What’s happening with wholesale prices?

by Ryan Esplin, Economist

Vanty Tang, Economist

Oliver Nunn, Senior Economist

With the restrictions to address the coronavirus pandemic having been in place for almost a month, it seems an opportune time to examine recent outcomes in the electricity market. In this short article, we examine recent spot and contract price outcomes, and the potential drivers of these outcomes: reductions in electricity demand, and a fall in domestic gas prices.

Spot prices are liquidating at their lowest levels in several years

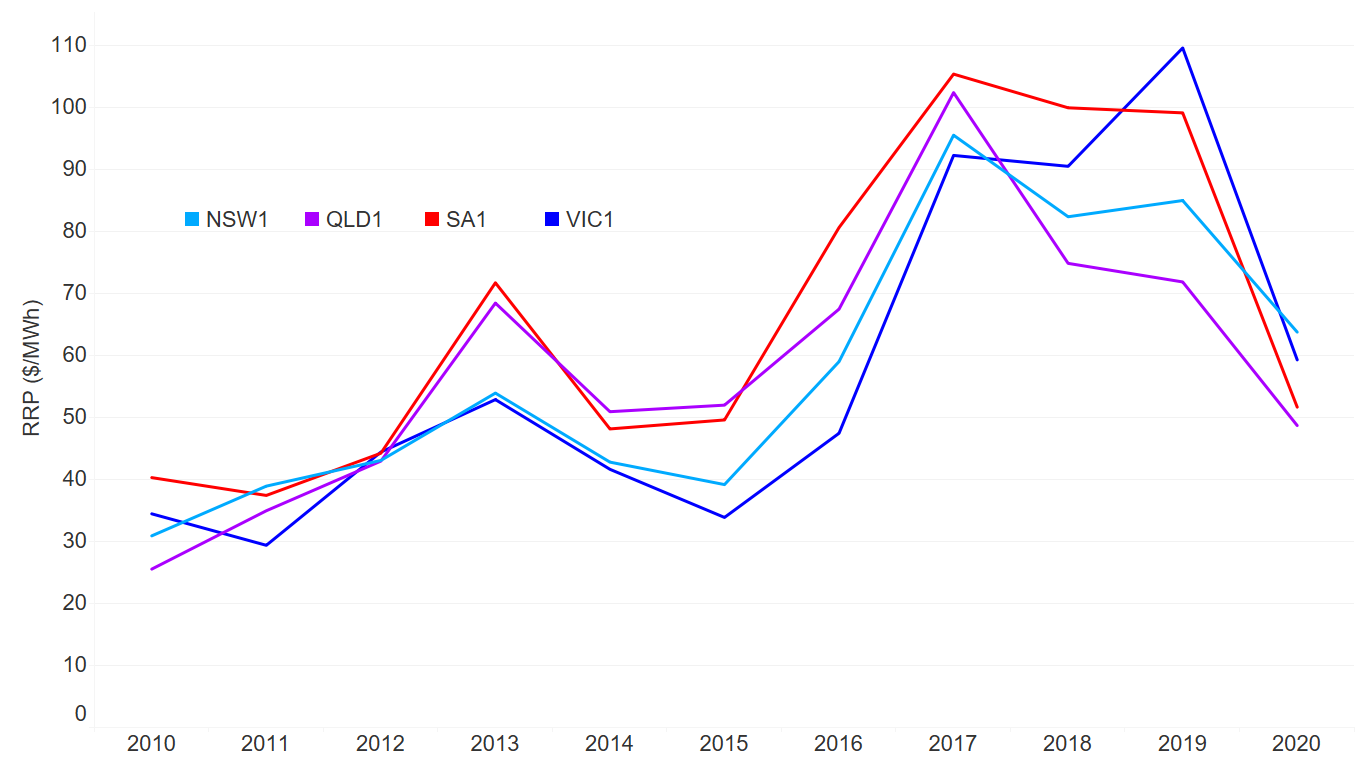

Figure 1 shows annual time-weighted regional reference prices (RRP) by national electricity market (NEM) region from 2010 to 2020, where the 2020 value is given by the contract price for calendar year (Cal) 2020 as at 31 March 2020. Despite there having been a number of high price events in New South Wales and Victoria, spot prices have been liquidating at levels not seen since prior to the closure of Hazelwood.

