Victoria Mollard, Executive General Manager, Economics & System Security

Australian Renewable Energy Zones Conference

Swissotel, Sydney

Good afternoon. Let me first acknowledge the Traditional Custodians of the land on which we meet today, the Gadigal people of the Eora Nation, and pay my respects to Elders past and present.

Thank you to the conference organisers for inviting me back for another year – and to all of you for sticking around for this session. I’ll do my best to make it try to make it worth it.

My name is Victoria Mollard and I am Executive General Manager of Economics and System Security at the Australian Energy Market Commission.

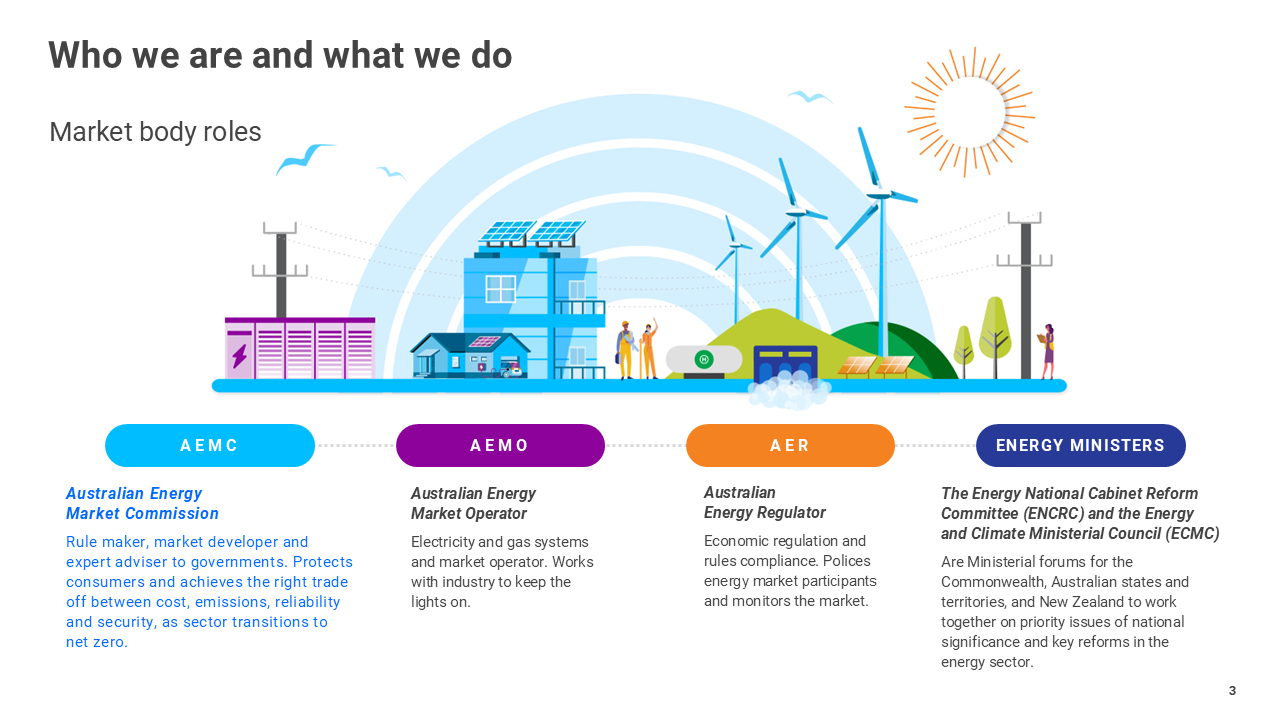

For those less familiar with us, the AEMC is one of the three Energy Market Bodies.

At its simplest, our role is to help to deliver a power system that works in the long-term interest of consumers – one that is reliable, secure, safe, low emissions and low cost.

We make the rules for the National Electricity Market, parts of the gas market and related retail markets.

We also advise governments on how the system needs to evolve as the transition accelerates.

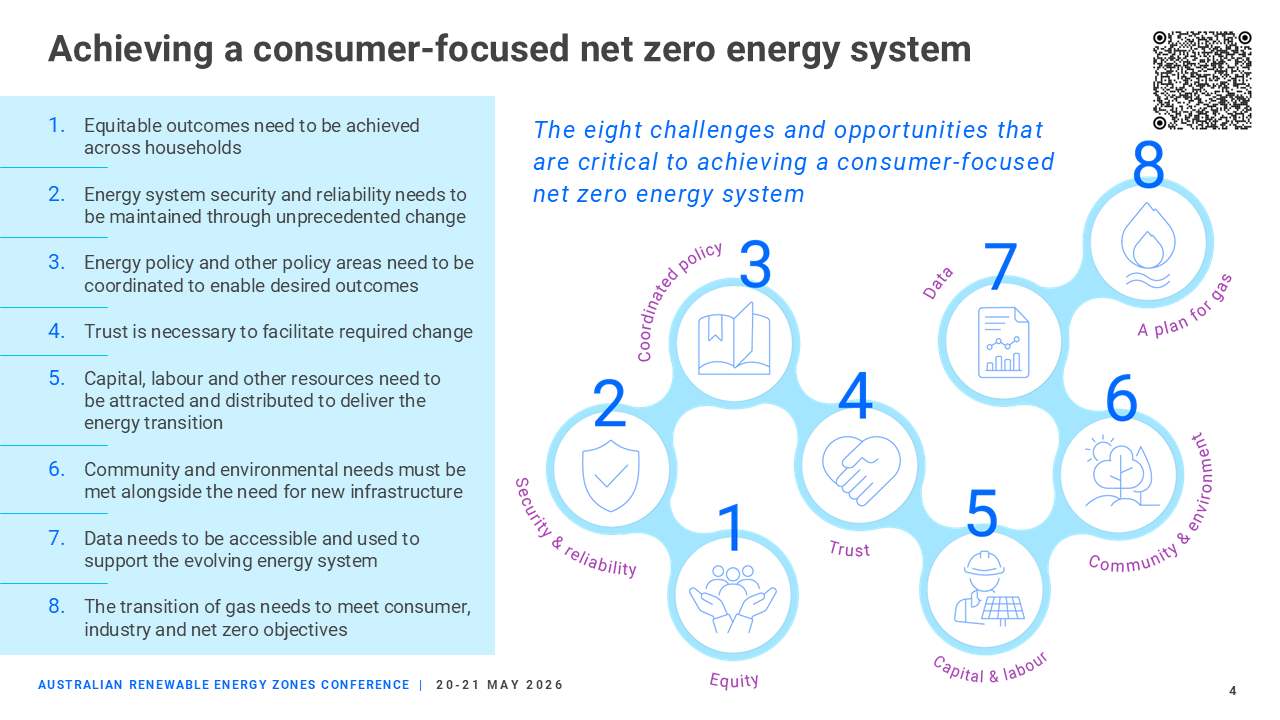

Much of our work is guided by eight challenges and opportunities we see as critical to achieving a vision of a consumer-focused net zero system. We set these out in our ‘strategic narrative’ which is our narrative of the longer term work we must do to successfully navigate a clear path to that consumer focused net zero Australia.

You can find this online if you’re interested.

Today, I’ll focus mostly on Number Two – How do we maintain energy system security and reliability through unprecedented change – which relates to the transforming nature of the system including the influx in REZs.

Before I turn to that, I want to quickly highlight a few big pieces of AEMC work that may be of interest to this audience.

