Profiling the capacity market debate

Australia’s national electricity market is already integrating capacity market mechanisms – but global debates on how to deliver long-term reliability in systems powered by renewables say the missing link is properly integrated government policies

By Greg Williams

Senior Economist – Strategy and Economic Analysis

Consumers in Australia’s national electricity market (NEM) have always enjoyed a high level of power supply reliability delivered by well-designed and responsive market mechanisms. Government policy at federal and state levels have separately been very effective in driving massive penetration of new technology generators, particularly wind and solar, into the system. Today, reflecting the scale of the technology revolution in the NEM, there are widely held concerns about the performance of the wholesale spot market in recent years - concerns that:

- the transition is happening too fast or too slow, depending on your point of view, but will in any case hasten the retirement of the remaining coal-fired power stations, despite an obligation in the rules for generators to provide over three years’ notice of closure

- wholesale prices in recent years have been unusually high as increasing penetration of variable renewable energy (VRE) has induced the retirements of the first few coal-fired stations (most notably Hazelwood in 2016)

- spot prices will become increasingly volatile as the transition continues, making it more difficult for investors to appropriately time their investment in technologies (eg gas turbines, demand response, storage technologies such as pumped hydro, chemical batteries) that run profitably only when VRE output is low (and high in the case of storage).

Two well-trodden paths to achieve adequate reliability

There are two well-trodden paths taken by electricity market designers to coordinate investment so it is sufficient to achieve reliable levels of supply.

The price-driven approach is employed in Australia by the national electricity market (NEM), in the United States by the ERCOT (Texas), New Zealand, Singapore, and in Canada (Alberta). In summary, it consists of:

- setting a market price cap at a level high enough that any demand curtailment is acceptably low

- regulating forward coordination mechanisms (such as the NEM’s Electricity Statement of Opportunities, Projected Assessment of System Adequacy, Retailer Reliability Obligation) and facilitating forward contracting to reduce the other risks and impact of significant under-investment in resources that would otherwise cause a lower than expected level of reliability.

Thequantity-driven approach is employed by other parts of the US and in some European markets:

You will note in the outline below that Australia’s NEM has already adopted two mechanisms that fall into the quantity-driven approach.

On 1 July 2019, the rules were amended to create the retailer reliability obligation (RRO), which is a similar mechanism to those employed in the California (CAISO) and Southwest Power Pool (SPP) markets and other US utilities and states to manage resource adequacy. The contracts struck by load serving entities create must-offer obligations on resources contracted. Further, the NEM’s operator, AEMO, procures additional capacity via the reliability and emergency reserve trader (RERT) mechanism, which is a type of strategic reserve limited to emergency periods where AEMO considers such resources are necessary to meet the reliability standard. The retailer reliability obligation allocates a share of RERT costs to retailers short of contracts that hedge their share of demand peaks.

In summary, the quantity-driven approach of capacity markets consists of:

- setting the market price cap at a lower value sufficient to recover short-run marginal cost of generators and add penalties for being short of energy or ancillary services at an administered cost of non-supply.

- Choosing one, or more, of the following to cover the fixed costs of capacity sufficient to meet demand:

- a de-centralised obligation: regulate bilateral contracting for resource adequacy (also now employed by the NEM through the retailer reliability obligation, and by the CAISO and SPP markets in the US), by requiring load serving entities (LSEs) responsible for supplying electricity to consumers to cover forecast peak demand plus a reserve margin.

- a central buyer to estimate the combination and location of resources necessary to achieve acceptably low levels of demand curtailment (PJM, New York, and New England markets in the US) and conduct auctions for resource adequacy several years ahead.

- a strategic reserve: additional capacity is contracted (usually by the system operator) and held in reserve outside the market and only operated under specific scarcity conditions (as employed in the NEM, Germany, Belgium, and Sweden).

Australia’s national electricity market employs the price-driven approach

The NEM has a high market price cap by world standards (it is $14,700/MWh for the year ending 30 June 2020), which is set by the Reliability Panel and reviewed at least once every four years. The advantage of this approach is that the spot price is imbued with a reliability or scarcity value high enough to induce generation and demand to match nearly all the time. Wholesale market purchasers (consumers and their retailer agents) and generators manage the cashflow implications of spot price volatility via forward contracts and investment/retirement decisions.

