Rainer Korte, Commissioner

Data Power series

28 April 2026 - The Wheeler Centre, Melbourne

29 April 2026 - Greenhouse, Sydney

Good morning. Thank you to The Energy for inviting me to this important conversation.

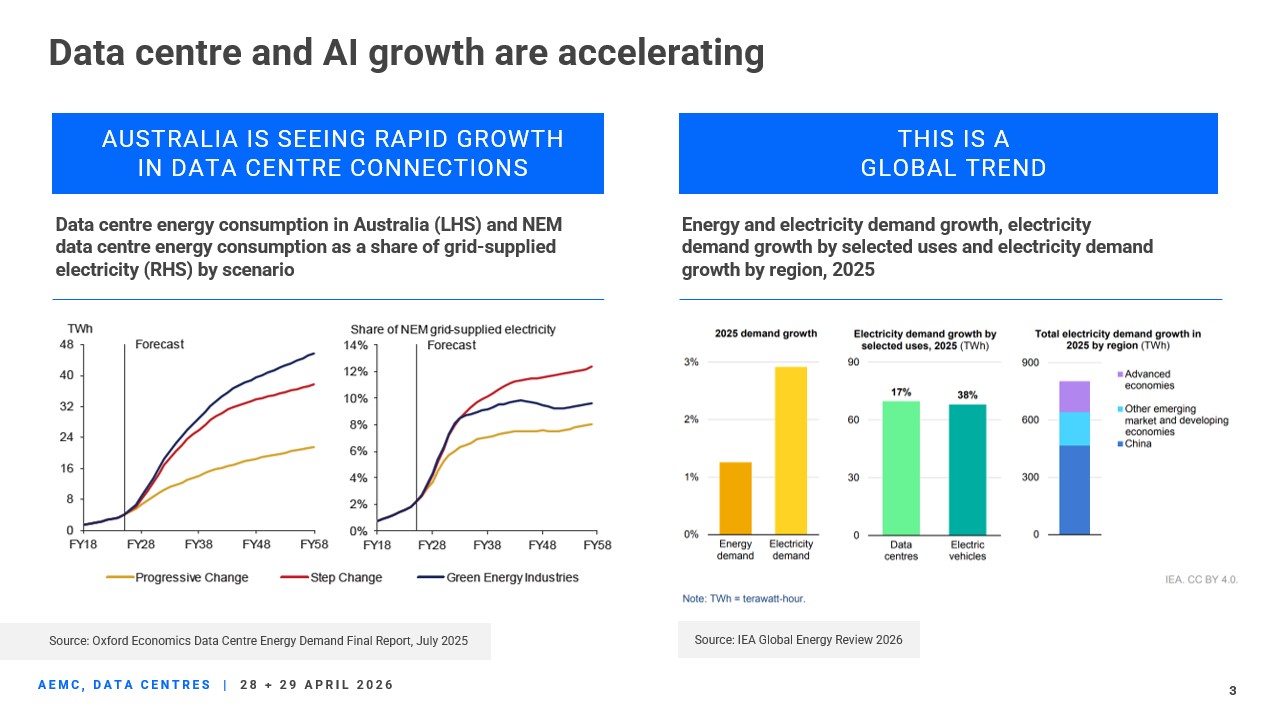

Australia is at a pivotal moment in its energy and digital transformation.

The energy transition is driving electricity demand growth through electrification and unprecedented levels of investment in renewable generation.

The digital transition is driving rapid growth in data centres and AI infrastructure, which have become among the fastest-growing components of electricity demand.

That brings enormous upside: jobs, productivity, and a stronger digital economy.

But it also brings a very real challenge. If large loads aren't planned and integrated well, the consequences land squarely on the power system and its security, and ultimately on consumer bills.

So, the question for us at the Australian Energy Market Commission (AEMC), and across government and industry, is simple:

How do we enable this investment without compromising affordability or system security?

Today I'll cover three things:

- first, I will briefly discuss how governments are responding to the opportunities and risks that come with increasing data centre connections;

- second, how data centre growth is impacting the technical parameters of our power system and introducing new challenges, and;

- third, what we are doing at the AEMC to ensure the regulatory framework supports connecting this new demand efficiently and securely.