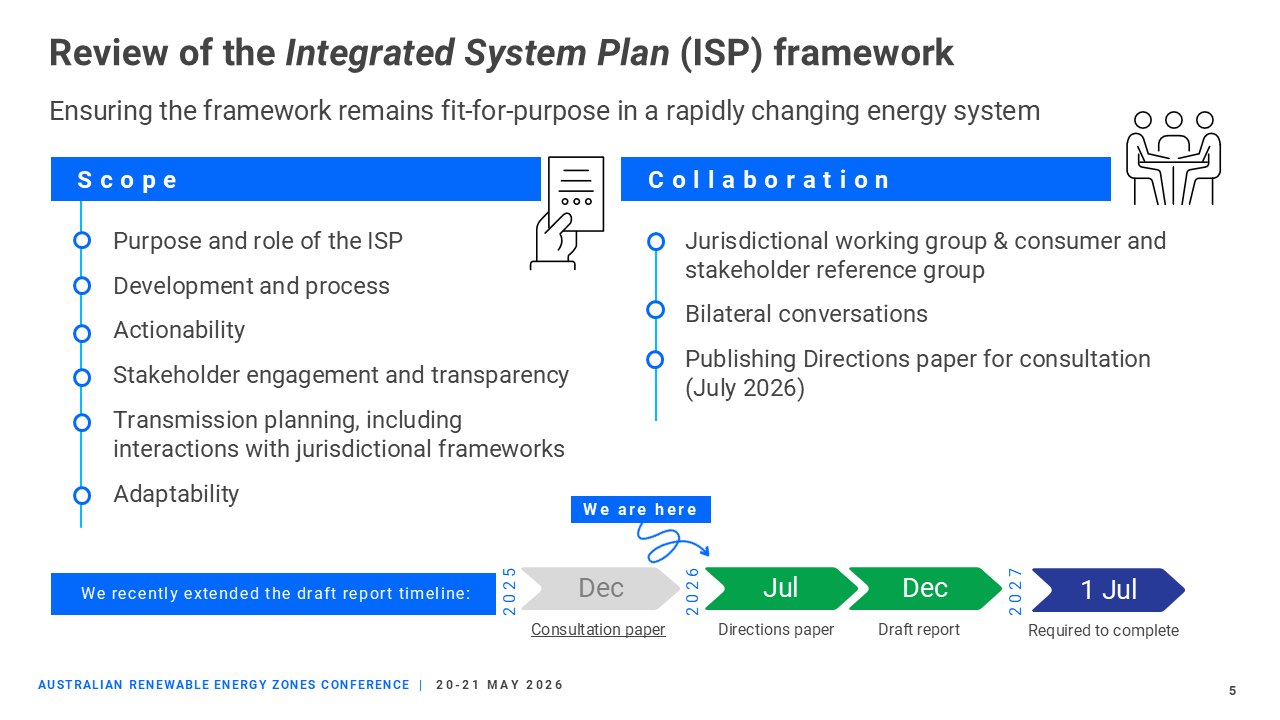

We recently began a Review of the ISP framework to ensure it remains fit-for-purpose in a rapidly changing system.

The review will include looking at how the current ISP framework best contributes to achieving the NEO. Part of this is looking at how it interacts with jurisdictional frameworks, such as how the state based REZ planning documents interact with the NER documents of the ISP and transmission annual planning reports.

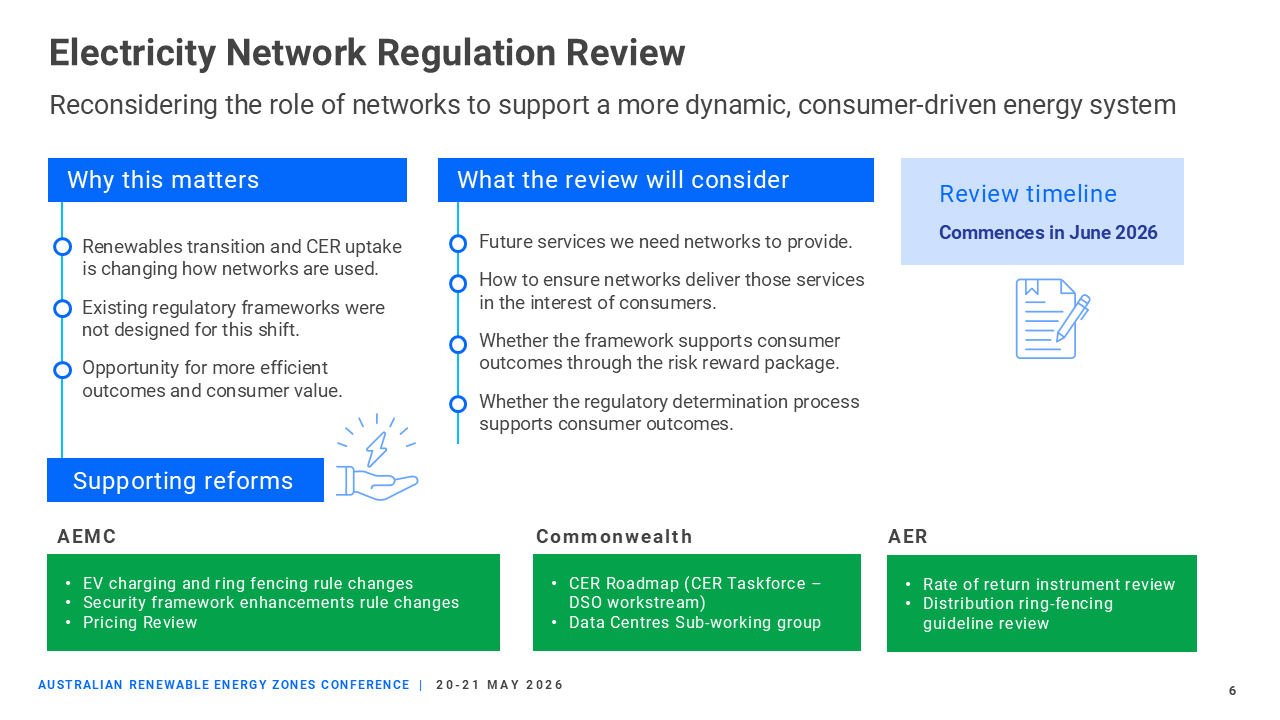

We’re also about to commence review into Electricity Network Regulation to reconsider the role of networks to support a more dynamic, consumer-driven energy system.

We will be considering rule changes we have on EVs and ring fencing alongside this review.

And that will commence shortly.

