Rainer Korte, Commissioner

CEDA Energy Security Series

26 February 2026 - Pullman, King George Square, Brisbane

I would like to thank CEDA for the opportunity to speak with you today.

And I would like to acknowledge the traditional owners of the land on which we meet today – the Turrbal and Yuggera people – and pay my respects to Elders past and present.

When was the last time a blackout hit your neighbourhood?

The lights go out. The washing machine stops … and oh no! The Wi-Fi drops out.

Disaster.

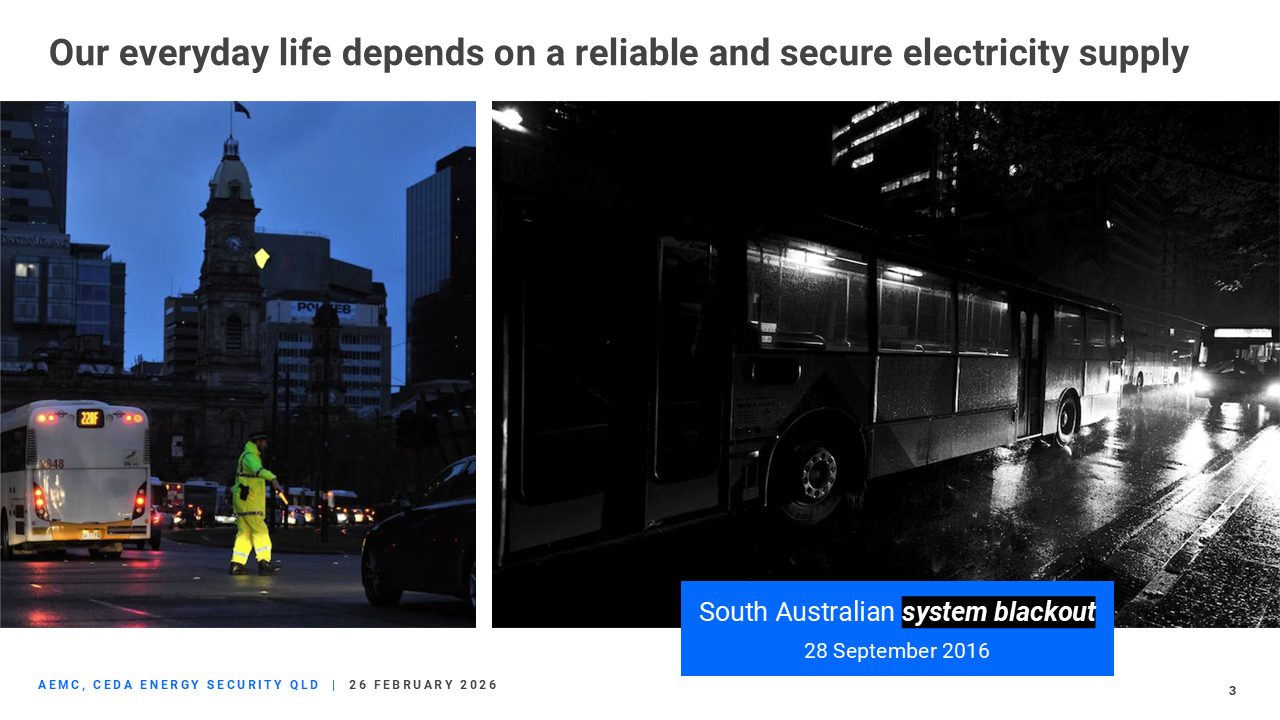

You are suddenly reminded of how much your everyday life depends on a constant and reliable supply of electricity.

Yet how often do you really think about it?