National expectations are setting the direction

The Commonwealth has set a clear direction through the release of its National AI Plan and key expectations (on the screen), stating that this digital infrastructure must serve the national interest and integrate responsibly into the energy system.

For us in the electricity industry, those themes translate into three expectations for data centres:

- bring new clean energy

- be flexible in how you use power, and

- pay your way when connecting to the grid.

This is where the opportunity comes in.

Because when data centres meet these expectations, they don't just avoid harm; they actively support the system by underwriting new generation, shaping demand more efficiently and reducing pressure on shared network costs.

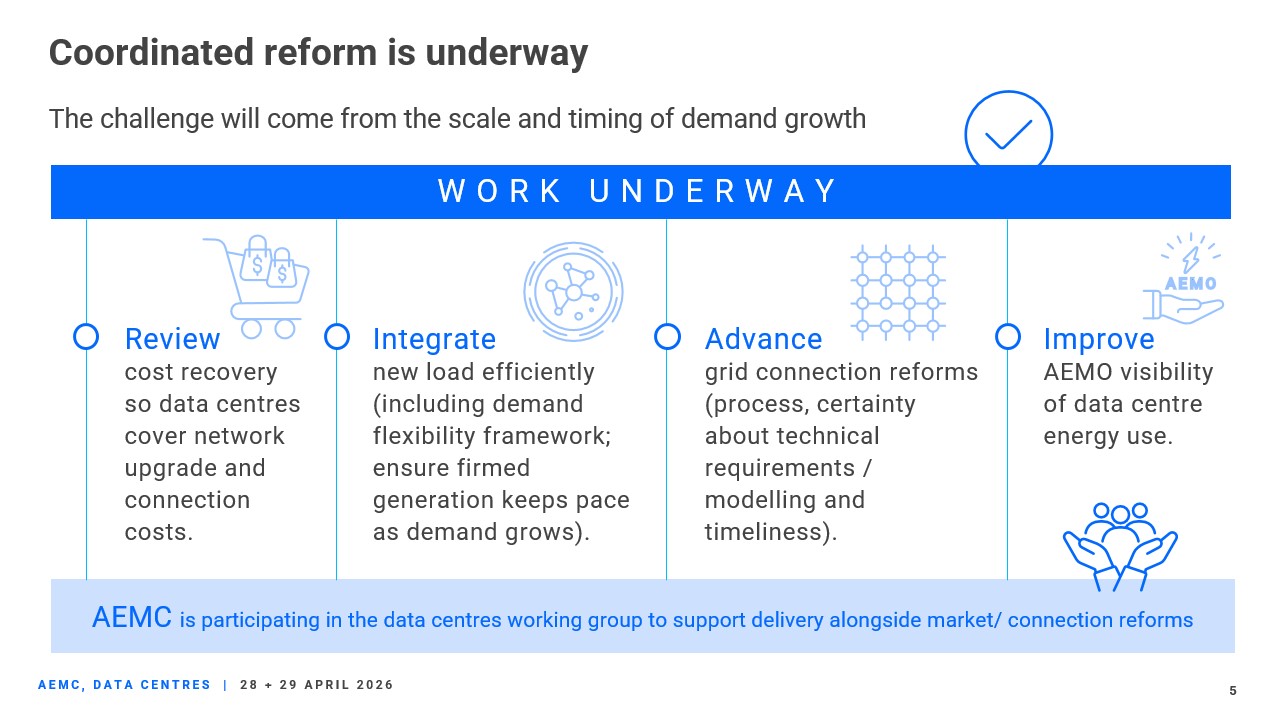

The AEMC, the Australian Energy Market Operator (AEMO), and the Australian Energy Regulator (AER) are working with governments to examine the impacts of data centre growth.

The reform agenda is focusing on:

- ensuring new loads fund their own network connections and augmentations

- integrating demand efficiently, particularly through flexibility and firming

- improving connection processes and technical certainty, and

- increasing operational visibility of large loads.

At the AEMC, we're contributing to this work, particularly where it intersects with connection standards and system security.