Fundamentally, the NEM and other markets like ERCOT, Alberta and New Zealand all rely on spot prices to drive operational, contracting, and investment decisions by market participants (retailers, consumers and generators). If demand is higher or generation is lower than expected, generators enjoy higher revenues (or experience a financial cost if they fail to deliver fixed quantities agreed in contracts) while retailers are exposed to the potential for higher prices for every unhedged MWh.

The supply/demand balance and competition between firms determine the degree to which prices reflect costs – higher levels of competition and supply drive prices toward short run marginal costs (or below for short periods of time), lower levels drive prices closer to long run marginal costs (and beyond for short periods of time). Investment and retirement decisions prevent prices being below SRMC or above the cost of new entry for more than short periods of time.

The quantity-driven approach employs the same supply/demand model

A quantity-driven approach to managing resource adequacy was standard practice for electric utilities in the last century before digital control and communications systems and the development of markets which have enabled the decentralisation of electricity supply. It has remained largely unchanged and remains a common method in the United States for delivering the required level of reliability (or resource adequacy as it is known there).

In terms of a reliability standard, utilities, system operators, and regulators across North America have relied on variations of the 1-in-10 standard for many decades. For instance, the PJM power pool began in 1927. In order “to prevent any member from free riding on the capacity of other members and not bearing the cost of owning capacity”, the PJM operating agreement “required that each member have capacity, through ownership or contract, equal to its forecasted peak load plus a reserve margin”.

This ‘one in ten’ standard means there is sufficient generation and demand response resources such that system peak load is likely to exceed available supply only once in any ten-year period. The standard is translated into a reserve margin required by the Regional Transmission Organization (RTO) and implemented either:

- as a requirement on load serving entities (equivalent to retailers in the Australian context) to show they hold contracts sufficient to cover their peak demand plus the reserve margin (this is the original method)

- via a capacity auction (an option adopted to pool capacity resources within large interconnections such as PJM).

On the FERC website, there is a report from Brattle Group/Astrape Consulting, Resource Adequacy Requirements: Reliability and Economic Implications, which illustrates the economic and reliability implications of a variety of implementations of the resource adequacy standards.

The report notes that the translation of the standard into a reserve margin depends on how long and how deep the single event is defined – for example, loss of load expectation (LOLE) or loss of load hours (LOLH) or normalised expected unserved energy (EUSE). The difference in interpretation alters the economic reserve margin (RM).

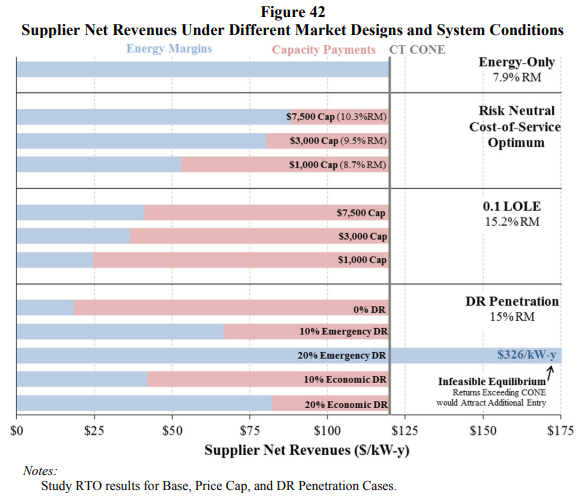

Figure 42 of the report, reproduced below, shows the range of capacity market revenues depends on the market price cap. The modelling results indicate the range of supplier net revenues from energy and capacity markets under different market designs, price caps, reserve margin targets, and demand response (DR) penetration levels.

Source: Brattle Group/Astrape Consulting (2014)

The attraction of the quantity-driven approach

The results in the figure demonstrate that the modelling employed in the US is not much different to that employed by the Reliability Panel here in the Australian NEM. Both are complicated projections of the supply and demand balance and yield results that are imprecise and uncertain, which suggests the concerns about their outcomes should also be similar (and it appears that they are).

