Danielle Beinart, EGM Networks & Technical

Keynote address, Australian Energy Week Conference 2025

Melbourne Convention and Exhibition Centre

Introduction

Thank you for your welcome!

It’s a real pleasure to have the opportunity to share our work with you today and please, be ready with your questions at the end because we are very ready to hear from you.

But first, like others before me today, I acknowledge the traditional custodians of the lands, waters and skies where we live and work. The AEMC recognises that First Nations people have cared for the places we all now call home for millennia before this time.

I pay my respects to the enduring relationship that Aboriginal and Torres Strait Islander peoples have to Country – particularly to Boonwurrung country where we meet today – and to the lessons those relationships have for each of us.

Setting the scene

I’m going to start with a bit of scene setting.

There have been many attempts to capture the scale of the challenges facing the energy sector as we aim for net zero emissions by 2050.

It’s been likened to the moon or Mars landings, the invention of the wheel, or the printing press or steam engines.

But I’m not here to capture the full gamut of our tasks, or we’d be here all day and I am conscious that for many of you this is the end of an enjoyable but, eventually, exhausting conference week.

I’m just here to talk about the AEMC’s role in the pricing reforms that consumers need all of us to deliver for an affordable, secure and reliable low-carbon future, and how you also can help to shape those reforms.

But as a way of setting the scene, I do have a somewhat related analogy for where we are at and how we’re thinking about pricing, and it begins with taking you back to the days of this little beauty: the classic Nokia 3310.

And even if you’re too young to remember owning one, you might remember mum or dad letting you play Snake on theirs.

It’s not the phone itself I want you to think about though – it’s the moment in time it represents for mobiles becoming ubiquitous. And, the real heart of the matter: think about the way the telcos initially approached pricing and billing for calls and texts with this incredible new technology.

I’ll be coming back to this shortly, and I don’t want you to think we’re suggesting energy bills follow the exact same arc as phone billing has done. But I do want you to know that the review we’re conducting is coming from a bold, future-consumer-focused perspective and our scope for change is ambitious.

Timely discussion

Pricing reform is a timely discussion for many reasons. You’ve heard Minister Bowen announcing he will ask AER to review the Default Market Offer at the conference this week. With our Pricing Review due to finalise in March next year, we will continue to collaborate with our AER colleagues as we each pursue these important reforms.

You all know this.

The energy sector is going through unprecedented change And in Australia we face unique challenges, including the growing scale, pace, and engagement of Consumer Energy Resources (or CER) in a grid that covers vast distances and multiple jurisdictions.

Very often this means we are at the vanguard of global change – we have no choice but to invent new solutions because no one else can answer the questions we are asking.

The AEMC’s focus is on reshaping and creating rules that proactively manage engineering and economic challenges, and the huge influx of inverter-based technologies that can see the mix in the NEM rapidly vary on any single day.

Our job at the Commission – and indeed for all of us – is to anticipate and prepare for that change. And I acknowledge the work being done across the sector, including by many of you here in the room today, to do that.

But these changes aren’t just about technology, governance and systems management. They are meaningful for all of us, whether we work in the energy sector or not.

It’s meaningful for all of us, because we’re all energy consumers. And the role of the consumer in our energy system is changing.

CER changes everything

I know you’ve heard a lot about this over the past few days from other speakers, but it’s worth taking a moment to reflect on the scale of change occurring with CER and what it means for the future and of course pricing.

Once upon a time we received electricity one way from a few big generators that supplied the whole grid. Our only choices were which devices and appliances we used and when we turned them on or off.

Consumers can now generate, store and consume significant percentages of their energy without interacting with the grid.