Figure 1: Annual time-weighted prices by region, 2010 to 2020*

Source: AEMC analysis of AEMO and ASX data

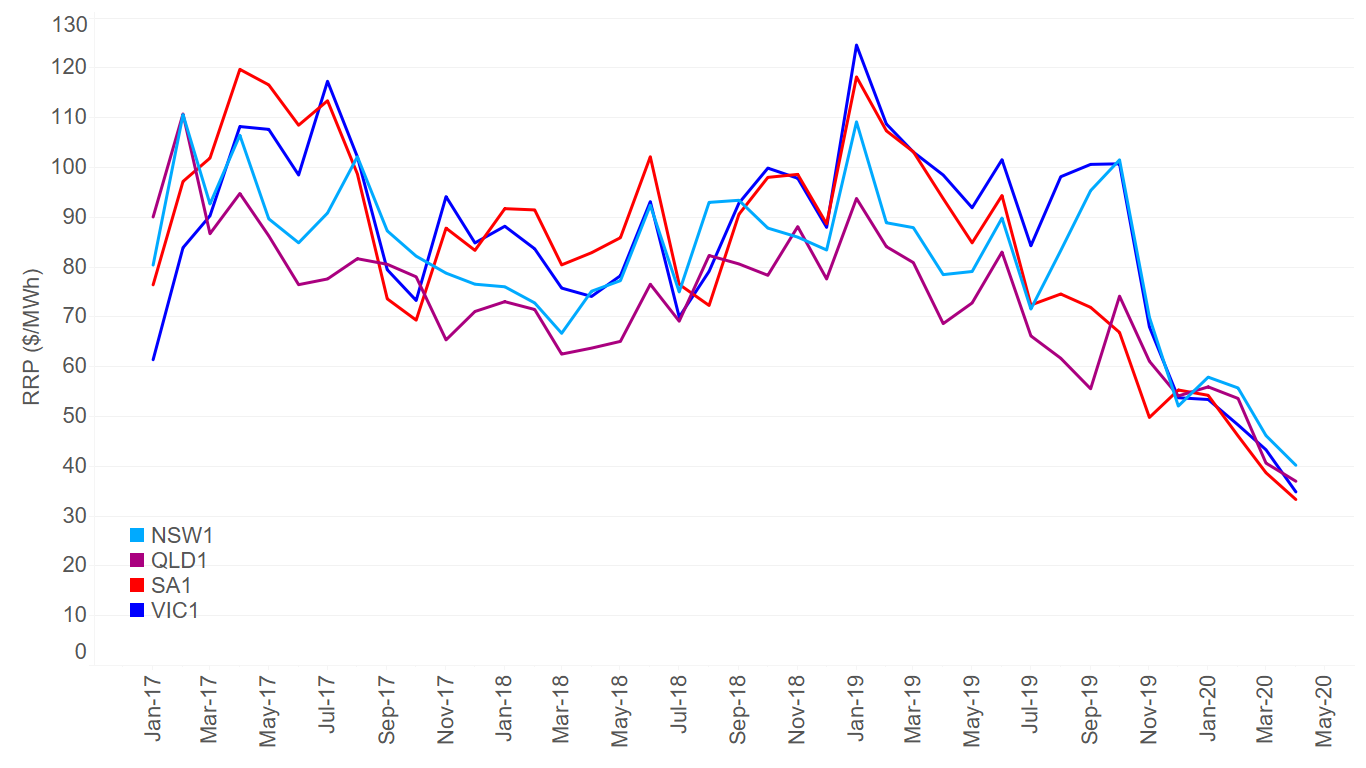

Importantly, this was a trend that was emerging prior to the COVID-19 restrictions. Figure 2 shows monthly average underlying (sub $300 per megawatt-hour prices) from January 2018 to April 2020 for all regions. These underlying prices exclude the effect of short periods of supply scarcity when wholesale prices are very high and give an indication of the supply-demand balance that prevails for the vast majority of the time. The last three or four months have seen the lowest underlying prices across all regions in years.