One of the attractions of a quantity-driven approach to policy makers is that it reduces concerns about market power and high prices when supply conditions are tight. The quantity-driven approach turns this curtailment of producer surplus above the wholesale market price cap into a penalty on resources cleared in the capacity auction (eg PJM) or contracted by each public utility (eg SPP), much like a cap contract with a strike price at a very high price. This approach is attractive in jurisdictions where policy makers are sensitive about high wholesale spot prices – setting a lower price cap limits the potential for prices to rise far above SRMC when supply is tight and participants have more scope to set prices. The trade-off is that consumer bills include the cost of capacity payments, which may or may not make them better off in the long run.

Another potential attraction of the quantity-driven approach (particularly a capacity market) is that it appears to provide the promise of a more graceful transition to a low emission generation mix. This is because a capacity auction could be designed to calculate the most cost effective mix of resources required three (or more) years in advance, providing the market a firm schedule of generation retirement (ie generation not cleared in a capacity market auction) and making the investment environment more stable.

Concerns the capacity market is artificially slowing the transition

Western Australia’s electricity market has a well-documented recent history of concern about the over procurement of capacity in its reserve capacity mechanism (RCM), which has been acknowledged in the final recommendations paper produced by the Public Utilities Office of the Department of Treasury.

The relatively recent UK capacity mechanism (auctions started in 2014) has been controversial for other reasons. In fact, the UK capacity market was suspended in November 2018 after a ruling from the European Court of Justice concluded the mechanism was in breach of European Union State Aid rules after the appellant, Tempus Energy, argued the market rules discriminated against demand response in the market.

Before it was suspended, Michael Grubb and David Newbery (2018) reviewed OFGEM’s Electricity Market Reform package and suggested the outcomes of the auctions had not worked out as planned as the “government really wanted and expected the capacity mechanism to bring forth large flexible gas-fired generation (which it has not)”.

The government tinkered with the rules after each auction. After disallowing distributed diesel generators from the auction for environmental reasons, it also had to reduce the assumption about the firmness of batteries. Yet prices continued to be below the level to support a new combined cycle gas turbine (CCGT) power station.

In a report typical of the concerns about the UK capacity market, the Institute for Energy Economics and Financial Analysis, made the following statement:

Britain’s capacity market has achieved its goal to assure security of supply, but at a cumulative cost since 2014 of around £3.8 billion (excluding withdrawals from the scheme). The vast majority of these funds (83%) have gone to operators of existing power plants (see Table below). Most of those power plants would have remained available regardless of the scheme. Only 3.5% have been awarded to operators to build new generation.

There are similar concerns with the PJM capacity market, which is the reliability pricing model (RPM), operating in the US. David Kolata, executive director of the Citizens Utility Board in Illinois, has said “the capacity market is ill-suited to a future world of high renewables and zero-carbon power”. He and other critics argue “PJM’s capacity auctions are biased toward larger power plants and don’t offer enough flexibility to states such as Illinois with ambitious renewable goals”.

The FERC website also contains a statement made on 15 April 2019 from Richard Glick, a FERC commissioner, in which he offered a dissenting view on a proposal by PJM Interconnection to adjust a parameter of the RPM, which is PJM’s capacity market. In the statement, Commissioner Glick suggested that “the PJM capacity market has suffered from a chronic oversupply of generation resources” for many years, primarily due to an artificially high cost of new entry (CONE):

An excessive Net CONE distorts the shape of the demand curve that PJM uses in its capacity market, causing PJM to procure too many resources at too high a price, with obvious detrimental consequences for consumers.

But the harm from an excessive Net CONE goes beyond its impact on consumers’ bills. By retaining too many resources, PJM dulls the price signals in the markets for energy and ancillary services (E&AS), impairing their ability to incentivize the services we actually need to reliably operate the grid. A market is only as efficient as the price signals it sends. So long as the flaws in PJM’s capacity market distort the prices throughout the other PJM markets, consumers will pay excessive prices and get a suboptimal resource mix.