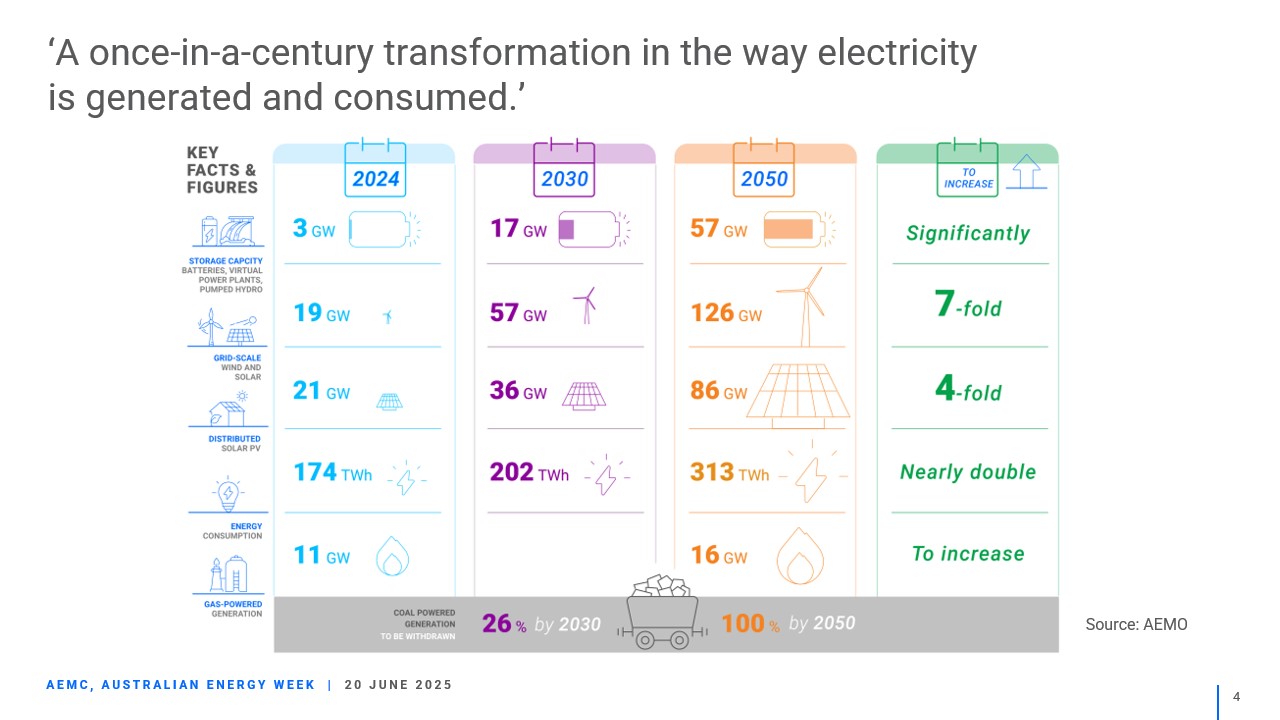

AEMO’s Integrated System Plan (ISP) – the energy transition roadmap – shows us what we’re heading towards. It says that by 2050, we’ll have:

5 times today’s levels of CER, accounting for almost half of the NEM.

80% of detached homes will have rooftop solar, up from around one-third today.

Residential and commercial batteries will account for 34GW of capacity, compared to 1GW today.

And 97% of vehicles will be electric.

I’ve got some of these numbers up on the screen and I’ll be honest, it makes me feel a little nervous – the numbers are changing so fast that it’s always a little risky to put them on display, isn’t it?! But they do tell the story of a one in a lifetime evolution.

Pricing for consumer revolution

We often think of CER in terms of our world-leading rates of rooftop solar, supported by other household investments like batteries and EVs. This is certainly what the ISP talks about.

We also often hear of CER owners in a context that means heavily engaged, early-adopting, solar-app wielding afficionados who actively hunt down great deals and navigate the system with relative ease.

But we need to also factor anyone who has any device with flexible load, like dishwashers and air conditioners – many of us have these in our homes already fitted with built in timers or delay-start functions.

And we need to consider consumers who, even if they have all the toys that new energy tech can offer, just want a simple price for a simple service.

So, we’re looking at potentially millions of additional sources of controllable energy demand and supply being added to our system, including those owned by customers who can’t access rooftop solar or domestic batteries or who don’t engage actively in the grid.

And you must all know this story by now: if we get this right, if we integrate CER well, and we meet the needs of all customers, it means:

Everyone can save money, by choosing how and when they use energy.