Figure 2: Monthly average underlying (sub $300) prices, January 2018 to April 2020

Source: AEMC analysis of AEMO data

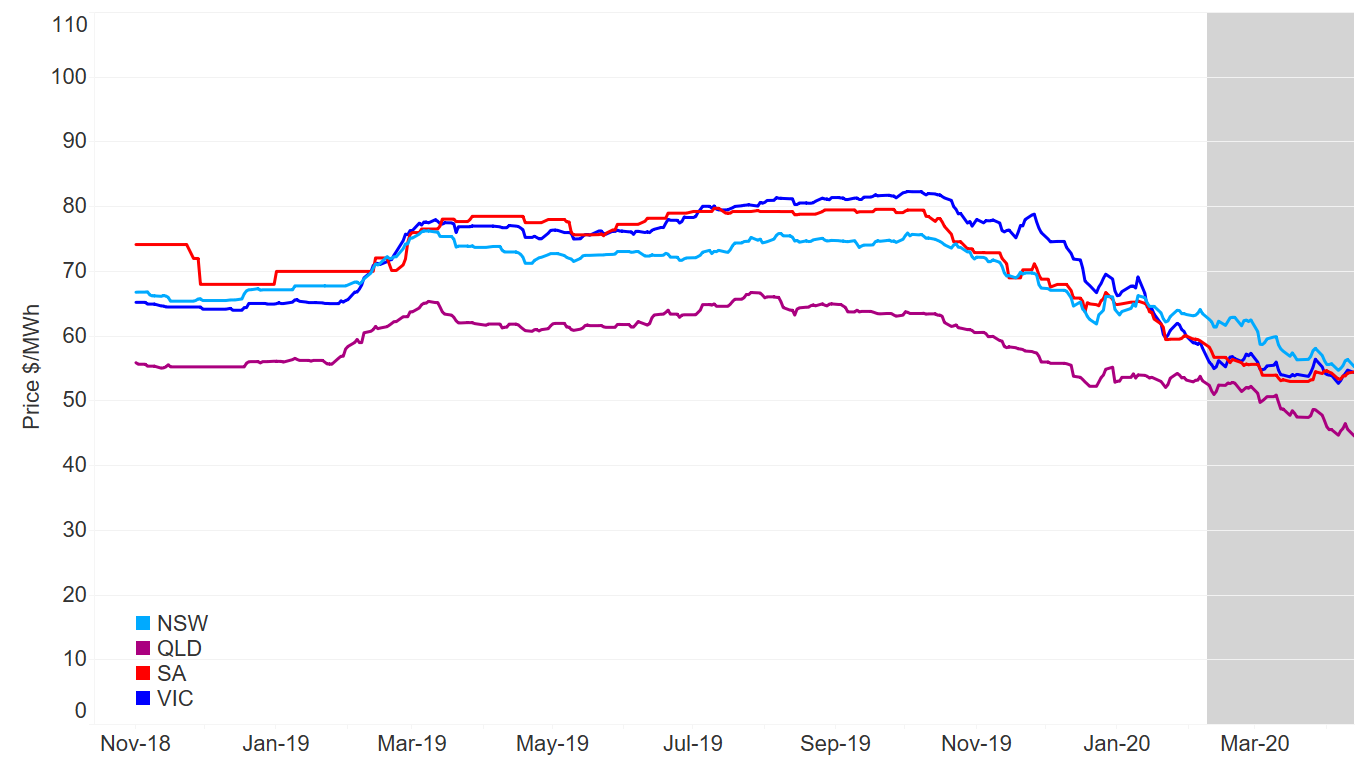

This trend is also borne out in futures prices. Figure 3 shows that over the past six months, Victoria flat swaps for calendar year 2021 have fallen from around $82 per MWh to $55 per MWh – a decline of 33 per cent. We have also seen large declines in other regions. This decline was already underway prior to the COVID-19 restrictions. What has driven this significant shift in the price of electricity?