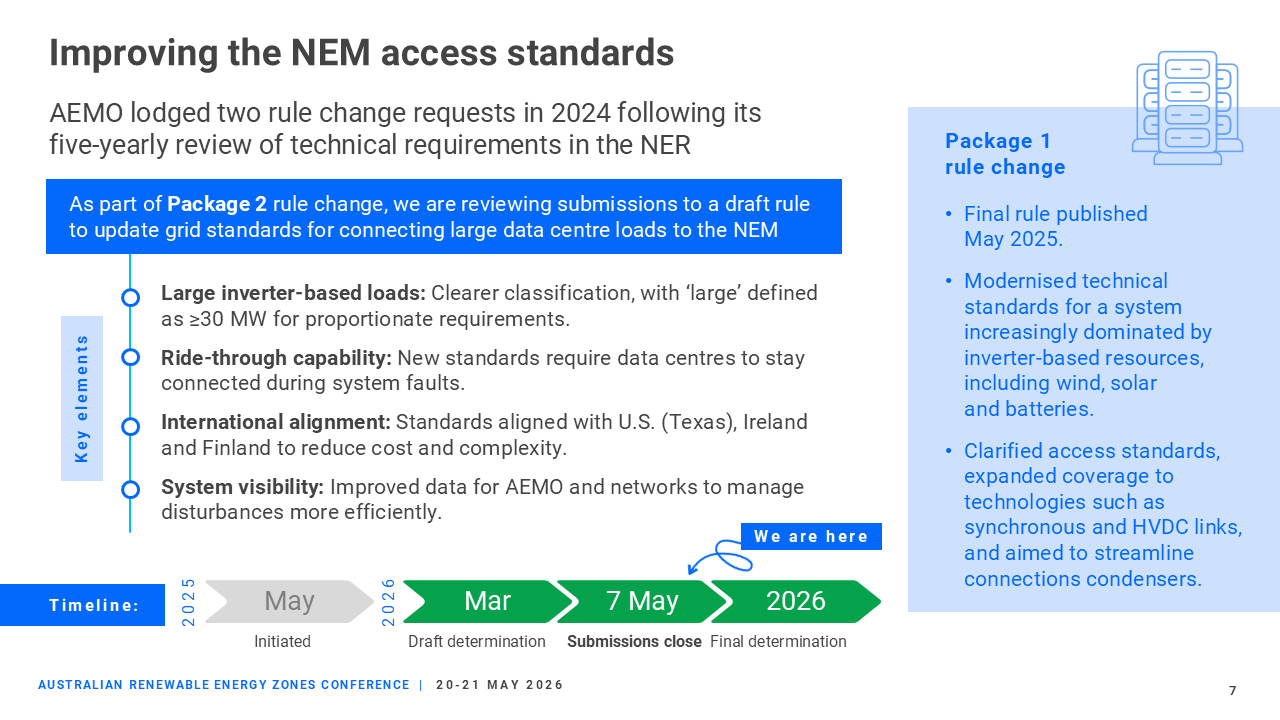

Finally, last year we finalised a major overhaul of technical requirements for renewables and batteries connecting to the grid.

Later this year we’ll publish our final determination on a rule change from AEMO that’s looking to update grid standards for connecting large loads such as data centres to the NEM.

And Ministers have now asked the AEMC to advise on how regulatory frameworks could support expectations for data centres to bring forward renewable generation and firming, operate flexibly, and locate in ways that support the broader energy system. In some ways concepts not dissimilar to REZs.

So there is a lot underway at the AEMC. If you want to chat to us about any of these topics please reach out after my session today or use the ‘contact project leader’ forms on our website.

Today I want to focus on how batteries are becoming central to the reliability and security task in our system – and what this means for renewable energy zones.

The uptake of batteries

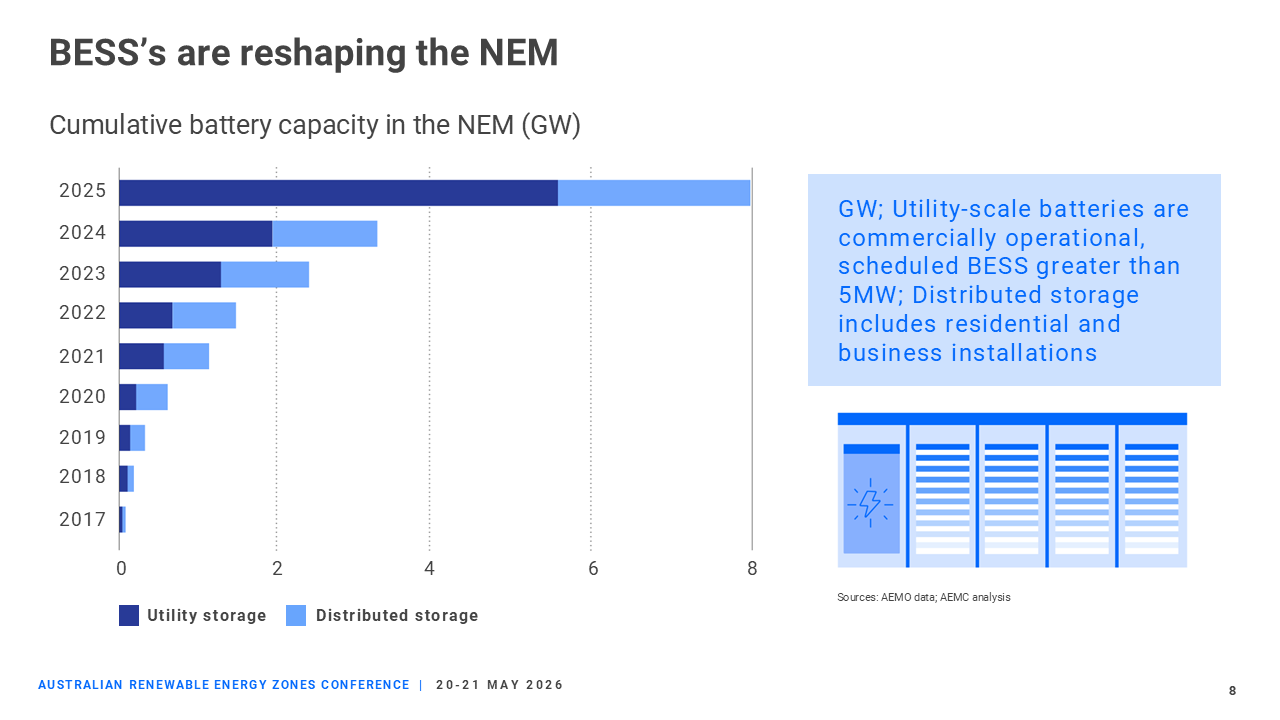

So to set the scene, the uptake of batteries is one of the key themes in this current chapter of Australia’s transition.

They are moving from the edge of the NEM to the centre of it.

This chart shows the cumulative battery capacity in the NEM – comprising both utility scale storage as well as distributed storage i.e. behind the meter capacity.

By the end of last year, utility scale and behind the meter battery capacity reached around eight gigawatts – and that number is certain to rise again this year. We have definitely seen a sharp increase since the Cheaper Home Batteries Program was introduced – and the home battery uptake is faster than the peak rooftop solar uptake.

So we have a lot of ‘battery capacity’ in the system.

But capacity is only part of the story. It’s also how batteries are changing – or complimenting – what renewables can do for the system:

they can shift renewable generation from when it is produced, to when it is needed

they can help manage the ramps that emerge as solar output falls away

and they can help smooth the flow of energy across shared network infrastructure.

As an example, we understand that nearly all solar generation at the moment is being co-located with batteries.

How batteries can complement other types of generation is especially important for REZs.

This is because the value of a REZ is not determined only by how many megawatts of generation connect inside it.

It’s also determined by how effectively that generation can be integrated, stored, shifted and delivered into the broader system.

In that sense, batteries cannot just be an add-on to REZ development, but they can become part of the operating model for making REZs work – helping renewable generation become more usable, flexible and valuable to consumers.