We see lower overall system costs and improved reliability, which again benefits consumers.

Those who engage actively with their CER technologies can reap greater rewards, by allowing their assets to participate in the wider power system.

The market operator can more efficiently match demand and supply and manage system security.

And perhaps the greatest benefit of all is that collectively we’ll help Australia achieve a net zero energy system.

System savings

All these opportunities and challenges and more are also discussed in a relatively new tool the AEMC has been applying, our Strategic Narrative. You can grab a copy from the QR code up on the screen.

And the upshot is that there are substantial system savings to be gained from effective coordination. These savings of course would be felt by consumers through lower bills across time.

If we get this right, we’ll need to build fewer large-scale infrastructure projects to keep the system running.

And we all know how hard they are to build at the moment.

Estimates vary as to the total value of integrating CER well.

The current ISP estimates $4.1 billion in avoided grid-scale investment.

the ENA Electricity Transformation roadmap suggests $16 billion could be avoided

we engaged Energeia to look at this, and they found CER assets could help deliver $45 billion in overall system benefits to 2050.

So, no matter which numbers you believe, and they are all big, there’s a lot riding on getting CER integration right.

What is certain is that if we fail to integrate CER effectively, we’ll have a less efficient system. It will need more electricity to be generated and transported and most importantly, it will be more expensive for consumers.

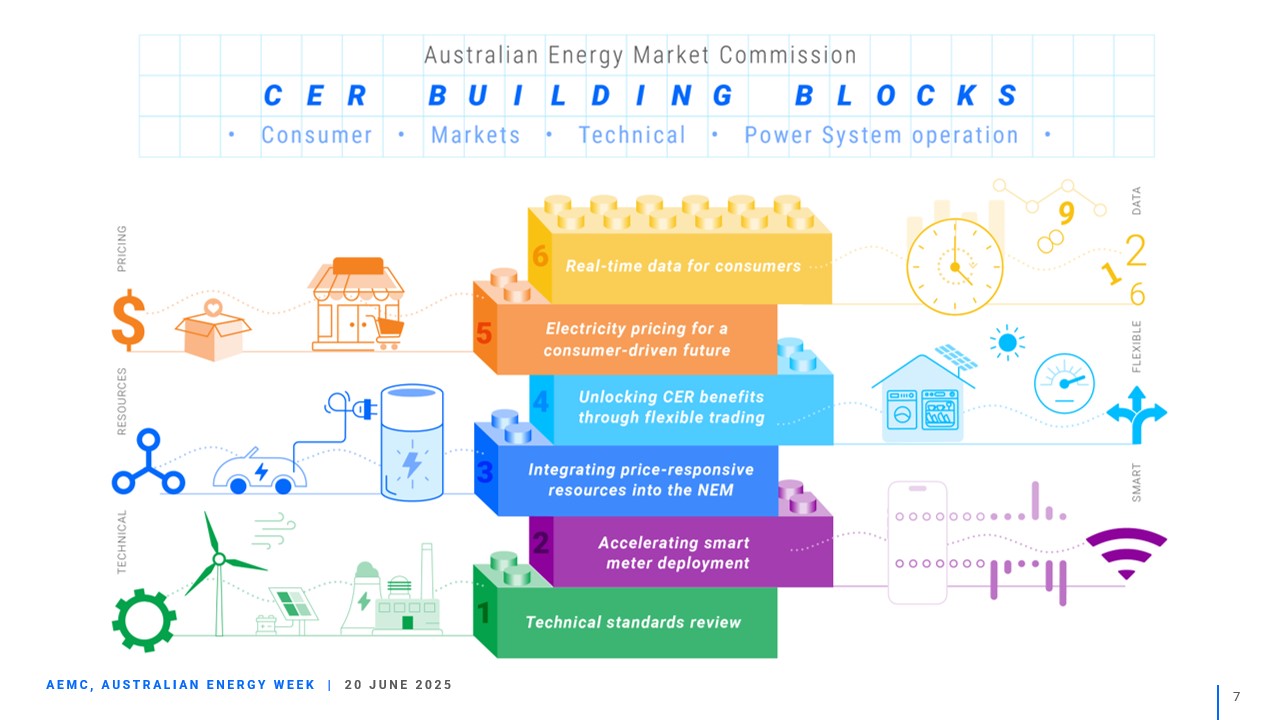

That’s why a large part of our work plan at the Commission relates to CER. Some of our recent and current work in this area includes:

Accelerating the rollout of smart meters.