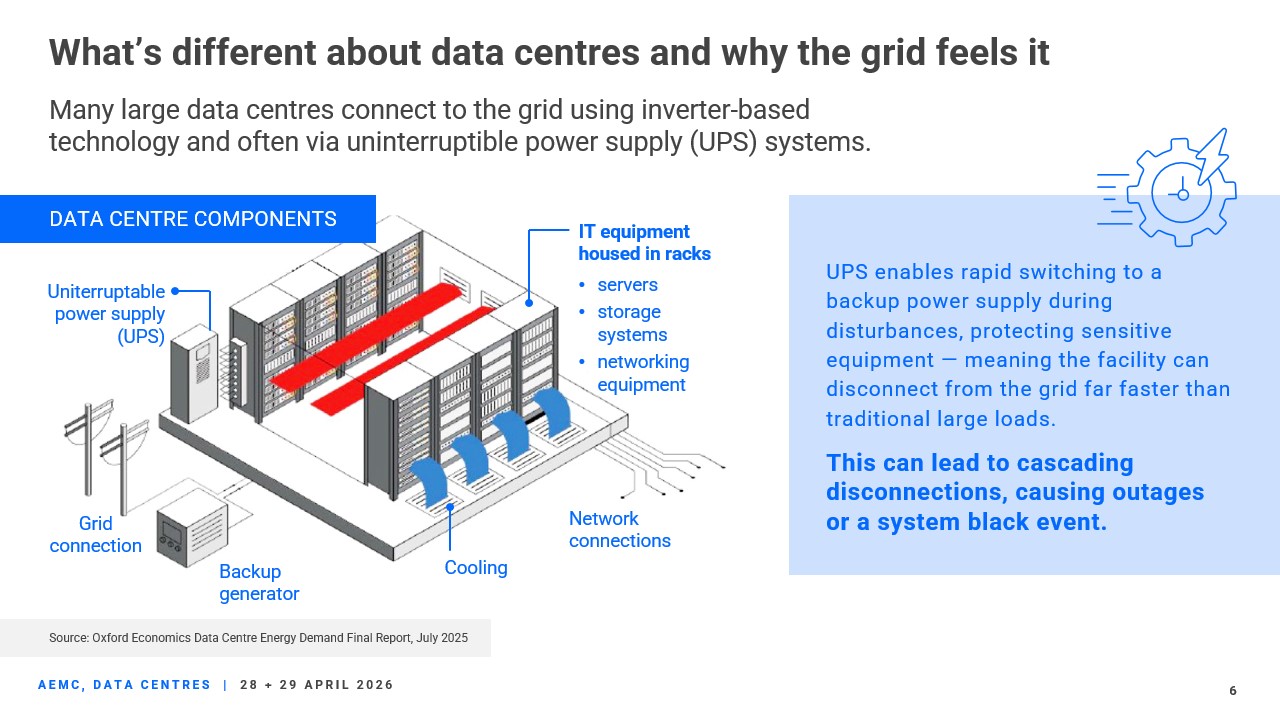

What's different about data centres and why the grid feels it

This brings me to the second item I want to discuss today: how data centre growth is impacting the technical parameters of the power system and introducing new challenges.

We are quickly learning, both here and overseas, that data centres differ from traditional large loads in important ways. They are:

- fast-growing and can be geographically concentrated

- more uncertain in timing and scale, and

- deeply integrated with inverter-based technology.

Many connect through inverter-based systems, like Uninterruptible Power Supply (UPS) infrastructure. That means their response to disturbances can more closely resemble that of a generator than that of a traditional industrial load.

Unlike traditional loads, which tend to have simple, predictable control systems, data centres can quickly disconnect from the grid during a credible disturbance to protect their sensitive equipment.

If multiple large loads disconnect at once, this can amplify frequency and voltage disturbances, trigger cascading events and risk system security.

We've already seen this in the US.

"Data Centre Alley" in Northern Virginia is one of the largest concentrations of data centres in the world. There, we saw how thousands of megawatts of data centres disconnecting in milliseconds can turn a routine disturbance into a major system event. This occurred because data centres connected at scale before their behaviour was well understood and factored into grid planning and operations.

We have also seen the rapid, concentrated growth of data centre connections in Ireland place significant strain on the grid. This created system-wide impacts that were not fully anticipated. In 2021, Ireland took the significant step of introducing a moratorium on new data centre connections until operational, planning and regulatory responses caught up. Roughly three years later, they lifted the moratorium and introduced significant regulatory reforms.

In Australia, we are learning from these international examples and acting now to better manage the risks. And better leverage the opportunities.