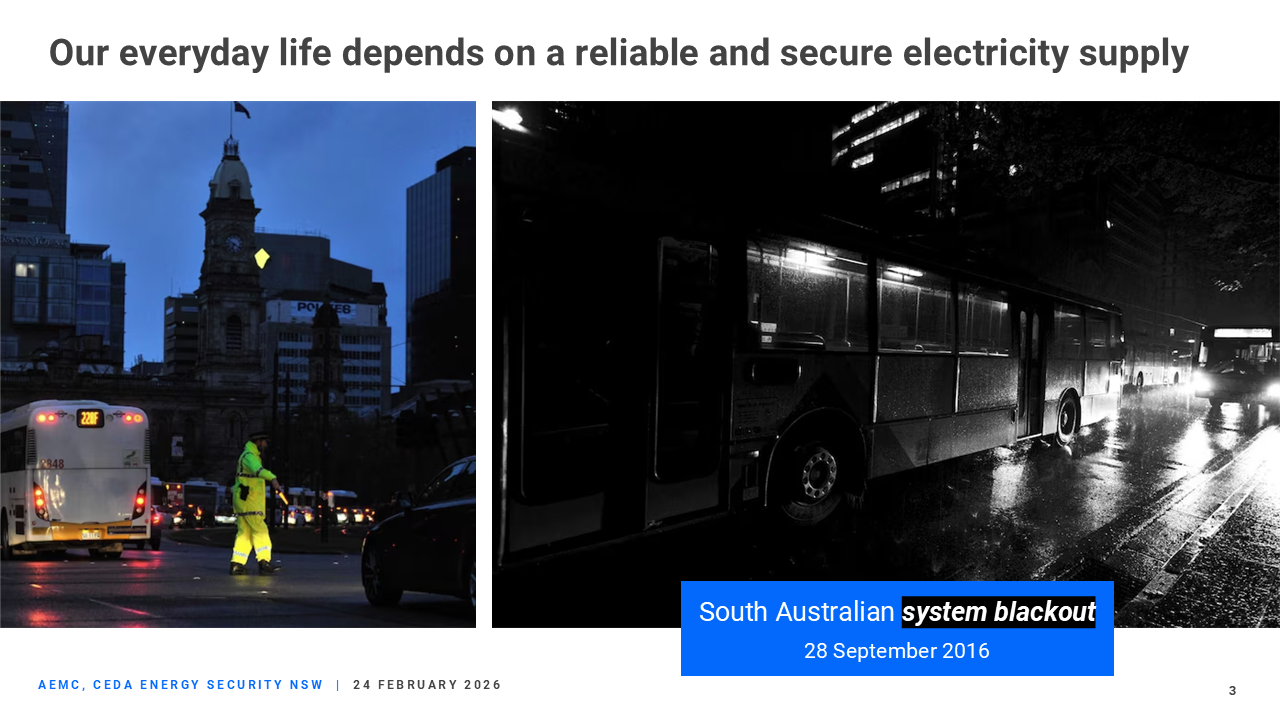

Recently, on Australia Day, I experienced a power blackout at home … ironically, while I was preparing for this talk. It was an exceptionally hot, record-breaking evening in Adelaide — over 40 degrees. The power was out for about 4 hours due to a fault on the distribution network.

Household or neighbourhood blackouts can be frustrating and annoying, and even life-threatening for some people in our community. Usually, these are fixed quickly. But on a larger scale, blackouts can have much more serious social and economic consequences. It's more than a few hours without Wi-Fi.

I lived through the South Australian statewide blackout in September 2016 and the subsequent investigations.

Fortunately, in that case, approximately 80–90% of the metropolitan and suburban supply was restored within eight hours. However, regional supplies took up to a week to restore. The blackout is reported to have caused economic losses of $450 to $500 million.

Blackouts remind us that energy security is essential for business continuity, economic prosperity, and safety. It underpins our way of life.

As you know, Australia is in the middle of the biggest structural transformation of our energy system in a century.

During the transformation, we are trying to keep the lights on, keep bills manageable, and cut carbon emissions – all at the same time. It's not easy!

At the Australian Energy Market Commission (AEMC), we are doing our part to address these challenges by implementing practical rule changes and providing sound advice to policymakers in line with our vision for a consumer-focused net zero energy system.

So, where are we up to in ensuring the lights do stay on through the energy transition?