Figure 3: Daily CAL2021 contract prices, 04 November 2018 to 04 May 2020

Source: AEMC analysis of ASX data

Despite the hype about COVID-19, it is not a major driver of falling demand

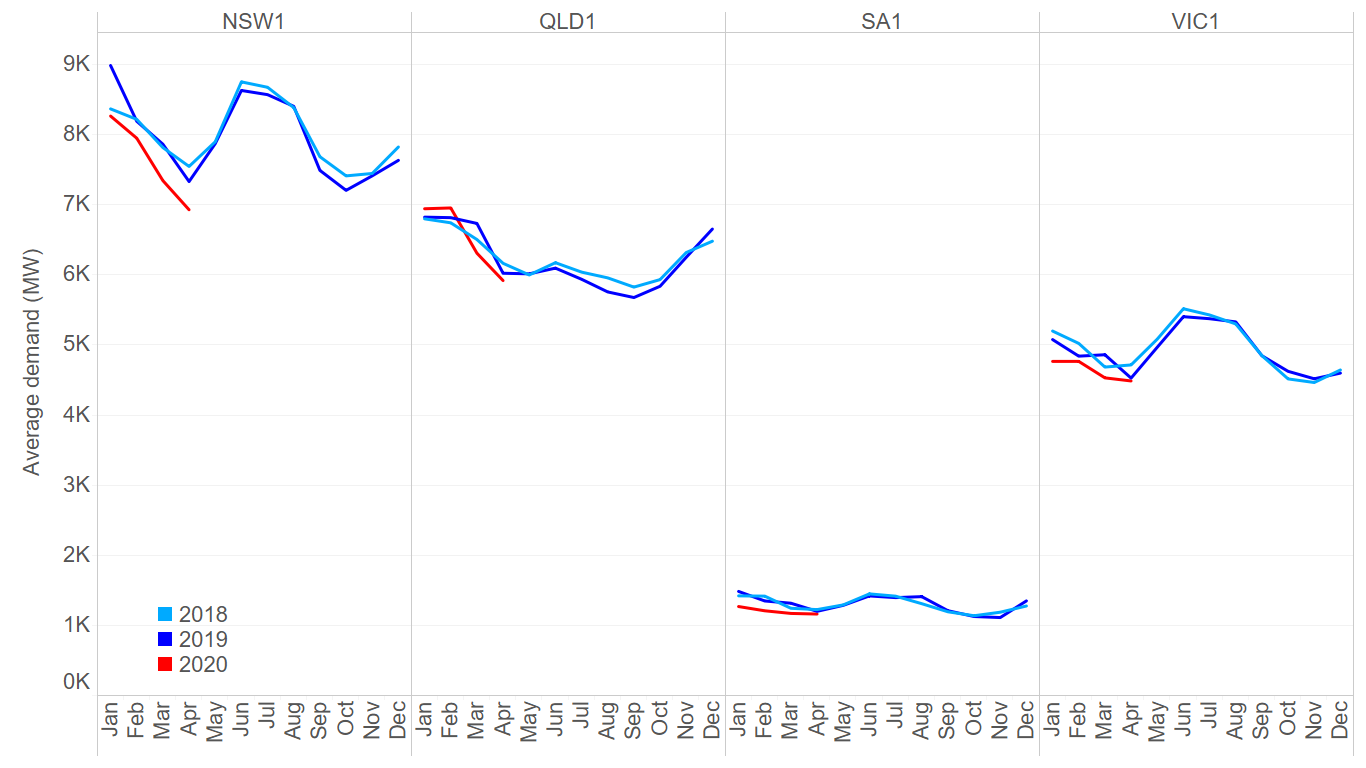

Whenever we see marked changes in spot prices, an obvious driver to consider is falling demand. And demand has been falling – see Figure 4, which shows monthly average demand for each major NEM region from January 2018 to April 2020. Although there has been a great deal of focus on the very low demand outcomes seen in March across the NEM, we can see from the Figure that this was merely the continuation of a trend of declining demand that has been apparent for most of quarter 1. We expect that the COVID-19 restrictions have exacerbated the low demand outcomes in March and April, but to date the effect appears to have been limited.

