The value of dispatchability in the NEM

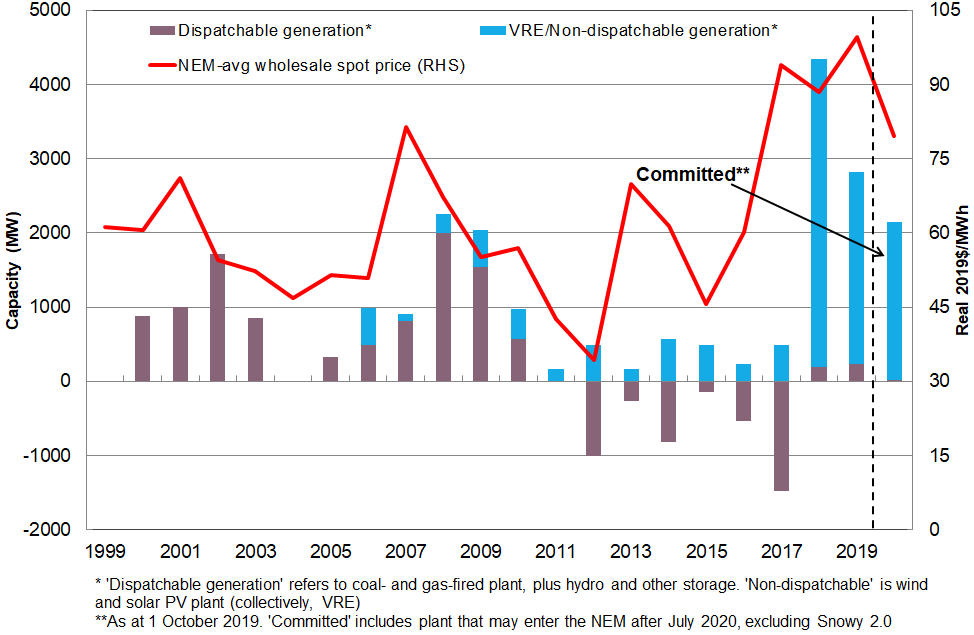

The COAG Energy Council has tasked the Energy Security Board (ESB) with developing advice on a long-term, fit-for-purpose market framework to support reliability that could apply from the mid-2020s. The design of the wholesale electricity market is a key area of focus within this advice, given the lack of entry of ‘dispatchable’ capacity (which includes gas-fired generation, hydro plant, and battery storage) into the NEM since 2017 despite record high prices (see below figure).

One of the potential reasons cited for this lack of entry is that the National Electricity Market (NEM) does not currently value “dispatchability”. While the term “dispatchability” does not have a universal meaning, it is commonly considered as the extent to which the resource (i.e. demand or supply resource) can be relied on to ‘follow a target’ in relation to its load or generation. “Dispatchability” therefore incorporates notions of controllability and flexibility.

One of the potential reasons cited for this lack of entry is that the National Electricity Market (NEM) does not currently value “dispatchability”. While the term “dispatchability” does not have a universal meaning, it is commonly considered as the extent to which the resource (i.e. demand or supply resource) can be relied on to ‘follow a target’ in relation to its load or generation. “Dispatchability” therefore incorporates notions of controllability and flexibility.

In recent published work, Oliver Nunn and I argue the NEM does value dispatchability. This value is not as transparent in the NEM as it is in other electricity markets, which may be a potential reason why the NEM’s ‘dispatchability premium’ is not as obvious.