Unlocking CER benefits by allowing consumers to separately meter their flexible and passive loads.

Better integrating price-responsive resources into the NEM to improve the overall system efficiency (and lower cost) for consumers.

Real-time data for consumers – which is looking at enabling better consumer access to the value of the data produced by their smart meters

And, the purpose of today – that orange block up on the screen is our Pricing review – and it’s an ambitious review of what pricing needs to be in a consumer-driven future.

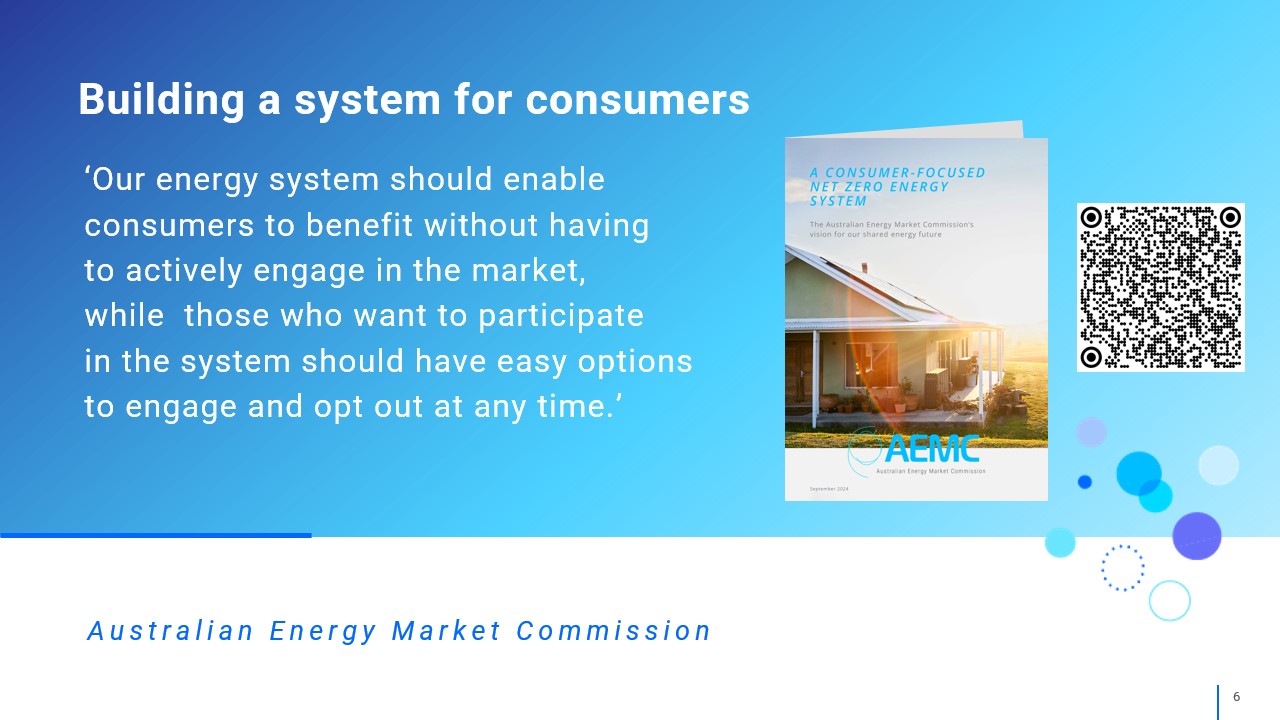

Building a system for consumers

Our review is about building a set of market and regulatory arrangements that deliver a system that’s designed for consumers.