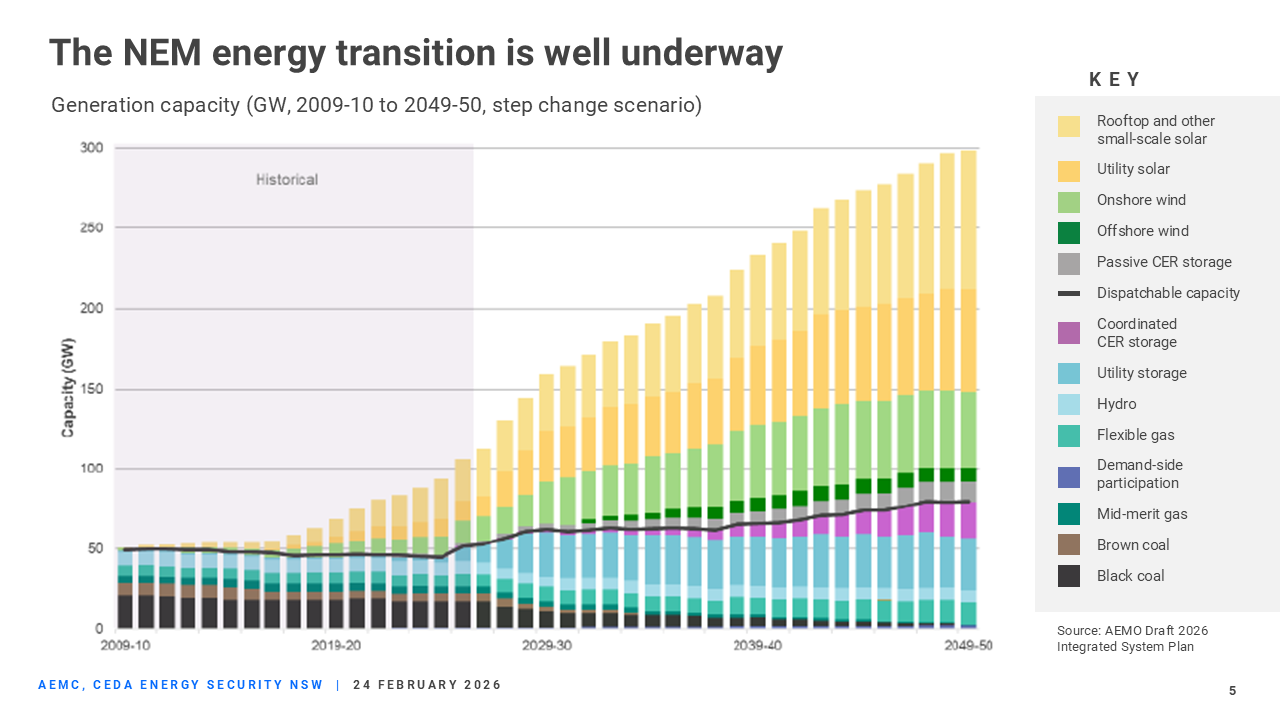

The energy transition is well underway

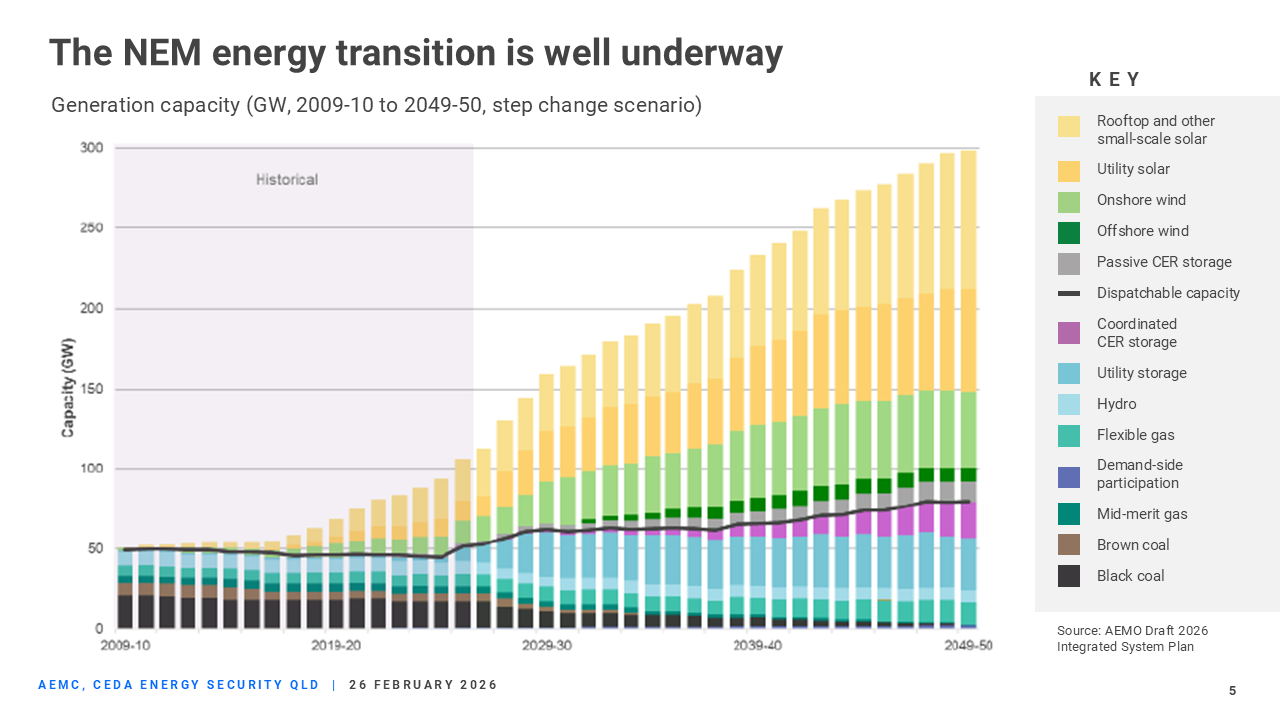

In the National Electricity Market (NEM), the energy transition is well underway.

Australia is increasingly relying on grid-scale and consumer renewable energy sources.

At the same time, our ageing coal fleet is retiring.

Electricity demand is rising — driven by the electrification of industry, homes, and transport, and the growth of new energy-intensive industries, such as data centres.

Altogether, electricity consumption in the NEM is forecast to nearly double by 2050.

In December 2025, the Australian Energy Market Operator (AEMO) released its Draft 2026 Integrated System Plan (ISP). It reaffirms that renewable energy generation, connected by transmission and distribution, firmed with storage, and backed up by gas-powered generation, is the least-cost way forward for Australia.

The ISP Optimal Development Path (ODP) sets out the least-cost mix of grid-scale resources needed to replace retiring coal plants, accommodate the near-doubling of electricity demand, and meet government renewable energy and emissions targets, while accounting for the estimated growth in consumer energy resources (CER).

Under the central 'step-change' scenario, the Draft ISP projects the need for:

- A fivefold increase in grid-scale wind and solar by 2050

- A fourfold increase in distributed solar PV – noting that 1 in 3 households already have solar panels

- An 18-fold increase in storage capacity

- More flexible gas-powered generation to provide back-up power when needed

- An additional 6,000 km of transmission

The scale of investment required is huge. The annualised capital cost of the utility-scale generation, storage, transmission, and distribution infrastructure is estimated at $128 billion by 2050.

Significant momentum is underway to deliver these investments, but challenges remain in doing so quickly enough.

Projects face delays due to protracted planning decisions and approvals, navigating supply chain constraints, securing social licence, and construction delays.

A key finding of the AEMC's latest Residential Electricity Price Trends report is that energy prices risk rising unless new renewable generation, battery storage and transmission projects are delivered faster than currently projected.

Government policies, such as the New South Wales Electricity Infrastructure Roadmap, are being implemented to ensure sufficient grid-scale infrastructure is in place before coal plant retirements, thereby reducing reliability and system security risk.

In addition to providing a roadmap for the NEM energy transition, the ISP informs regulatory processes and jurisdictional planning programs.

The AEMC is conducting a review of the ISP framework in 2026 to ensure it remains fit for purpose and continues to guide billions of dollars in investment decisions with confidence.