Because the very technologies that enable rapid disconnection of data centres can also enable system benefits, including:

- fast, flexible demand response

- participation in essential system services, and

- more dynamic interaction with the grid.

So, the question is not just about how we can best design regulations to minimise risk. It's also about how regulatory responses can unlock and harness data centre technical capabilities to support the power system and energy transition.

AEMC regulatory response

This is exactly the challenge the AEMC is addressing.

The AEMC released a draft determination on improving access standards for large loads in March this year.

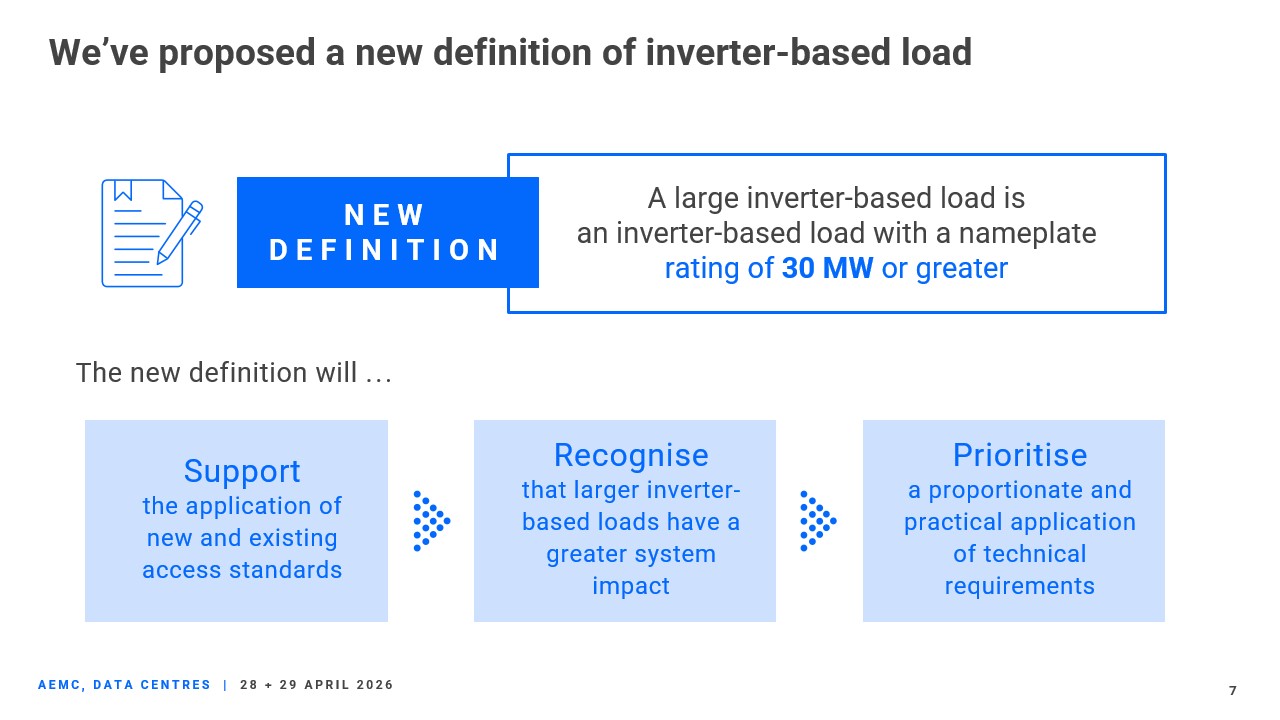

The Commission's central message is that the existing access standards are not well-suited to the technical characteristics or scale of large inverter-based loads, like data centres. As a result, the draft rule proposes updating and introducing new access standards that reflect modern system needs, while still supporting efficient investment and innovation.

To support the application of new and existing standards, the draft rule seeks to clearly define inverter-based loads in the National Electricity Rules (NER).

This is important because their technical performance differs from that of other loads, and they require different regulation under the NER.

