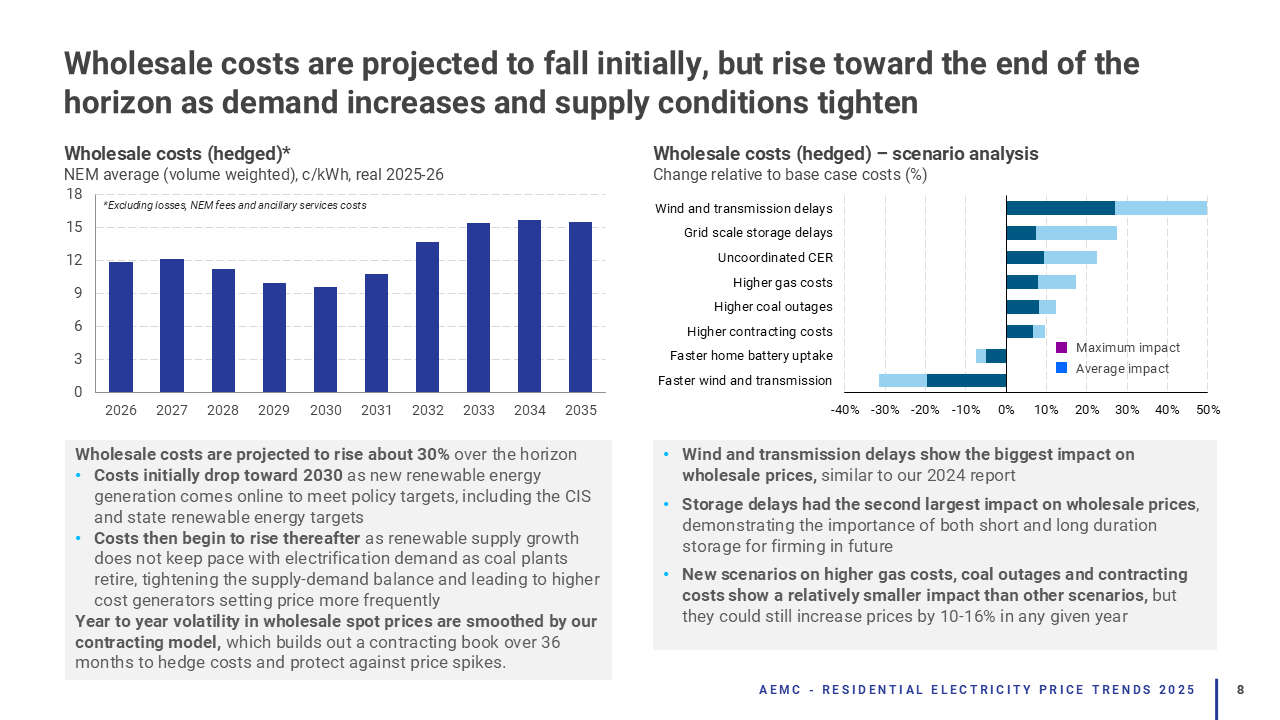

Our modelling suggests that average household energy costs across the National Electricity Market could decline by around 15 percent in real terms over the coming decade under plausible transition scenarios — even if electricity bills themselves rise slightly as households electrify more of their lives.

That distinction is critical.

Electricity bills might go up, but total energy spending can still go down.

But — and this is important — averages don’t tell the whole story.

Not all households can electrify easily.

Upfront costs, rental arrangements, apartment living, access to finance, infrastructure constraints — all of these influence who can participate in the transition.

Without thoughtful policy design, electrification benefits risk being unevenly distributed.

And that has implications not just for equity, but for social licence. If parts of the community feel locked out of the transition, confidence in the broader energy reform agenda can weaken.

Behavioural factors also play a bigger role than we sometimes acknowledge.

Energy decisions aren’t purely economic. People think about convenience, familiarity, perceived risk, reliability and trust.

Take electric vehicles as an example.

The economics are increasingly favourable, but adoption still depends heavily on charging infrastructure visibility and consumer confidence. International evidence shows adoption accelerates once public charging becomes both available and trusted.

So infrastructure policy, consumer information and market design all intersect with behavioural economics.

That’s not always reflected in traditional price analysis, but it’s central to real‑world outcomes.

From a system perspective, electrification also shapes infrastructure needs.

If demand grows but generation, storage and networks don’t keep pace, price pressures can emerge. If infrastructure investment keeps pace — and ideally anticipates demand — electrification can support both emissions reduction and affordability.

Planning approvals, connection processes, regulatory frameworks and investment signals all influence how quickly infrastructure can respond.

These may sound like technical regulatory issues, but they directly affect household energy costs.

Faster connections can mean lower costs. Delayed infrastructure can mean higher costs.

It’s that simple in many cases.

Another major development is the rise of consumer energy resources — rooftop solar, batteries, demand response, smart appliances and digital energy services.

When integrated effectively, these resources can reduce peak demand, improve system flexibility, limit network investment needs and dampen wholesale price volatility.

Importantly, the benefits can extend beyond households that directly participate. System‑wide efficiency gains help all consumers.

But integration doesn’t happen automatically.

Tariff design, export pricing, data access, interoperability standards and market rules all influence whether distributed resources deliver value or create inefficiencies.

That’s an area where ongoing regulatory evolution is critical. And these are all areas the AEMC has work underway.

Reliability is another essential dimension.

As generation mixes change and inverter‑based resources grow, maintaining system security requires new operational approaches and technologies.

Consumers need confidence that affordability gains won’t come at the expense of reliability.

And confidence matters enormously. Energy systems are foundational infrastructure. People expect them to work — consistently, predictably and affordably.

Maintaining that confidence is both a technical challenge and a policy challenge.

One of the most valuable aspects of the price trends work so far has actually been the iterative learning process.

Each annual update incorporates new data, policy developments, technology uptake trends and methodological refinements.

That continuous learning improves robustness and keeps the analysis relevant in a rapidly evolving sector.

We’ve seen assumptions change around battery adoption, electrification pace, generation investment pipelines, policy initiatives and consumer behaviour.

And that’s likely to continue. The energy transition is dynamic by nature.

So stepping back, what are the key messages I’d leave you with?

First, focusing solely on electricity prices gives an incomplete picture of energy affordability. A household energy wallet perspective provides more meaningful insights.

Second, electrification can reduce total household energy costs — but those benefits depend heavily on coordination, infrastructure investment and equitable access.

Third, timing matters. Delays in generation, networks or policy alignment can increase costs. Timely, coordinated investment helps keep the transition affordable.

Fourth, consumer behaviour is now central to how energy systems evolve. Household decisions about vehicles, appliances, solar and storage are shaping demand patterns and system planning in ways we haven’t seen before.

And finally, transparency and engagement matter. Publishing assumptions, methodologies and results supports better policy outcomes and stronger stakeholder confidence.

So just to close.

The energy transition isn’t only about technology or infrastructure. It’s fundamentally about households and businesses — affordability, reliability and confidence in the future energy system.

There are real opportunities to reduce energy costs through electrification, coordinated investment and smarter use of distributed resources. But capturing those benefits requires thoughtful policy design, efficient infrastructure development and continued focus on consumer outcomes.

The goal is straightforward:

A reliable, affordable and increasingly sustainable energy system that works for everyone.

Achieving that will require ongoing collaboration between policymakers, regulators, industry, researchers and consumers — across Australia, New Zealand and globally.

And the more we keep the consumer perspective at the centre of that conversation, the better the outcomes will be.

Thank you very much — and I look forward to continuing the discussion.