Maintaining reliability and system security is critical

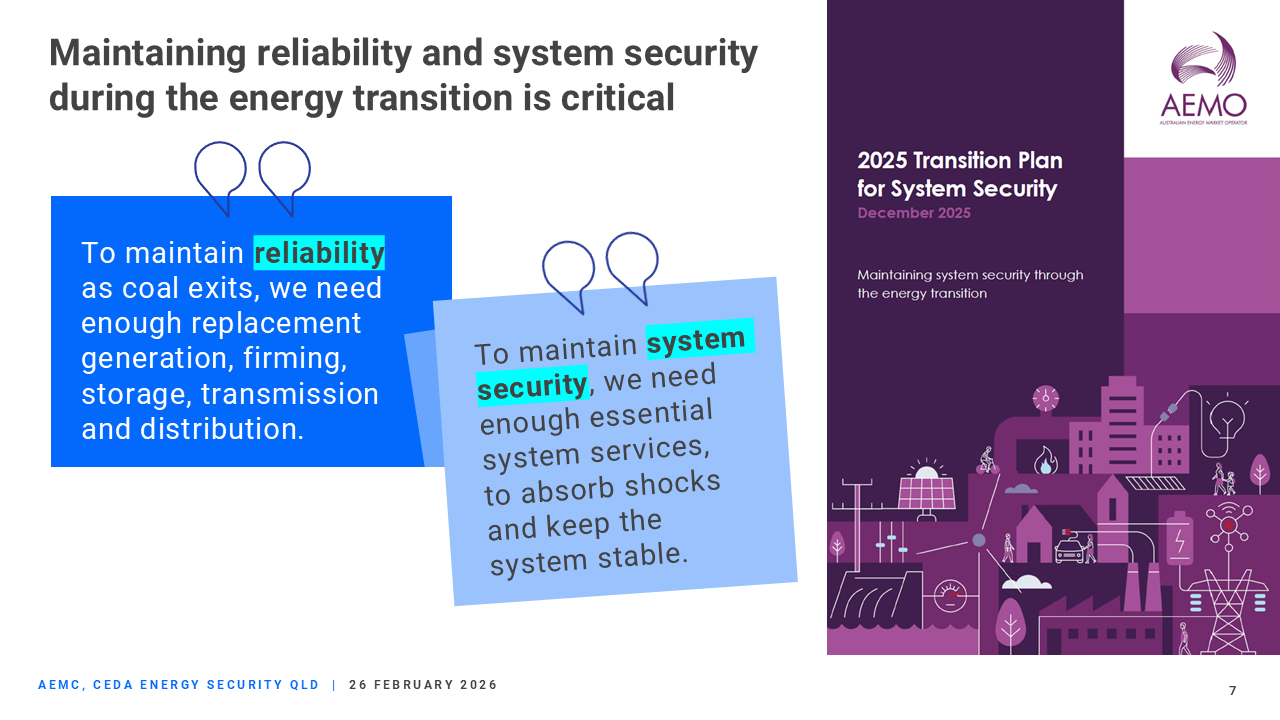

Maintaining reliability and system security during the energy transition is critical.

As coal exits, we need enough replacement generation, firming, storage, transmission and distribution to maintain reliability.

To be secure, the power system must operate safely within its defined technical limits, withstand disturbances, and restart after a widespread outage, such as a statewide blackout.

To maintain system security, we need enough essential system services, such as inertia and system strength, to absorb shocks and keep the system stable.

Early investment in replacement resources is essential to mitigate the impacts of coal closures.

AEMO's Transition Plan for System Security, released in December, identifies emerging security gaps that require coordinated action by AEMO, governments, networks, and market participants to support the energy transition over the next 10 years.

The plan highlights one major unresolved issue for Queensland: managing system security under low-probability minimum system demand conditions. Implementing emergency backstop mechanisms to actively manage smaller PV installations when needed can help to address this issue.

Recent major reforms of the National Electricity Rules system security frameworks continue to be implemented and evolve.

The AEMC has received two rule-change proposals to enhance the existing frameworks.

AEMO has proposed options to enable system strength and inertia shortfalls to be declared and managed more effectively, improve planning certainty, and adjust regulatory timeframes to better align resource entry and exit.

The Australian Energy Council (AEC) and the Clean Energy Council (CEC) are seeking improved clarity and transparency in the security frameworks.

We plan to commence these rule changes next month.

AEMO is progressing the implementation of new transitional services introduced under recent regulatory reforms to support operability and help trial new technologies such as battery grid-forming (GFM) inverters to deliver essential system security services.

These new investments and reforms are needed to maintain system security ahead of coal exits.

Undertaking strategic investments ahead of time to ensure the grid is ready for what's coming is better than trying to invest "just in time", as every delay increases risk to reliability and system security.