Figure 4: Monthly average demand by NEM region, 1 January 2018 to 30 April 2020

Source: AEMC analysis of AEMO data

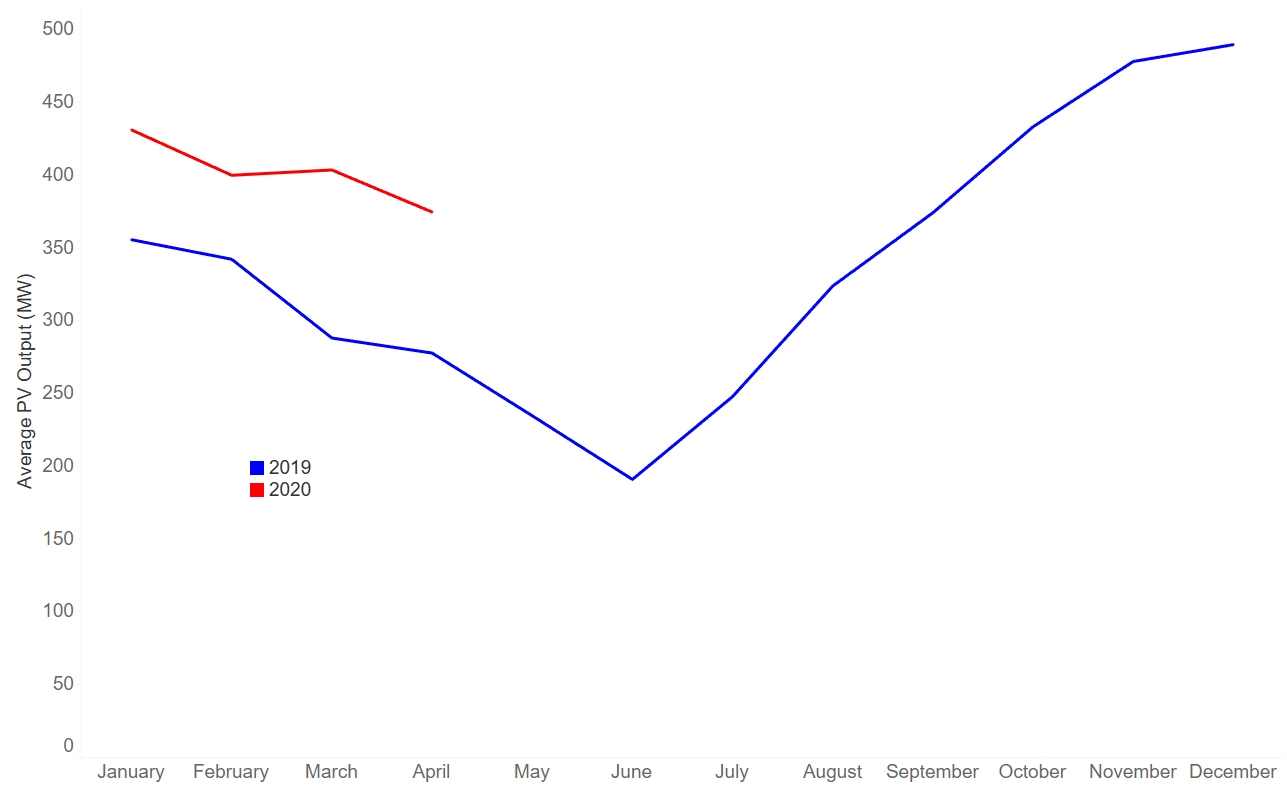

Our internal analysis suggests that much of the decline in demand versus 2019 is attributable to increased uptake of behind-the-meter solar PV over the last year. Figure 5 shows average monthly rooftop PV output for New South Wales in 2020 was significantly higher than for the first four months of 2019.