Implications for reliability

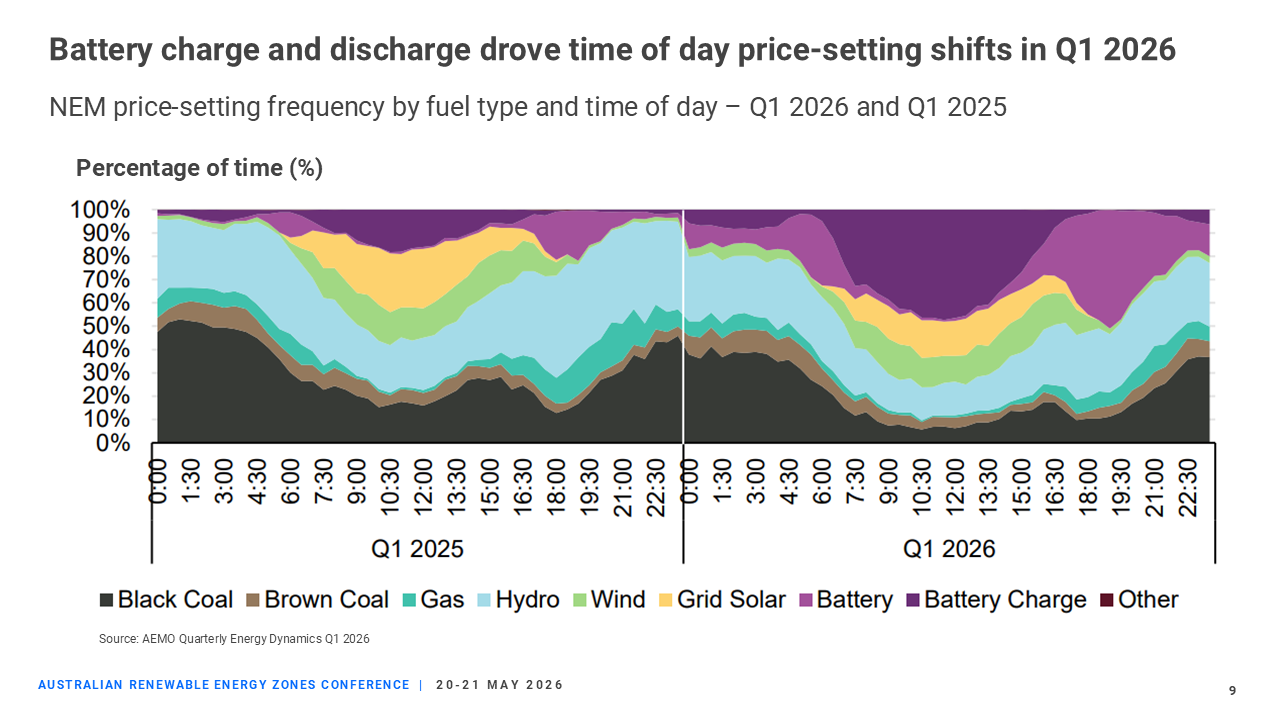

The next part of the story is how batteries are starting to change daily market operations.

This is a chart from AEMO's Quarterly Energy Dynamics. You can see that in Q1 this year, battery charging became much more prominent through the middle of the day - when renewable output is typically strong.

Battery discharge also becomes more visible later in the day, as solar output fell and the system moved into higher-demand periods.

South Australia shows us where this can lead.

For 30 days between mid-February and March this year, batteries delivered, on average, higher peak morning supply than gas.

This does not mean gas peaking plants disappear from the reliability picture.

But it does show batteries moving from a supporting role to an operational role.

For REZs, if people are thinking about integrating batteries, then that is the practical lesson...

Storage is not just insurance for the edge case. It can be part of how renewable energy is made useful across the day.

The Reliability Panel’s work helps explain the implications.

The Reliability Panel forms part of the AEMC’s institutional arrangements – it is comprised of members who represent a range of participants in the NEM – and is chaired by a Commissioner.

They determine the standards and some of the guidelines used by AEMO and other market participants in the NEM that help to maintain a secure and reliable power system.

Every four years, the Panel undertakes the Reliability Standard and Settings Review.

It considers the level of reliability consumers should receive – i.e. the “standard”, and the market settings - the market price cap and price floor as an example - needed to support efficient investment in generation, storage, interconnection and demand response across the NEM.

The Panel’s role is to recommend a reliability standard and associated market price settings that signal investment in an appropriate mix of resources, balanced with the level of reliability consumers value.

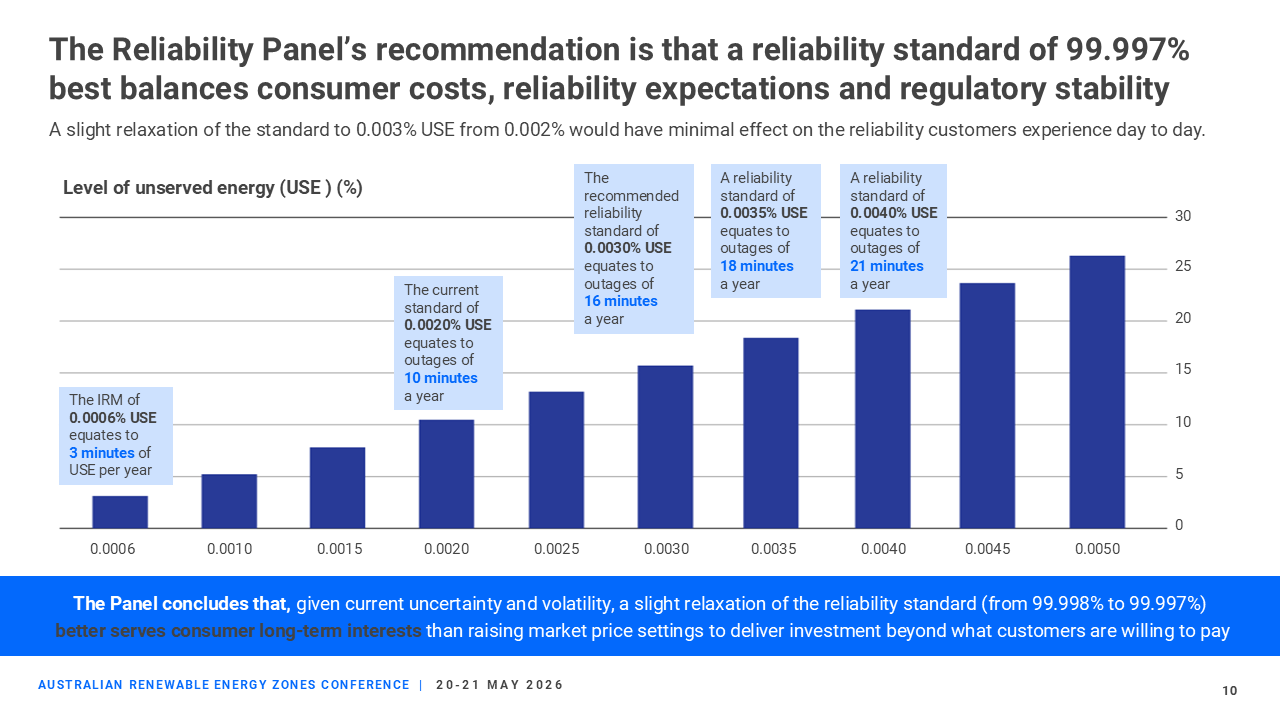

The latest review proposes updating the reliability standard to 0.003 per cent expected unserved energy from the current 0.002 per cent for the period from 1 July 2028 to 30 June 2032.

The recommendation reflects a careful trade-off between the reliability consumers value, and the cost of delivering more of it.

The review highlighted that the reliability standard has become less aligned with observed outcomes and consumer experiences – which is why the Panel recommended evolving the reliability standard rather than further raising the market price settings.

The recommended change to the reliability level is informed by modelling that the Panel undertook, and which reflect changing inputs of a reduction in the value of customer reliability, an increase in the costs of new generation capacity – and changes to the size and duration of modelled unserved energy events.

The recommended standard, if implemented, would have minimal day to day impacts on the reliability outcomes consumer experience’ – increasing the planned long term target from an average of 10 minutes to 16 minutes of unserved energy per year, while avoiding increases in costs required to meet the current standard. The review was informed by the Panel’s earlier Form of the Standard review, which asked a more fundamental question: are we still measuring reliability risk in the right way as the system changes?

In this, the Panel concluded that expected unserved energy remains the right form of the standard.