Importantly, and we’ve thought about this a lot, we are building arrangements that meet consumers where they are, rather than trying to change or educate consumers to meet the needs of the system.

We’ve gone through decades of trying to educate consumers to change their behaviour.

But research tells us that most consumers don’t want to change. They want electricity that’s affordable, bills that are predictable, and they want it to be available when they need it.

It’s honestly as simple as - If you flick a switch, you want the thing to turn on.

I’m now going to take you back to the noughties or thereabouts and my question for you now is NOT do you remember your first mobile phone, but do you remember your first mobile phone plan?

If yours was like mine, it was probably a lot like your current energy bill!

You had different rates for calls at different times and to different destinations and you had to pay individually for texts.

I remember staying up really late at night, for instance, to call my grandma overseas – not because of the time difference but because of the cheaper rates on offer once all the normal people were in bed.

People got bill shock – crazy phone bills of hundreds of dollars, because they made too many calls and at the wrong time.

And then what happened?

Telcos figured it out. They recognised that customers wanted a simpler way to access the service they wanted. And importantly they went about fixing it.

Nowadays, it’s so much simpler!

You never have to worry about what time it is when you make a call.

And you know exactly how much your bill will be each month. It doesn’t change for the life of your plan – so easy.

Electricity customers are the same customers that buy phones. Most of them want electricity to be simple, predictable, reliable, and hopefully as cheap as possible.

Nobody pretends that energy is the same as telecommunications, but surely we can work together towards a more consumer-centric way of doing things. And that is what the AEMC’s pricing review is all about.

The AEMC’s vision for the future is a consumer-focused net-zero energy system. Our pricing review is key to delivering on this vision

You may have read the discussion paper we released earlier this month – and if you haven’t, I invite you to give it a read.

It outlines two fundamental objectives of the pricing review.

Firstly, ensuring that the pricing framework supports the availability of the products and services that consumers want in the future (hopefully not unlike the telco example I offered), while also

Secondly, delivering a lower-cost system for all consumers.

We recognise the current framework may not sufficiently achieve either of these objectives in a CER-dominated future.

The Review also lays out some important opportunities we have before us.

For example, we can consider the interaction between retail and network pricing to better recognise consumer preferences. And, with CER much more progressed than it was in 2014, we can ensure the pricing regime supports the integration of CER in an equitable way.

Through this review, we’ve asked stakeholders – you – a series of questions:

Knowing what we know about technology and also knowing what customers tell us they want, what will ‘good’ future energy offerings look like?

What we’ve heard so far is that most of the ‘good’ future offerings are already here. The problem is just that they are not at scale, and not necessarily available to all customers. This is good news.

And here’s another question:

What are the regulatory barriers to getting those ‘good’ offerings out to the market?