Consumer energy resources cut energy costs and improve resilience

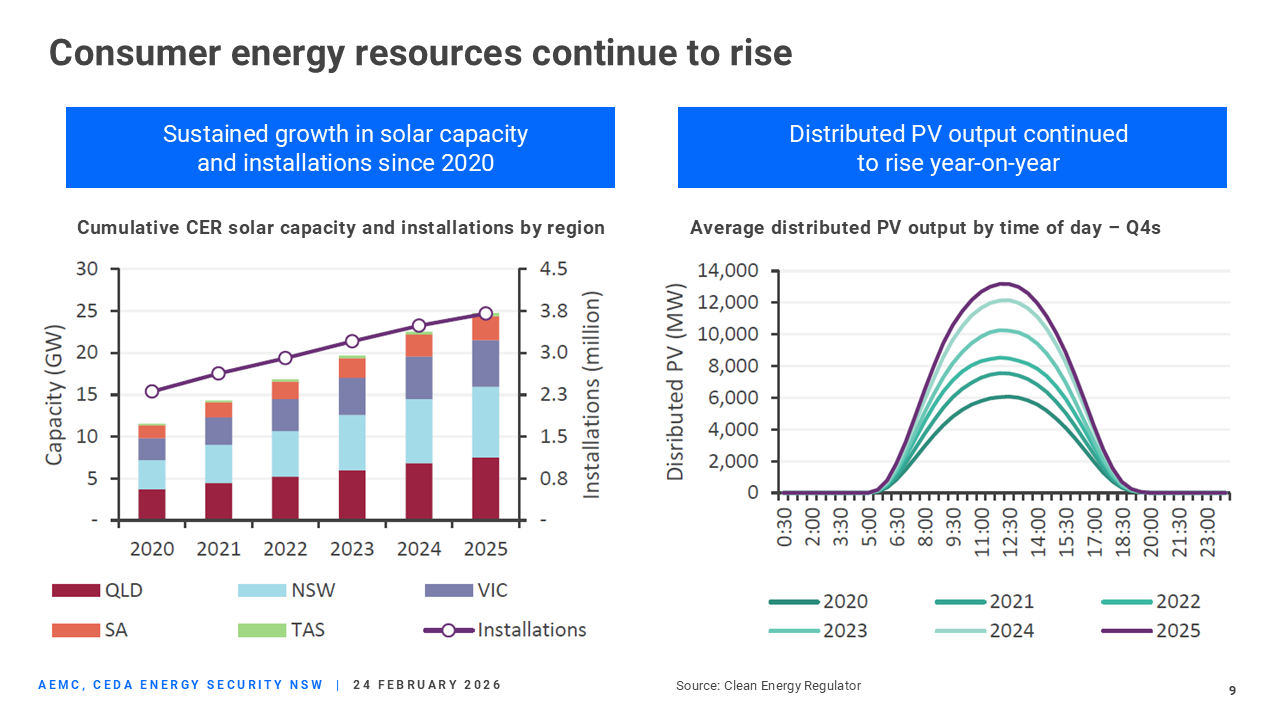

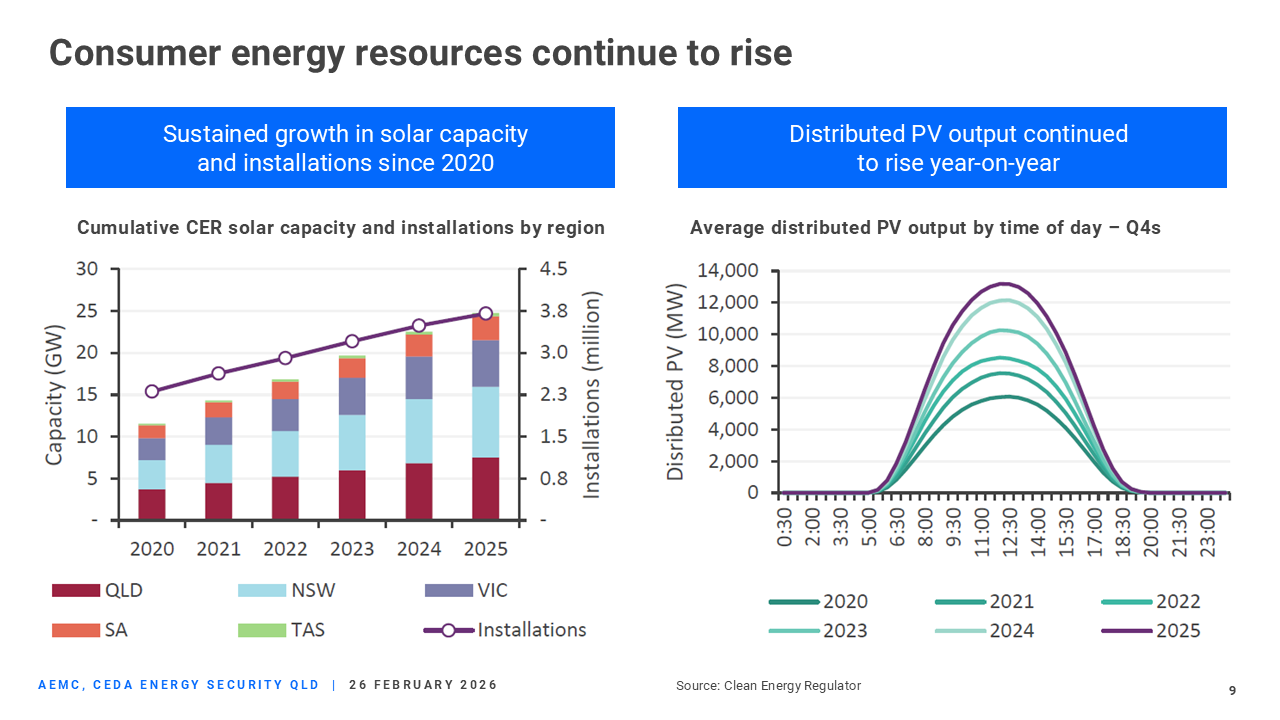

One of the most exciting – and challenging – parts of the energy transition is the rise of CER.

Rooftop solar. Home batteries. Electric vehicles. Smart appliances.

Queensland is approaching 1.2 million rooftop solar installations.

The opportunity is enormous:

- Households and businesses can lower bills by actively managing their home energy needs.

- Local communities can build resilience through microgrids and backup capability.

- Thousands of devices can be orchestrated to act as a virtual power plant.

- The need for expensive centralised infrastructure can be reduced.

But there are also significant challenges:

- Minimum grid demand is falling to levels that complicate system security.

- Voltage and local network management have become more complex.

- System operators need visibility and a level of emergency control over millions of small devices.

- Market rules and incentives must evolve so CER leads to firmer aggregated capacity, not just unmanaged variability.

Australia is at the forefront of these challenges globally – there is no playbook for us to follow.

As CER uptake continues to grow, visibility and orchestration of CER resources become critical to maintaining system security and delivering the energy transition at the lowest cost.

CER owners benefit directly from their investments and help lower system costs for all consumers.

Well integrated, CER could deliver up to $45 billion in net present value savings in avoided investment by 2050. Having the right regulatory frameworks in place is essential to realise these benefits.

The AEMC has been working hard to achieve this goal. For example, a recent reform, the integrating price-responsive resources rule change, will enable resource aggregators to participate in the wholesale electricity market, reducing system costs.