But the work also showed that the nature of reliability risk is changing.

It is becoming more regional, more weather driven, and more dependent on the depth and duration of tight supply events.

In the old system (and in energy, old can sometimes mean five years ago), reliability risk was often framed around a familiar problem: a hot summer day, high demand, and a large thermal generator outage.

That risk has not disappeared. But that story is evolving.

In a renewable-rich system, we also need to ask whether the system has the right mix of resources, in the right places, with the right duration, to manage variability across hours, regions and seasons.

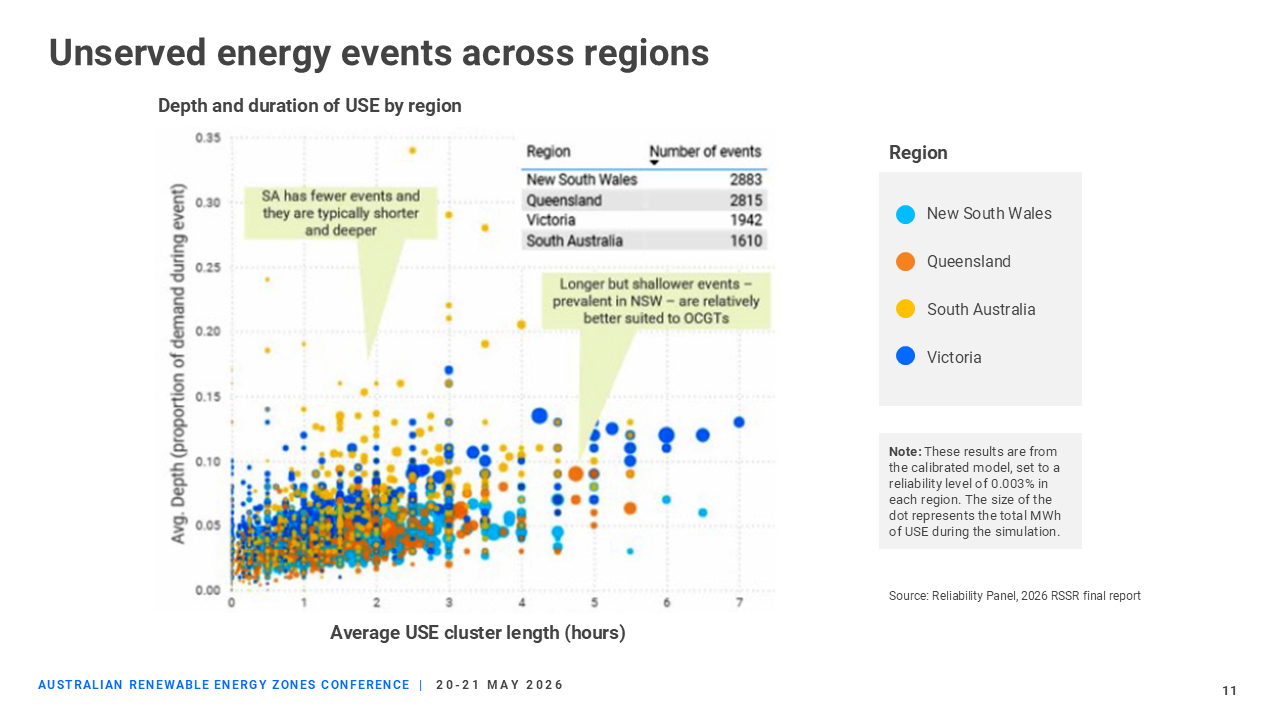

This chart shows why reliability risk cannot be treated as one uniform problem across the NEM.

This shows the depth and duration of USE by region – the coloured dots represent the different regions e.g. dark blue is Victoria; lighter blue is NSW; orange is Qld and yellow is South Australia.

This data is taken directly from our electricity market simulation model using an internally generated 83 year (1940-2024) renewable energy production data set.

The dots are not actual outcomes on the system but are simulated outcomes for the future period closer to 2040. The results here also represent results for a similar level of reliability as that which has just been recommended by the Reliability Panel.

On the right hand axis – it shows the average ‘depth’ of an event i.e. how much demand is lost during an event – the higher up the chart the dot is the more load is lost in this simulated event - you can think of that as more customers impacted.

On the bottom axis it shows how long an event is – so how long are customers experiencing outages.

You can see from looking at the plot and the different colour that South Australia – the yellow – typically has fewer events – there are less “dots” than other colours; their events are also typically shorter and deeper as they are clustered to the bottom left hand quadrant.

In contrast, NSW – the lighter blue – has much longer events – people are out of supply for longer but fewer people are affected and the events are ‘shallower’.

This shows that estimates of unserved energy events – where customers would be without supply - differ by region - in how often they occur, how deep they are, and how long they last. This is driven by the different characteristics of each region – in both generation mix and demand profile.

Some events are short and sharp. Others are longer and shallower.

And different risks call for different forms of flexibility.

If I talk about batteries: fast-response batteries can be well suited to shorter events and intraday ramps, so say, in South Australia.

Longer-duration storage becomes more valuable when tight supply conditions stretch over several hours, so in some of those events towards the right hand side of the chart.

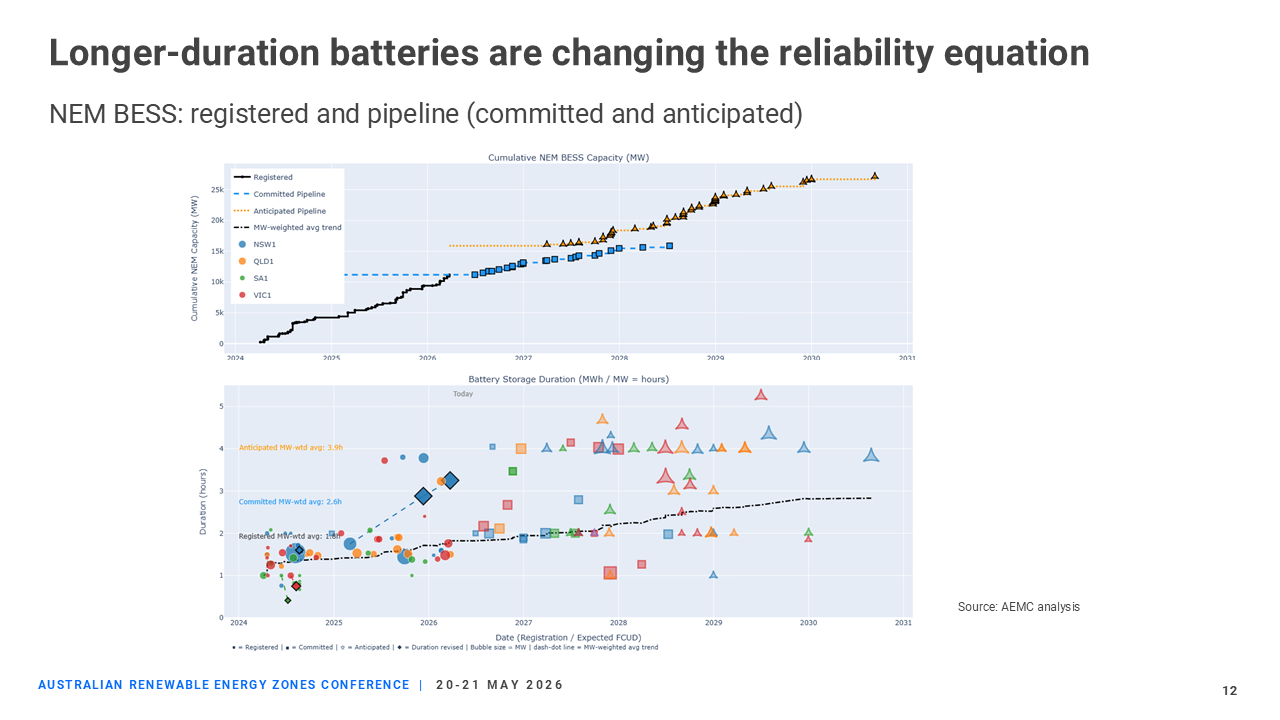

This battery duration chart adds the next part of the story.