A clear regulatory framework

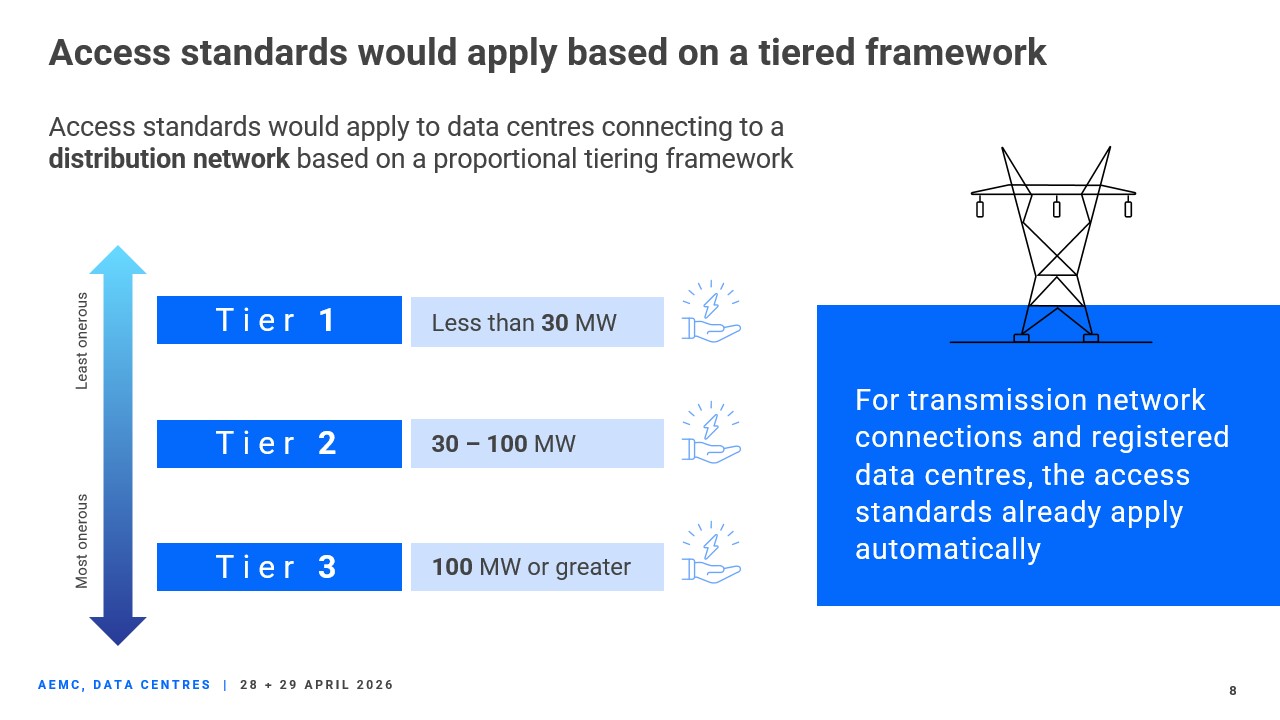

The draft rule also introduces a clear and transparent framework for classifying inverter-based loads.

This is important for connections to distribution networks where we are increasingly seeing significant new demand, including from data centres.

While access standards already apply to inverter-based loads connecting at the transmission level, and to those that choose to register in the market, there has been no consistent framework for large, non-registered loads connecting at the distribution level.

The draft rule introduces a three-tiered classification framework.

The intent here is proportionality. Not every load has the same impact on the power system. The connection standards applied to small loads should not be the same as those applied to larger loads that pose a greater risk to system security.

The proposed framework also addresses a growing issue in the NEM: AEMO has limited visibility of non-registered large inverter-based loads connecting at the distribution level, making it harder to plan and operate the system securely as their numbers grow.

Without a clear, fit-for-purpose definition of what constitutes a large inverter-based load, connection applicants, network service providers and system planners are left with uncertainty — about when technical requirements apply and how to design networks that remain secure as these loads increase. Providing that clarity is therefore a central objective of this rule change.

It is also important to understand that the proposed access standard reforms apply to data centres that connect directly via their UPS/inverter-based system. Where a data centre connects behind other plant, such as a battery, this is treated under the NER as an integrated resource system, for which different technical access standards apply.

The application of technical access standards for loads (schedule 5.3) and integrated resource systems (schedule 5.2) under the NER should not be duplicative.