And concerns it is happening too fast

The effect of the energy transition on incumbent thermal power stations appears to be as sensitive a subject in the US and European electricity markets as it is in NEM. Below are two examples of concerns about the validity of market outcomes that have moved agencies to try to retain resources that would otherwise be retired.

According to Euractiv (an independent pan-European media network specialised in EU policies), in September 2018, a group of seven European countries issued a common position on the reform of Europe’s electricity market, saying “strategic reserves” for electricity should not receive favourable treatment from regulators.

Germany had considered and chosen not to implement a full capacity market but argued instead that a “strategic reserve” was necessary to accompany the country’s transition to renewables and phase-out from nuclear power. The German scheme received clearance by the European Commission in February under the EU’s state aid rules. But Poland has complained of “double standards” because the scheme exempts German coal plants from environmental standards, including the upcoming CO2 emission limits that are currently being discussed as part of the ongoing reform of the EU’s electricity market. Another article on the same website suggests the Commission considers capacity mechanisms to be “state aid” and, “ultimately, Brussels wants to phase them out completely” as they “distort the market and subsidise the most polluting form of electricity.”

In the US, the independent market monitor’s (Monitoring Analytics) State of the market report for the first quarter of 2019 lists the subsidy proceedings going on and noted the significant effect state subsidies would have on the operation of the PJM market.

The issue of external subsidies, particularly for economic nuclear power plants, emerged more fully in 2017 and 2018 and the first three months of 2019. The subsidies are not part of the PJM market design but nonetheless threaten the foundations of the PJM Capacity Market as well as the competitiveness of PJM markets overall.

The Ohio subsidy proceedings, the Illinois ZEC legislation to subsidize the Quad Cities nuclear power plant, the request in Pennsylvania to subsidize the Three Mile Island and other nuclear power plants, the New Jersey legislation to subsidize the Salem and Hope Creek nuclear power plants, the potential U.S. DOE proposal to subsidize coal and nuclear power plants, and the request by FirstEnergy to the U.S. DOE for subsidies consistent with the DOE Grid Resilience Proposal, all originate from the fact that competitive markets result in the exit of uneconomic and uncompetitive generating units. Regardless of the specific rationales offered by unit owners, the proposed solution for all such generating units has been to provide out of market subsidies in order to retain such units. The proposed solution in all cases ignores the opportunity cost of subsidizing uneconomic units, which is the displacement of new resources and technologies that would otherwise be economic. These subsidies are not accurately characterized as state subsidies. These subsidies were all requested by the owners of specific uneconomic generating units in order to improve the profitability of those specific units. These subsidies were not requested to accomplish broader social goals. Broader social goals can all be met with market-based mechanisms available to all market participants on a competitive basis and without discrimination.

In late July, PJM cancelled its 2019 capacity auction after FERC refused to make the changes PJM proposed to the rules for the capacity market to account for state subsidies.

Conclusion

Because of the high cost of non-supply and storage, electricity markets are justifiably concerned about the coordination of investment, contracting and operational decisions to achieve satisfactory levels of reliable supply. This paper notes the two well-tested (quantity and price driven) approaches electricity markets have taken to achieve adequate levels of reliability. It argues that both approaches are sufficiently similar that they both attract the same criticisms and are often dragged into confused debates that misunderstand the underlying problem.

Reliability problems in electricity markets across the world today are increasingly linked to the speed of transition to a low emission generation mix. This technology-driven transition is being led by choices made by market participants, businesses and consumers to invest in renewable energy resources. These choices are influenced by each decision maker’s appetite for change (capital risk/reward) and the price signals in the spot market, but are also increasingly driven by the incentives inserted into markets by government emissions reduction policies.

These choices change the supply and demand balance in the market. They affect the retirement of thermal generation and consequently change the reliability of supply experienced by consumers.

The choice of market design has little influence over the impact of policies and costs. Markets will reflect the costs flowing from consumer choices and government policies. The global debate today is exploring more effective and less costly options in which governments coordinate and size emissions policies that encourage a pace of change that both supports market-led investment responses to reliability concerns and minimises the amount of central intervention required to then slow it (eg delay thermal retirement).