It shows a significant pipeline of storage projects (while recognising that not every project in that pipeline may proceed).

It also shows a clear trend: battery duration is increasing over time.

There are already major projects operating, being upgraded, and planned with longer duration.

Because a weather-dependent system does not only need fast response. It needs resources that can move renewable energy across the timeframes where reliability risk actually emerges.

For REZs, this is the practical point:

batteries can absorb renewable generation when output is high or network capacity is constrained

they can hold that energy for later periods of system need

and they can help get more value out of shared REZ infrastructure.

So as reliability risk becomes more duration-dependent, battery duration becomes a reliability issue - not just a project design feature.

The final piece in understanding the role of batteries in the system – and so REZs - is weather.

In the system we are building, reliability risk is increasingly shaped by weather-driven variability.

That is because renewable supply is weather-dependent - and demand is weather-sensitive. We have supply that is impacted by the amount of sun and wind; and in a climate of extremes our demand for electricity is also triggered by the weather – hotter days call for air conditioning; cooler days for heating.

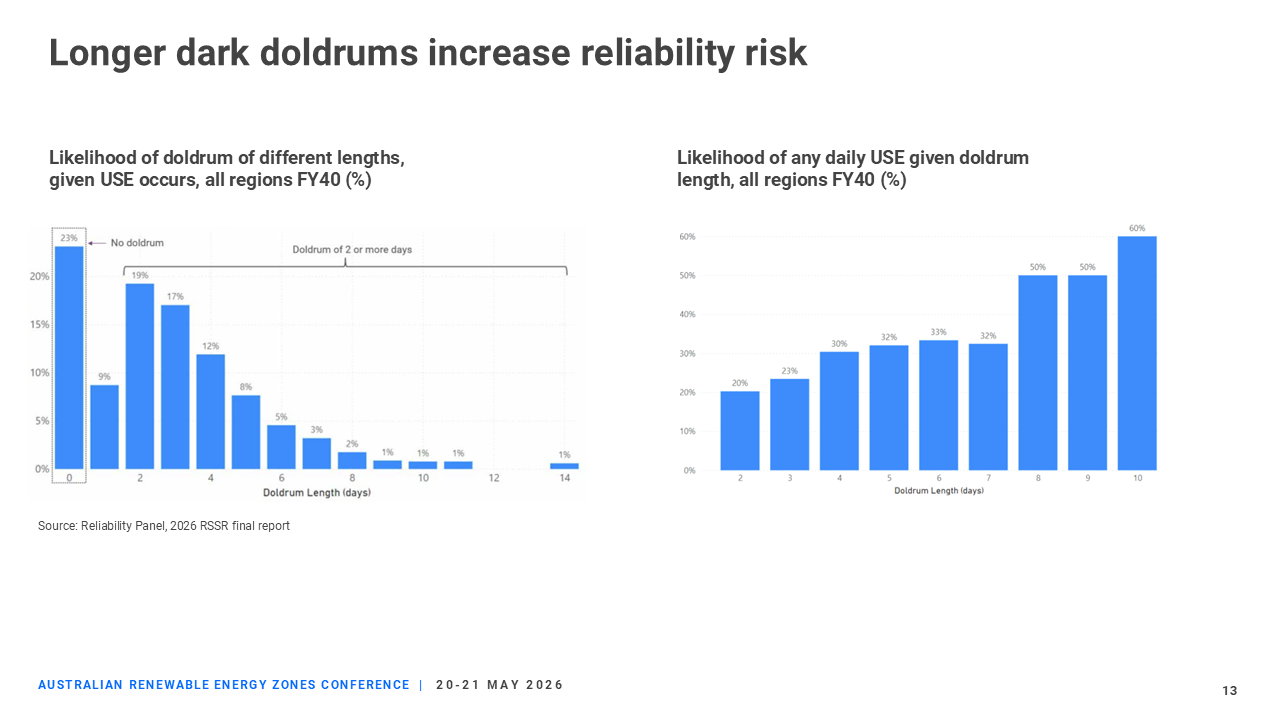

An obvious example we often talk about is the risk of so-called dark doldrums.

The term is used in different ways, but here we are using it to mean periods of two or more days where daily variable renewable generation is very low.

The important point is not that every dark doldrum causes unserved energy.

The Panel’s modelling found that dark doldrums are a significant contributor to unserved energy outcomes, but they are not the only driver. Other factors matter.

Still, the relationship is important: The longer a dark doldrum lasts, the more likely it is to be associated with daily unserved energy, which is what this chart shows.

While doldrums are highly correlated with USE (two-thirds of USE events occur during a doldrum), a doldrum is certainly not a guarantee that USE will occur, as more than half of doldrums in the modelling did not produce any USE.

It is that these conditions show why we need a deeper understanding of weather-driven risk.

Common industry practice is to model reliability using a set of historical weather reference years.

That is useful, but a small sample can miss the wider range of plausible conditions.

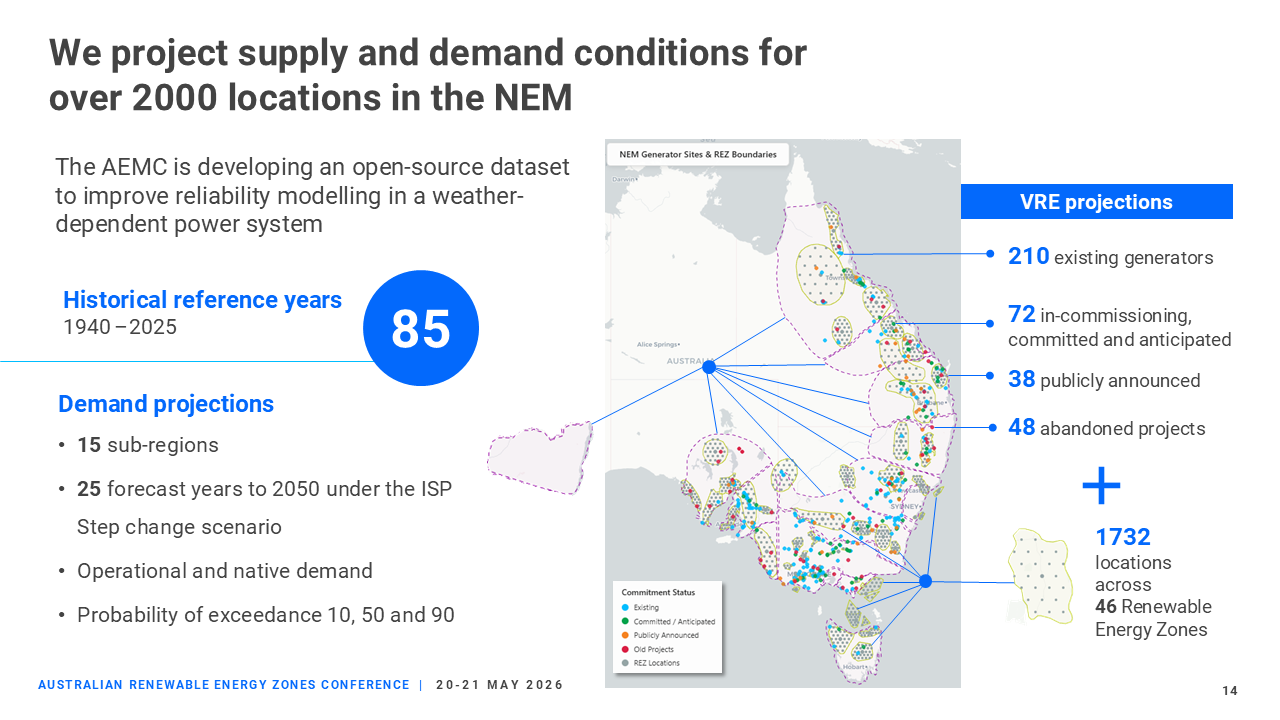

So the AEMC is developing a much larger 85-year set of weather reference years for both supply and demand.