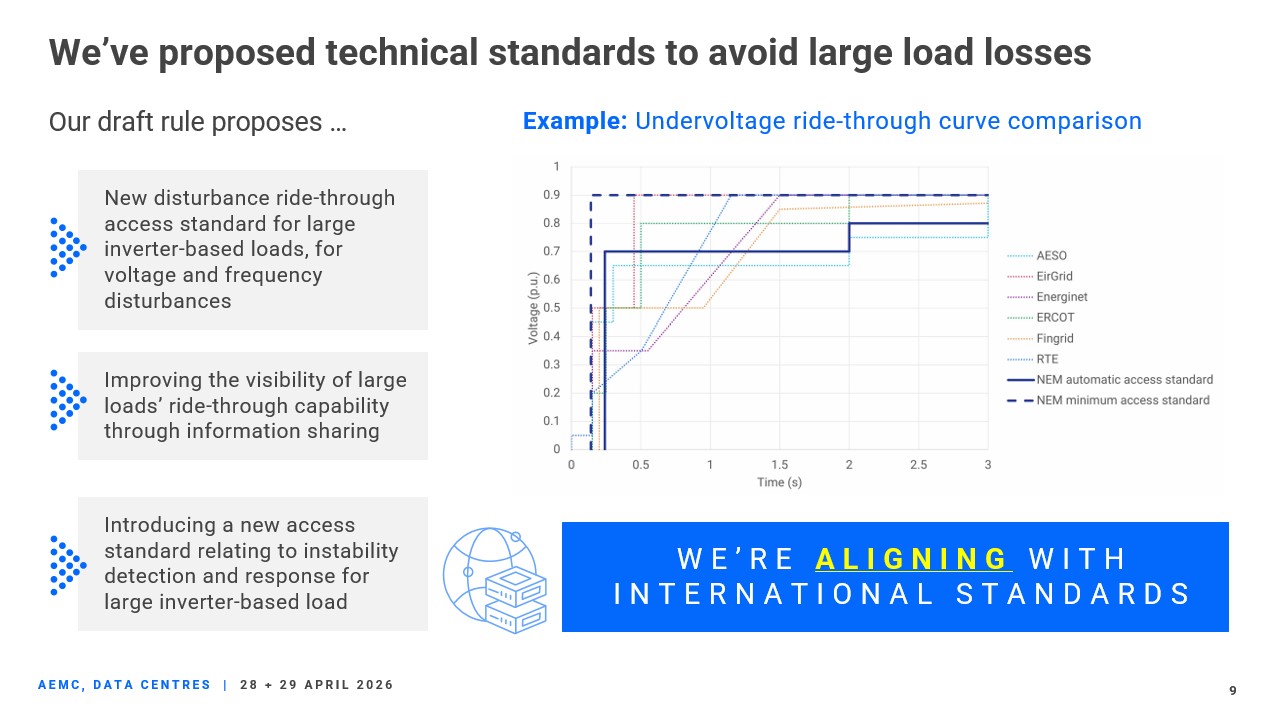

Ensuring power system security

Another key focus of the draft determination is strengthening and introducing new technical requirements. These cover how large loads, like data centres, respond to credible disturbances, such as voltage or frequency events. The objective is to ensure they can ride through these disturbances or disconnect in a controlled manner when necessary.

The intent is to reduce the risk that large loads exacerbate system events, particularly as their scale and concentration increase in parts of the network. We've learned from international experience that if we do not seek to reduce this risk, we could see cascading disconnections that result in outages, with the costs ultimately borne by consumers.

Importantly, the draft rule recognises that these changes should not unnecessarily deter investment. Instead, the framework is designed to provide upfront clarity, reduce negotiation uncertainty, and support timely connection processes.

Our approach is internationally aligned

The Commission has sought to align the proposed new access standards with those in comparable international jurisdictions.

This should enable investors to leverage feasibility studies, grid-integration assumptions, and risk models developed elsewhere, thereby reducing technical and regulatory incompatibilities that could deter investment in the NEM.

It should also enable investors to benefit from access to standardised OEM load equipment.

The objective is shorter procurement timeframes, reduced engineering hours, and lower equipment integration risk for the NEM. Those savings should flow directly into lower capex and faster commissioning for data centre developers, whilst ensuring system security is maintained.

Summary of draft rule discussion

In summary, to fully realise the benefits data centres can bring, we need clear and predictable connection processes. The draft rule is an important step towards that objective. By introducing a clearer classification framework and defined expectations for access standards, it reduces ambiguity in the connections process.