Figure 5: Average monthly rooftop PV output in New South Wales

Source: AEMC analysis of AEMO data

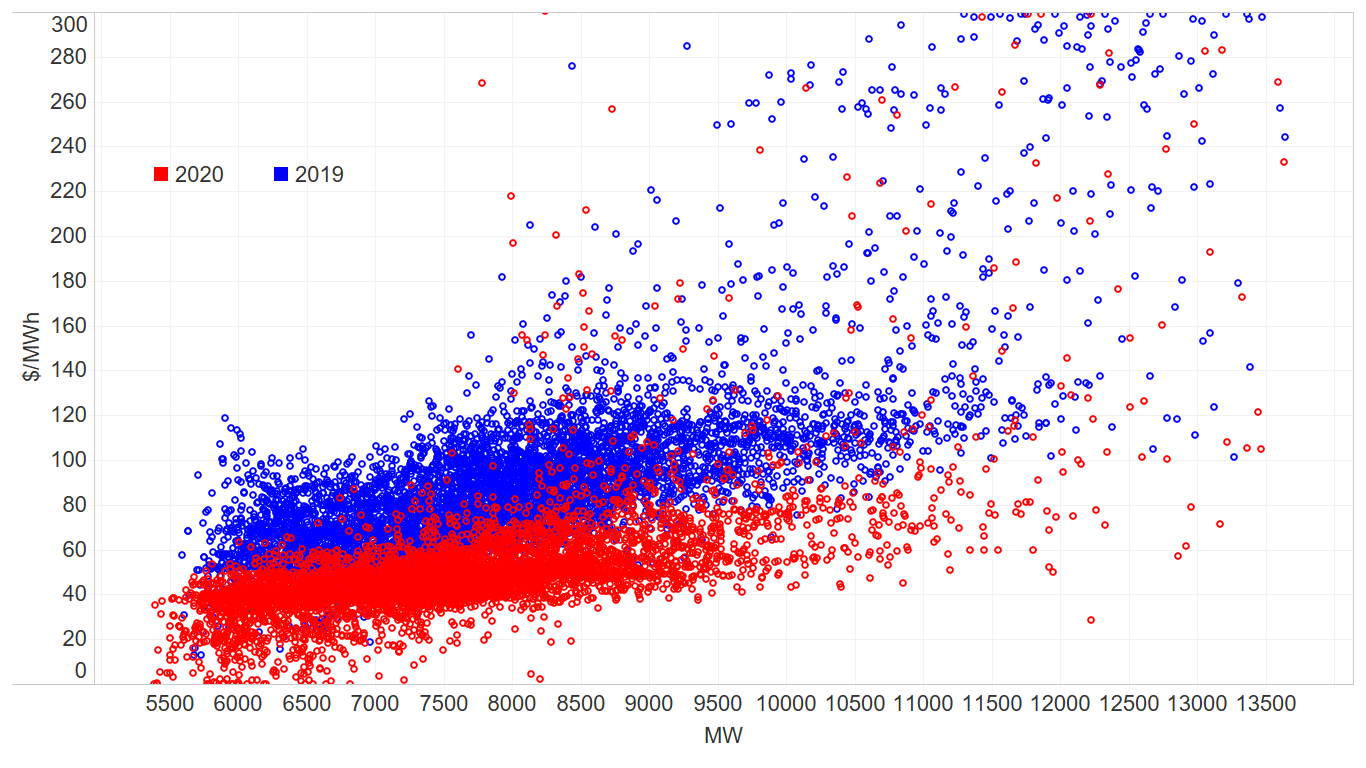

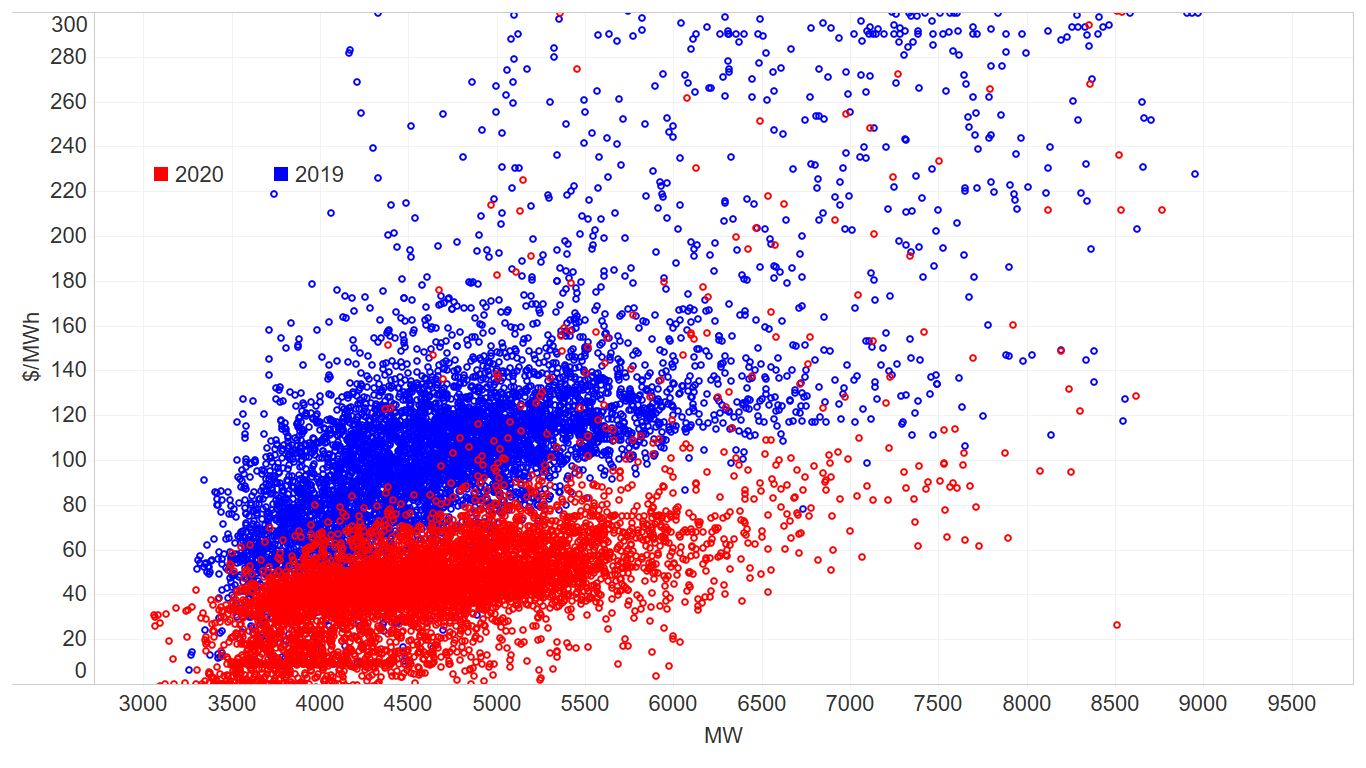

But whatever the cause, is the decline in demand responsible for the marked decrease that we have seen in underlying spot prices? Figures 6 and 7 help answer this question – they show the relationship between prices and demand for NSW and Victoria. We have confined the comparison to the period from 1 January to 05 May for 2019 and 2020. By way of explanation:

- the horizontal axis shows the observed level of demand in the region;

- the vertical axis shows the observed price in the region;

- each dot represents the outcome for a single trading interval (30 minutes);

- outcomes for 2019 are shown in blue, and outcomes for 2020 are shown in red; and

- we have restricted the chart to prices between $0 and $300 per MWh to avoid the results being dominated by extreme price events.

These two figures show that for any given level of demand, prices have fallen markedly. For example, as shown by Figure 6 in NSW at 8000 MW of demand, prices have dropped from somewhere in the range of $60 per MWh to $120 per MWh in 2019, to somewhere in the range of $30 per MWh to $60 per MWh. We can see a similar shift for Victoria in Figure 7. Given that the demand curve is relatively inelastic, this means that the majority of the change must be explained by a shift in the supply curve. So what is driving this change in the supply curve?

Figure 6: Price versus demand by trading interval for NSW, 1 January to 5 May, 2019 versus 2020

Source: AEMC analysis of AEMO data

Figure 7: Price versus demand by trading interval for VIC, 1 January to 5 May, 2019 versus 2020

Source: AEMC analysis of AEMO data

The major driver of falling prices appears to be a collapsing gas price

The fall in spot and forward electricity prices can be largely explained by the fall in the domestic gas price. Gas prices impact upon wholesale electricity prices through at least two channels:

- First, lower gas prices reduce the short-run marginal cost of gas-powered generation (GPG) directly, which reduces the prices that these units are bid into the market.

- Second, the lower bidding of GPG units causes other forms of generation, notably coal and hydro, to increase their capacity bid at lower price bands.