The dataset uses historical reanalysis weather data to generate normalised wind and solar output for more than 2-thousand locations across the NEM, from 1940 to the present.

That includes existing, committed and anticipated generators, and up to 25 points within each proposed REZ.

The aim is to publish this open source, so researchers, modellers and policymakers can better understand reliability risk in a weather-dependent power system.

For REZs, better data helps answer the questions that really determine value.

How often does renewable output fall across a zone?

How does that line up with demand?

Where does storage provide the greatest benefit?

And how can batteries, networks and renewable generation be planned together rather than as separate pieces?

That is the bigger message.

Batteries are not just another technology connecting to the system.

They are becoming part of how the NEM integrates renewable energy, manages reliability risk, and prepares for the system security challenges that come next.

Implications for system strength

Which brings me to the next part of my story.

Because for REZs, there is another part of the transition that is just as important.

It is the question of what keeps the power system stable as the generation mix changes.

For most of the NEM’s history, system security came bundled with the large synchronous machines that generated electricity.

As those plants retire, or run less often, we need to replace not only their energy, but also the stabilising services they provided.

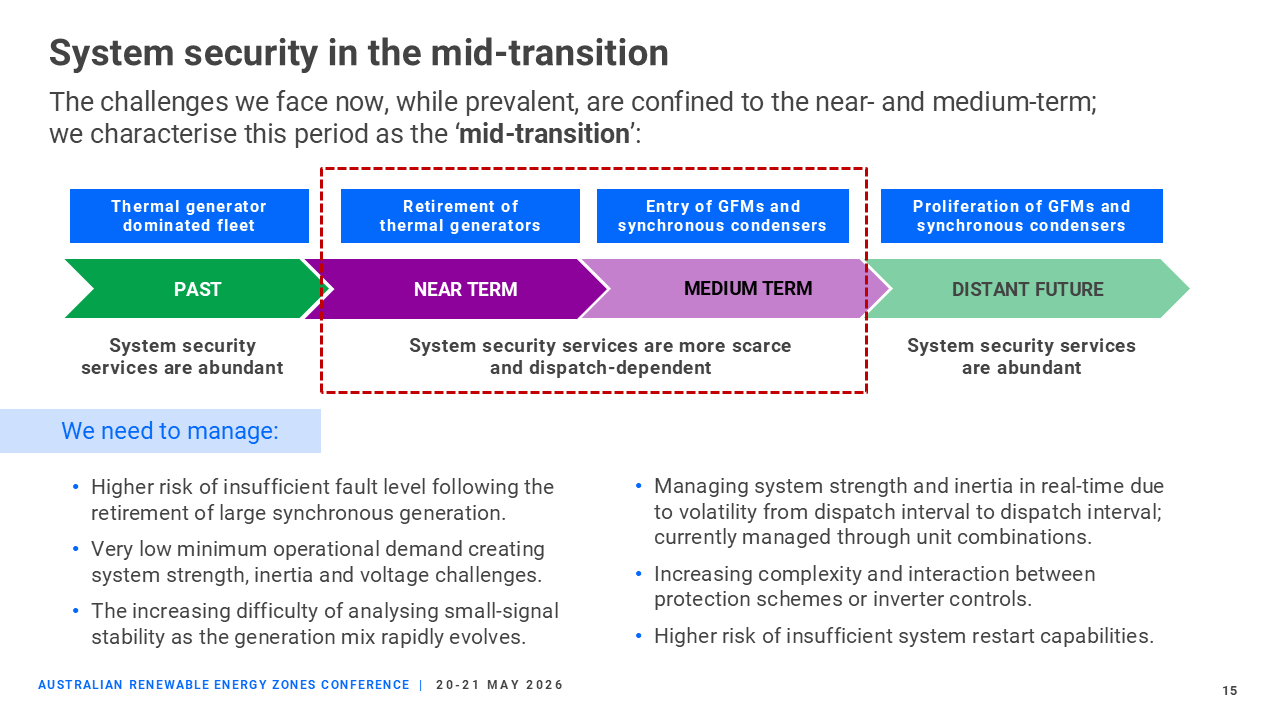

That is the challenge of what we sometimes call the mid-transition.

We are no longer in the old world, where many of these services came almost automatically from the generation fleet.

And we are not yet in the future world, where new technologies are fully embedded across the system and the operational arrangements are mature.

We are in the middle.

And in that middle period, system security services can become more scarce, more location-specific, and more dependent on what is online at any point in time.

That is especially relevant for REZs.

REZs are essential to connecting the renewable generation and storage we need. But they also involve large volumes of inverter-based resources connecting in particular parts of the grid.

So the question is not only: how quickly can we connect new generation?

It is also: how do we make sure that generation connects into a system that remains secure and stable?

A key concept is system strength – the ability of the grid to maintain stable electricity signal both in normal operation and after a disturbance.

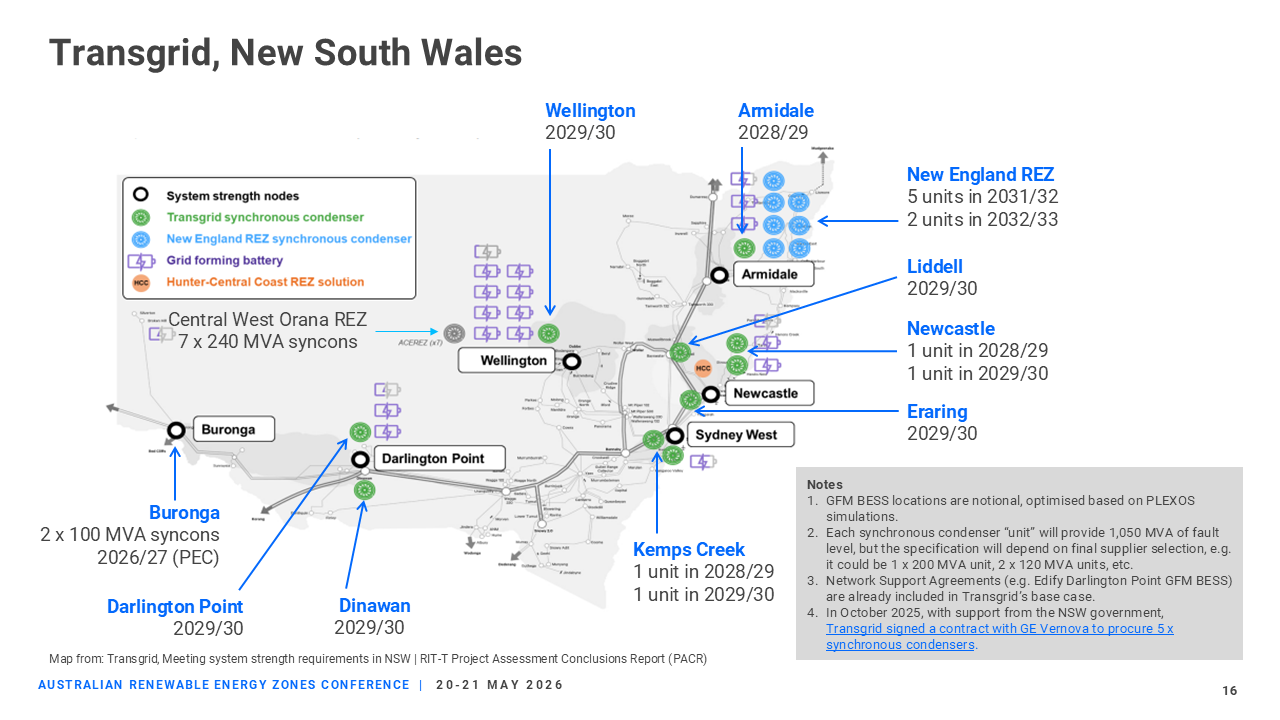

A key example of how batteries can play a role in this is in the recent RIT-Ts run by TNSPs to meet system strength standards.