For network service providers, this provides greater upfront clarity on technical connection requirements. For connecting parties, it creates a more predictable pathway, providing earlier certainty about what is required and the likely costs.

The result should be more streamlined connections.

Importantly, the new disturbance ride-through access standards for large loads, improved visibility of ride-through capability, and a new access standard for instability detection will help maintain a secure power system.

The AEMC is currently consulting on the draft access standards rule, with submissions closing on 7 May.

We look forward to stakeholder submissions and will continue working closely with industry to refine the final design.

Call to action

So, where does this leave us?

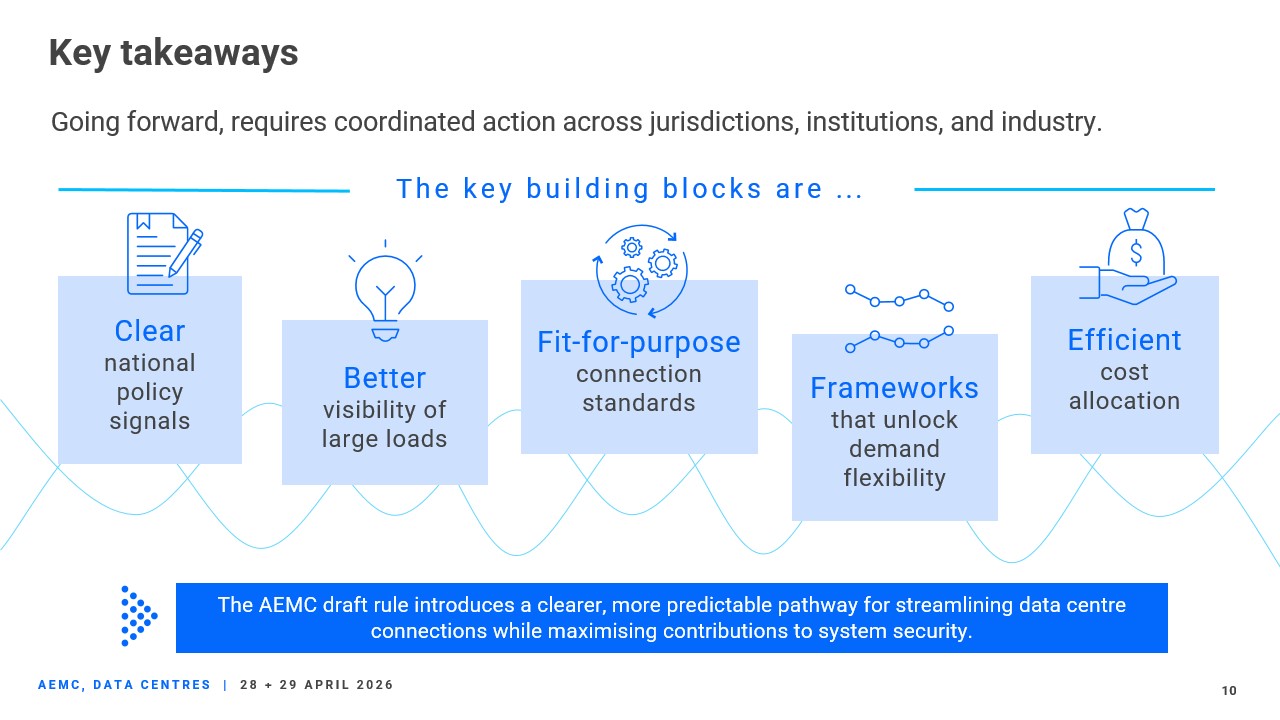

The path forward is clear, but it requires coordination:

Across jurisdictions. Across institutions. And across industry.

The key building blocks are:

- clear national policy signals

- fit-for-purpose connection standards

- efficient cost allocation

- better visibility of large loads, and

- frameworks that unlock demand flexibility.

If we get this right, the prize is significant.

We can enable the digital AI investment and economic growth Australia will benefit from, while keeping the system secure and affordable.

Ultimately, this is not a choice between digital growth and energy security. It's about designing a system where each strengthens the other.

If we align policy, regulation and networks effectively, data centres won't just be integrated into the grid, they will help power its future.

Thank you.