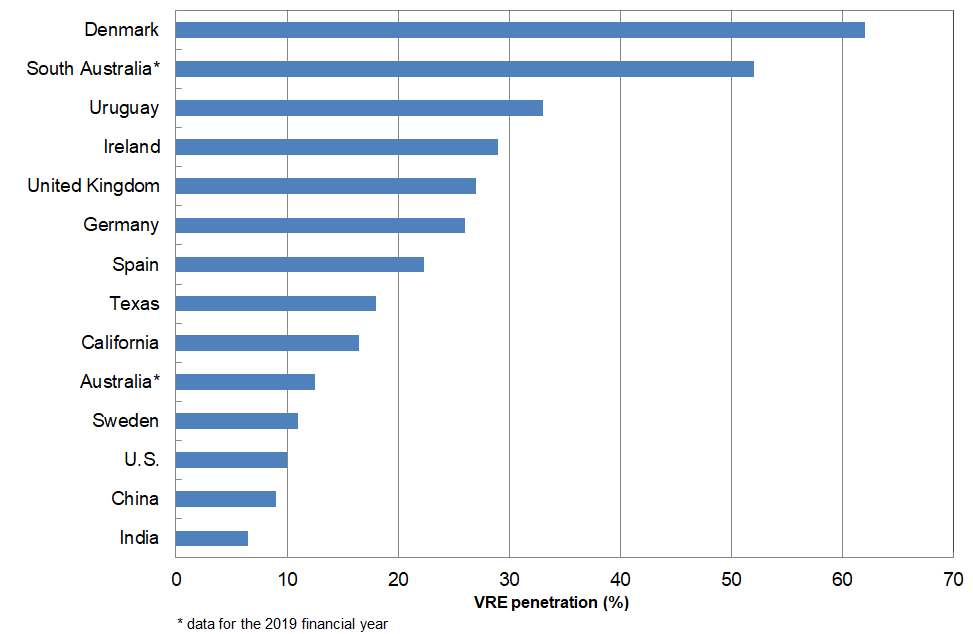

We calculate this premium as the difference between the dispatch-weighted prices received by non-dispatchable and dispatchable generators. South Australia (S.A.) is a good region to conduct this analysis as S.A. has one of the highest utility-scale penetrations of utility-scale variable renewable energy (VRE) – chiefly, wind and solar PV – globally (see below figure).

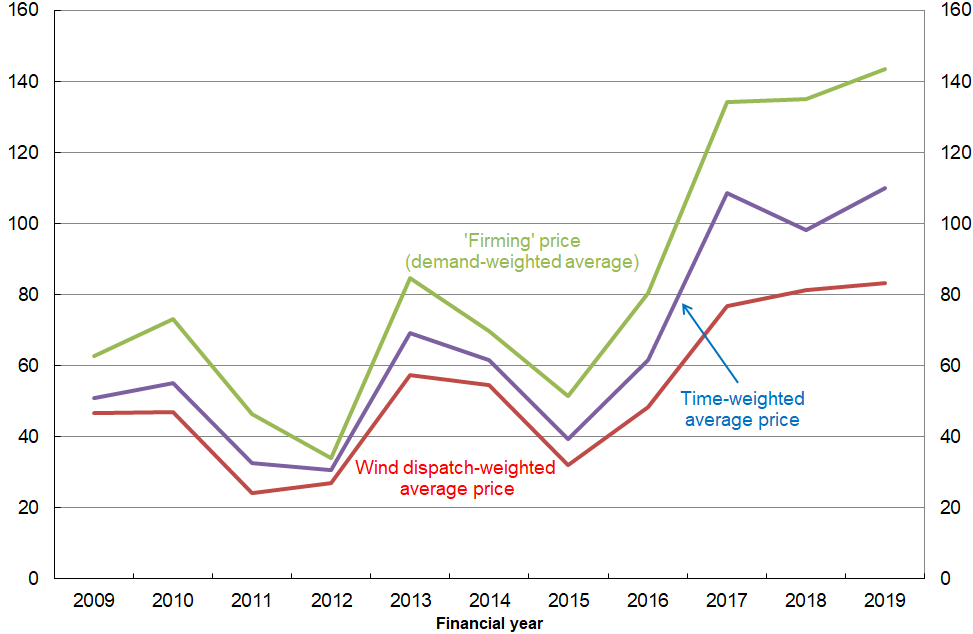

The dispatchability premium in S.A. has averaged around 70 per cent since 2016, with this premium more than doubling between 2014 and 2019 (see the below figure).

As we detail in our paper, this increase in the dispatchability premium is an expected result, given the increasing penetration of VRE and the weak correlation between VRE output and demand.

This suggests the lack of entry of dispatchable capacity is not due to a lack of a dispatchability premium. Instead, as we discuss, it is likely due to a range of other entry barriers, including the risk of asset stranding due to uncertainty on emissions reduction policy and technology risk. Managing these risks, and ideally overcoming them, remains a front-of-mind issue for the AEMC and for other policymakers.