Transmission networks are planning and procuring a mix of solutions to meet system strength needs.

Synchronous condensers remain important, particularly where strong fault-level support is needed.

Existing synchronous generators also continue to play a role.

In some cases, gas-fired plant can be fitted with clutches so it can operate in synchronous condenser mode - providing system strength without generating electricity in the usual way.

And grid-forming batteries are now clearly part of the portfolio.

If you look at this slide for example, it shows the system strength planning solutions in NSW. You can see that it includes grid-forming batteries as part of the solution set.

That points to a broader change in how system security is being managed.

Services that were once largely incidental to the generation fleet now need to be identified, planned and delivered more deliberately.

There is unlikely to be a single answer:

sometimes the efficient solution will be a synchronous condenser

sometimes it will involve contracting with an existing synchronous unit

sometimes it may involve a gas turbine operating in synchronous condenser mode

and increasingly, it may involve a grid-forming battery.

The point is not that one technology wins everywhere (TNSPs generally plan to use all these options).

It is that the framework needs to allow the right technology to provide the right service in the right location.

If a battery can provide multiple services from the same asset - storing energy, responding quickly to disturbances, supporting frequency and contributing to system strength - it can help reduce the need to procure each service separately from dedicated assets.

But we also need to be clear-eyed.

Grid-forming technology is maturing, but we are still learning and there are still many engineering questions that must be addressed.

Can these batteries provide the right quality of fault current?

Can they support protection systems?

How should their performance be specified?

And how do we make sure system operators can rely on them when the system is under stress?

These questions go directly to how we connect and operate REZs safely.

This is where the AEMC’s work comes in.

Our role is not to pick a preferred technology.

It is to make sure the regulatory frameworks can support the services the system needs efficiently, transparently and at the right time.

To finish, I want to come back to my central point: batteries are no longer sitting at the edge of the transition. They are becoming part of how the power system is planned, operated and secured.

This is especially the case for REZs.

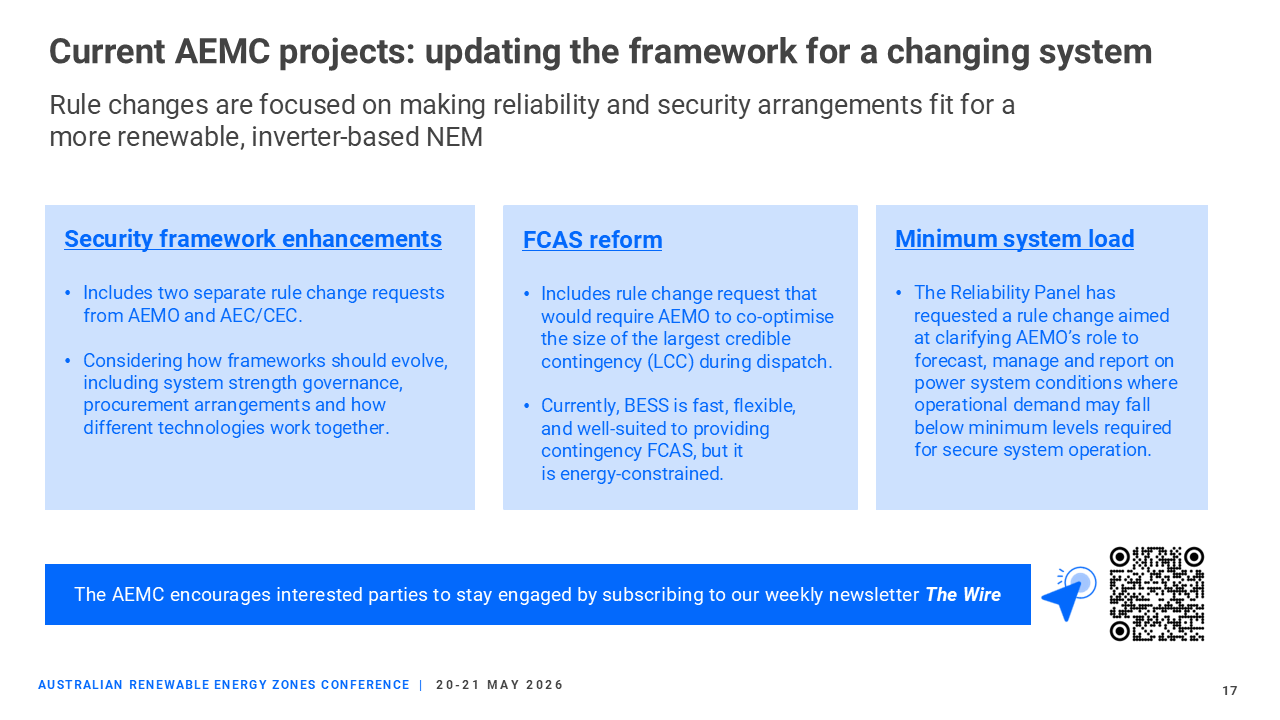

The AEMC has a number of current rule changes that go directly to the issues I’ve discussed today.

While these are not specific to REZs, many of the lessons learned can be applied to them, so we encourage anyone who’s interested to stay engaged and apply lessons learned.

Our Security framework enhancements rule change is looking at how we evolve the current system strength frameworks to be more fit for purpose in future, including how different technologies work together.

We’ve received two rule change requests that ask us consider how existing arrangements and TNSP obligations for procuring system security services can be strengthened, particularly in light of learnings from the first rounds of TNSP RIT-Ts for system strength. Consultation on our first round has just closed; we’re thinking through how best to progress these.

We are also progressing FCAS reforms including a proposal to co‑optimise the size of the largest credible contingency during dispatch. While NEMDE co-optimises bids across the energy and FCAS markets, it does not always operate central dispatch with the objective of optimising the size of the largest contingency relative to the costs of procuring FCAS to manage frequency risk.

This is important to consider in the context of the changing generation mix. For example, the implementation of multi GW REZs may change what the largest generation contingency size is in future. Our draft determination is due on this next month.

And the Reliability Panel has recently submitted a minimum system load rule change request aimed at clarifying AEMO’s role in forecasting and managing minimum system load conditions, while strengthening price signals so the market has a clearer incentive to increase demand when the system needs it. We anticipate initiating this shortly.

So my final message is this: The next stage of REZ development is not just about connecting more renewable generation.

It is about building parts of the power system that can operate reliably and securely as the generation mix changes.

Batteries will not do that alone. But they are becoming one of the technologies that can help turn REZs from places where renewable generation connects, into places where the future power system is built.

Thank-you again.