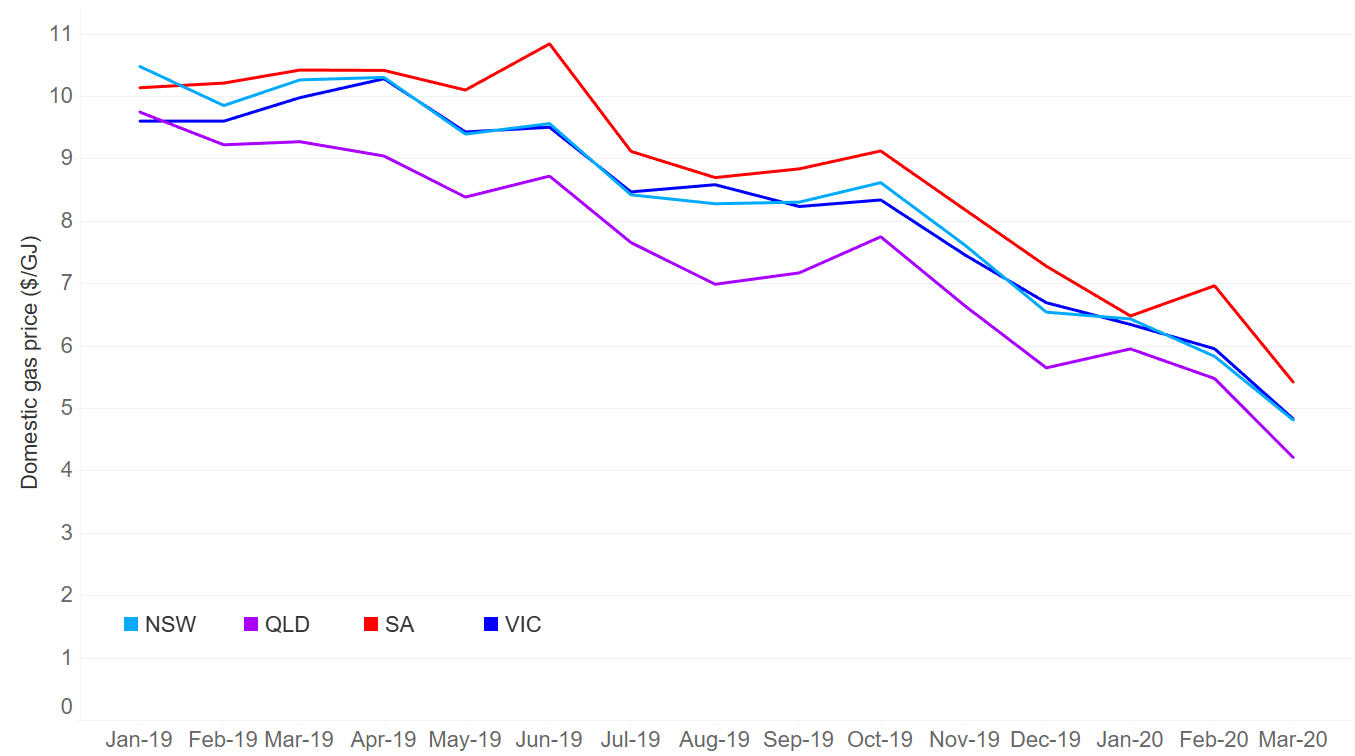

As can be seen in Figure 8, domestic gas prices have been falling since July 2020 following a global supply glut of Liquified Natural Gas (LNG) which pushed down the LNG netback price (this is the price that exporters can earn for exporting gas). As of March 2020 average domestic gas prices are around $5/gigajoule (GJ) which is about 50 per cent lower than average prices at the beginning of 2019.

Figure 8: Domestic gas prices

Source: AEMO Gas Bulletin Board

Low gas prices are expected to remain low in the short-term due to high levels of gas production in Queensland and lower gas demand domestically and abroad due to the COVID-19 pandemic.

However, it should be noted that while gas spot prices are soft, contract prices have not fallen as far. Quarterly ASX futures prices for gas in Victoria have eased from around $10/GJ to around $6-8/GJ over the past 6 months. Unfortunately, there is limited publicly available data on recent bilateral contracts whereby most gas is traded but conversations with industry analysts suggests that multi-year contract prices have not fallen as far as spot prices and in the longer-term are expected to be above the marginal cost of production. More information on recent gas contract prices is expected in future ACCC gas inquiry reports.

As noted in AEMO’s Gas Statement of Opportunities, there are also concerns about the gas supply outlook from the mid-2020s in the southern states. If the supply-demand balance were to tighten then we would expect that the recent low in gas prices will not persist.

The future interplay between the pandemic and the electricity market remains unclear

We have shown that, at least to date, the pandemic has had a relatively muted impact on demand. The pandemic does appear to have exacerbated a trend toward lower gas prices, that was already underway throughout the second half of 2019.

But the effect of the pandemic may evolve in the coming months. Demand may in fact be eroded as trade-exposed businesses face a sharp downturn in global economic activity. Another consideration is how the pandemic will affect maintenance schedules, as participants defer or limit maintenance in response to challenges obtaining parts, and access to international and local labour.

A final consideration is how the pandemic will affect investment, particularly in new renewable projects. Our discussions with major investors suggest that construction risk is now a major factor in their decision making.

In conclusion, our power system and energy markets are currently coping well with the many challenges arising from the coronavirus pandemic, but it is still early days. But just as there is a need for Australia to remain vigilant in its response to the pandemic, so too is there a need for all who work in the energy sector to maintain a close watch for changes and emerging challenges.