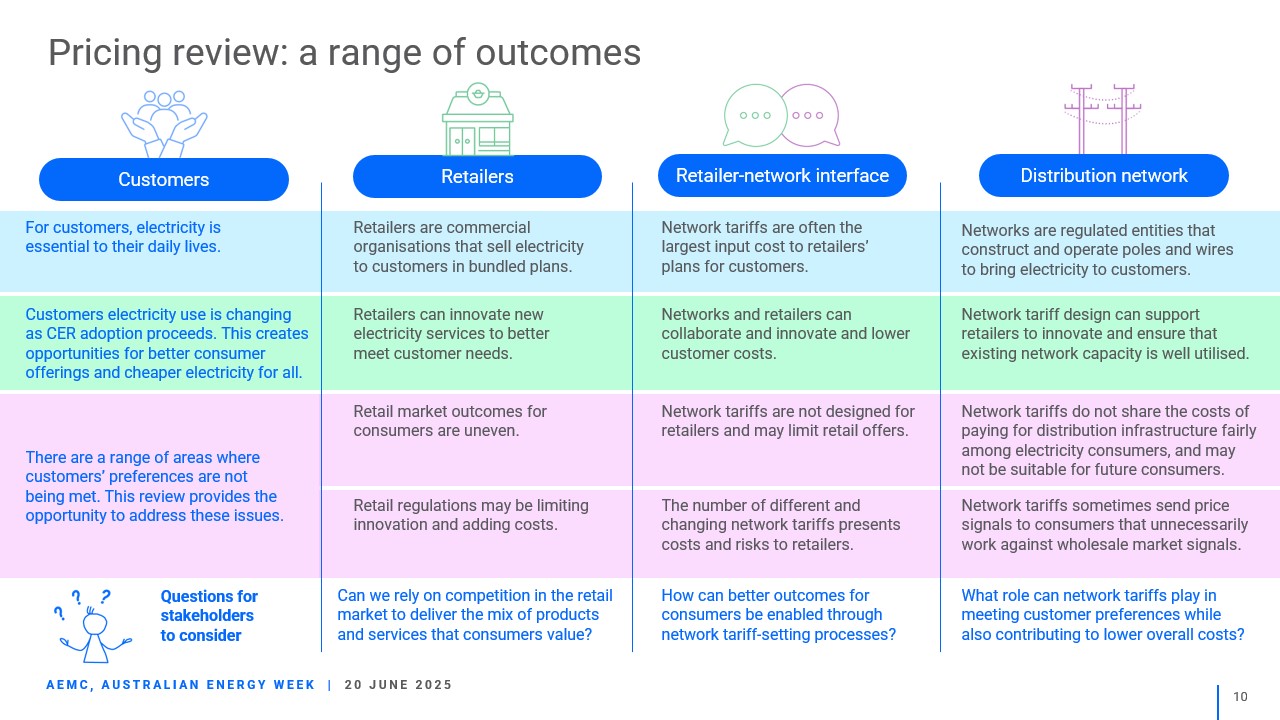

Stakeholders have helped us to identify the barriers that stand in the way of consistently good customer outcomes. We’ve mapped these across the key segments of the supply chain that are in scope for this review – which is the retail market through to distribution network arrangements.

In the retail space, a couple of big issues we’ve heard through consultation are that:

Outcomes for customers in the retail market are uneven

To get a good deal customers often need to regularly switch plans. This excludes customers who find the retail market complex and confusing and have difficulty comparing alternative offers and/or retailers. Which we are hearing is many if not most customers.

Retail regulations may be limiting innovation and adding costs.

Aspects of retail market regulation – in particular, consumer protections - do not deal with newer energy services.

And as I heard more than a couple of times here yesterday, retail market regulation also differs across states, leading to a high compliance burden for retailers, which flows through to increased costs for consumers

We’re also looking at the process by which network tariffs are set. What we’re hearing here is that network tariffs are not designed for retailers and may limit retail offers.

For example, they may discourage retailers from offering subscription-style products and other product types that are popular in markets outside energy.

Different and changing network tariffs present a cost and risk to retailers. Retailers must manage a number of network tariffs for each distribution region of the NEM they operate in and for each type of customer they serve. This is further complicated by regular changes to these tariffs. And the costs retailers incur here will typically flow through to customers.

And of course, a key component of the Review is looking at network tariffs themselves.

What we’ve heard here is:

Network tariffs do not share costs fairly among electricity consumers, and they may not be suitable for future consumers.

For example, under some network tariffs, consumers with CER can avoid some network costs, while consumers without CER cannot - and so these customers may end up paying a bigger share.

Another thing we are hearing is that network tariffs sometimes send price signals to consumers that unnecessarily work against wholesale market signals.

This can encourage consumption patterns that may not be preferable to consumers, and also may not even lead to lower network or wholesale costs.

For example, you might avoid turning on the washing machine at say 4pm in summer because of the peak network time of use prices on your plan, even at times when the wholesale spot price is low or negative and there’s no network congestion in your area.

Your behaviour here is potentially inconvenient for you, and doesn’t help anyone else either, because you are not lowering costs for others.

So while there are some significant issues, there is an opportunity for the Pricing Review to address these.

Stakeholders are already sharing their ideas with us as to the kinds of reforms we could pursue to address the barriers.

We’re also working closely with stakeholders to take in the learnings from their research, and from pilots and trials.

We are committed to undertaking the Review in an open and collaborative manner. This involves more consultation than is typical for our projects.

It also involves a different time schedule – we have introduced an extra stage in the process, with our discussion paper, to make sure we continue to hear stakeholders’ views as we move towards draft recommendations.

Subject to stakeholder feedback on our discussion paper, the next step in the review is to socialise and consult on solutions to the barriers we’ve identified.

We have the opportunity to reimagine network tariffs

I wanted to go a little deeper on network costs and network tariffs, which are a key consideration in our pricing review, because they’re the largest component of residential and small business bills.

We see the review as a really big opportunity to contemplate meaningful reform to how this is done.

Our last major review of tariffs was 11 years ago – back in 2014.

At that time, we understood consumers were best served by predictable long-run price signals from the network.

These included time-of-use tariffs, making consumption more expensive in periods of peak demand.

As I’ve just outlined though, there are material issues with the way network tariffs are working in the market in practice.

In 2025, with the technology available to consumers, industry and market bodies, we have new opportunities available to us.

We don’t have to just send broad-based, long run signals. We can contemplate other, smarter ways of doing things, leveraging the technologies that are now available.

Most importantly, we think we have the chance to make things simpler and easier for customers while not sacrificing a low-cost system.

So, here are a couple of observations on network tariffs.

First, network tariffs play a significant role in communicating to consumers the value of changing their behaviour and investments to contribute to a more efficient system for all.

I’ll explain why:

The wholesale market can fluctuate from high prices to potentially negative prices, but customers generally don’t face this volatility in the way they pay for electricity. Retailers hedge these costs on customers’ behalf and they generally do this really well.

Network tariffs are different. Consumers with smart meters generally do get some form of network signal through their retailer. This is commonly a time-of-use signal.

What this means is that the way customers pay for electricity is often heavily influenced by their network tariff. Peak rates in the evenings discourage people from using electricity at that time, while cheaper rates overnight and during the middle of the day do the opposite.

A second observation on network tariffs - the current tariff framework delivers network signals based on long-run costs, which are broadcast to consumers across whole networks.

This leads to the issues I described earlier – some consumers can avoid network tariffs by for example investing in solar PV, while others will avoid heating their homes in winter, when the network peaks in summer.

These actions come at a cost to the individual consumers, and they may not always deliver reduced network costs in return.

We believe network tariffs need to support a broad array of plans that meet consumer preferences, while also supporting a lower-cost system.

For example, rather than having an ‘efficient’ signal broadcast to all consumers, under the presumption that ‘one size fits all’, we may see a package of tariffs that offers:

Rewards to those who can engage and

Simpler lower-cost network tariffs for everyone else.

We also believe network tariffs have a role in harnessing the potential of consumers to contribute value for themselves and others, in two key ways:

Consumers should be appropriately rewarded for their actions and investments that contribute to lower network and wholesale market costs.

Importantly, the inverse is also true, consumers should not be rewarded for actions or investments which do not contribute value to the system.

But to make that reward pattern possible, consumers need to have the opportunity to access signals that make the most of their CER. This might mean more dynamic and localised network signals for those who want them.

In addition, network tariffs shouldn’t stop consumers from engaging with the wholesale market.

Some recent modelling work we commissioned suggests the value of consumers responding to the wholesale market is up to 8 times as valuable as the potential network costs savings.

This supports our argument that the network tariff framework should deliver signals that don’t get in the way of wholesale market signals.

Conclusion

Which brings me to the end of talking at you, and a welcome return to talking with you! So please don’t forget to download the review’s discussion paper and send your response in by the 10th of July.

I mentioned earlier a broad relationship between the way mobile phone technology and billing have changed and how open we are to major changes in energy billing for the consumer of the future.

Like telecommunications, energy is an area that touches all of us personally, and with great changes come great demands for reform.

We are able to revisit pricing reform because of the progress that’s been made over the past decade, not despite it.

Technological innovation and the Australian consumer’s embrace of CER have helped drive this change.

And if we capture those benefits in our pricing review, and take the opportunities to consumers instead of expecting them to come to us, we can further propel ourselves to a successful energy transition.

Thank you.