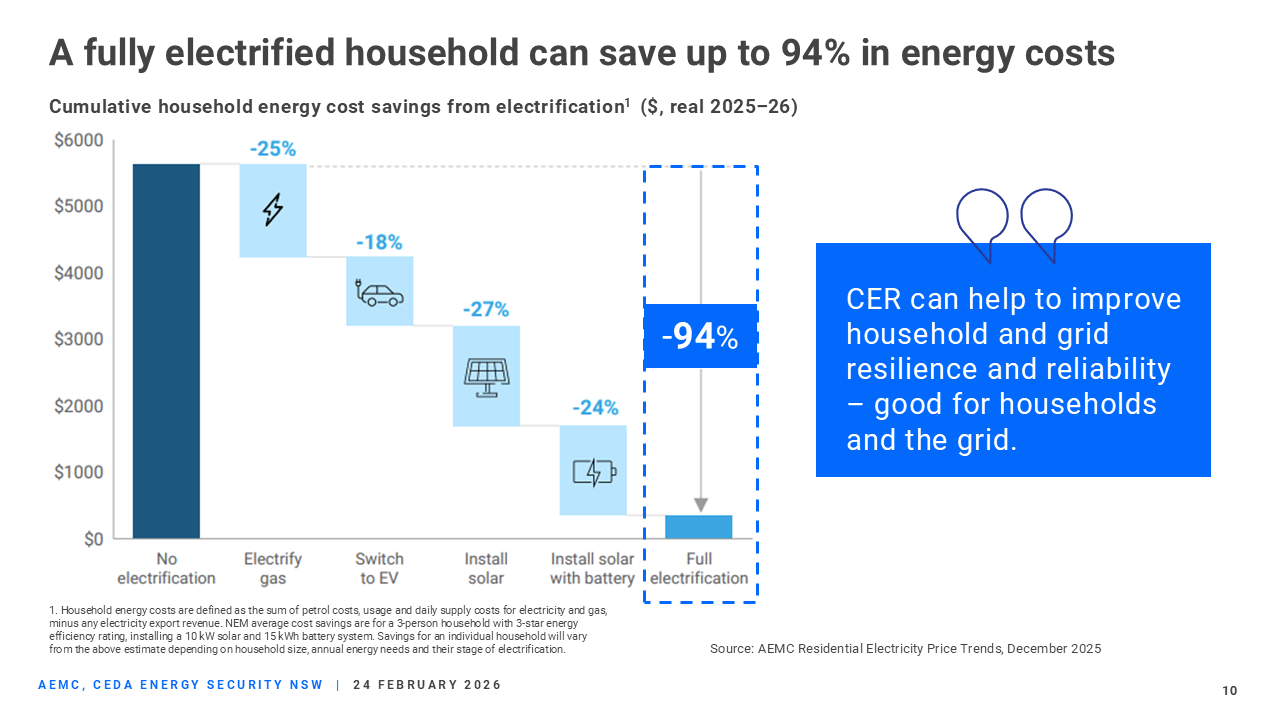

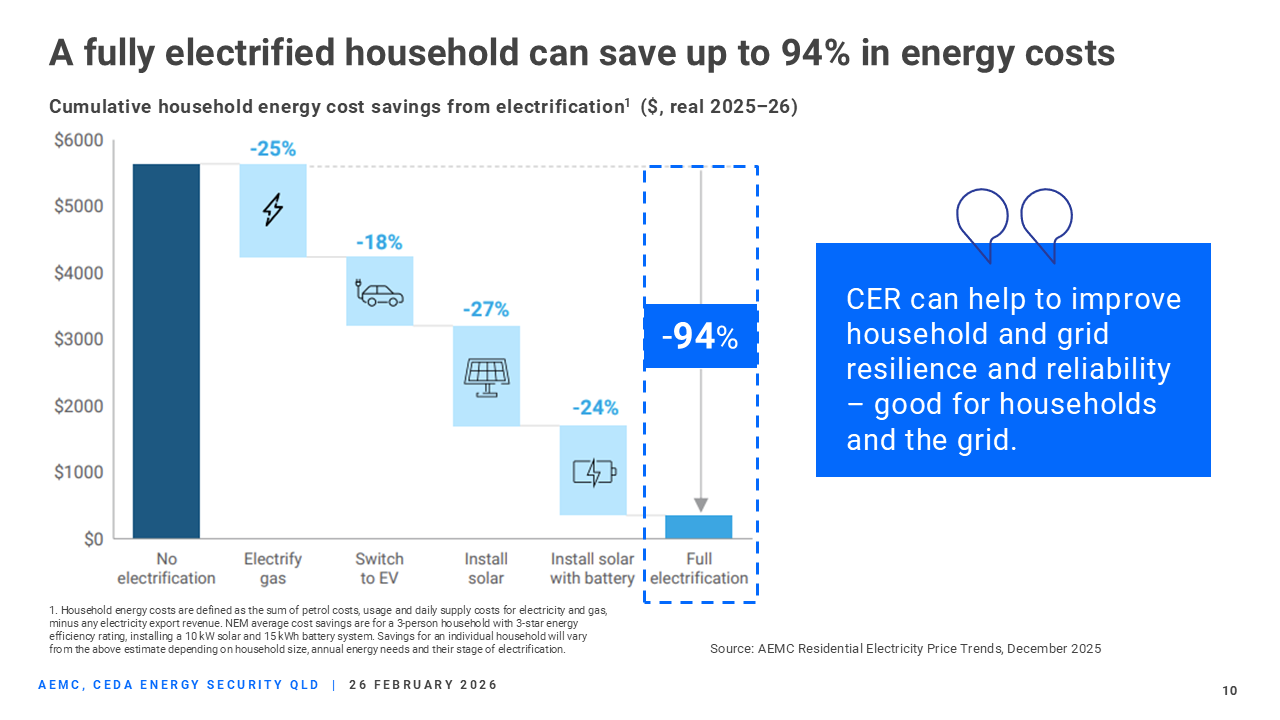

The AEMC's latest Residential Electricity Price Trends report shows that electrification is one of the most powerful tools that households have to cut their energy bills. Installing rooftop solar and a battery, switching to EVs, and replacing gas appliances with efficient electric ones can lower total household energy costs by up to 90 per cent per year.

CER can also help to improve household and grid resilience and reliability – so, good for households and the grid.

A fair energy transition

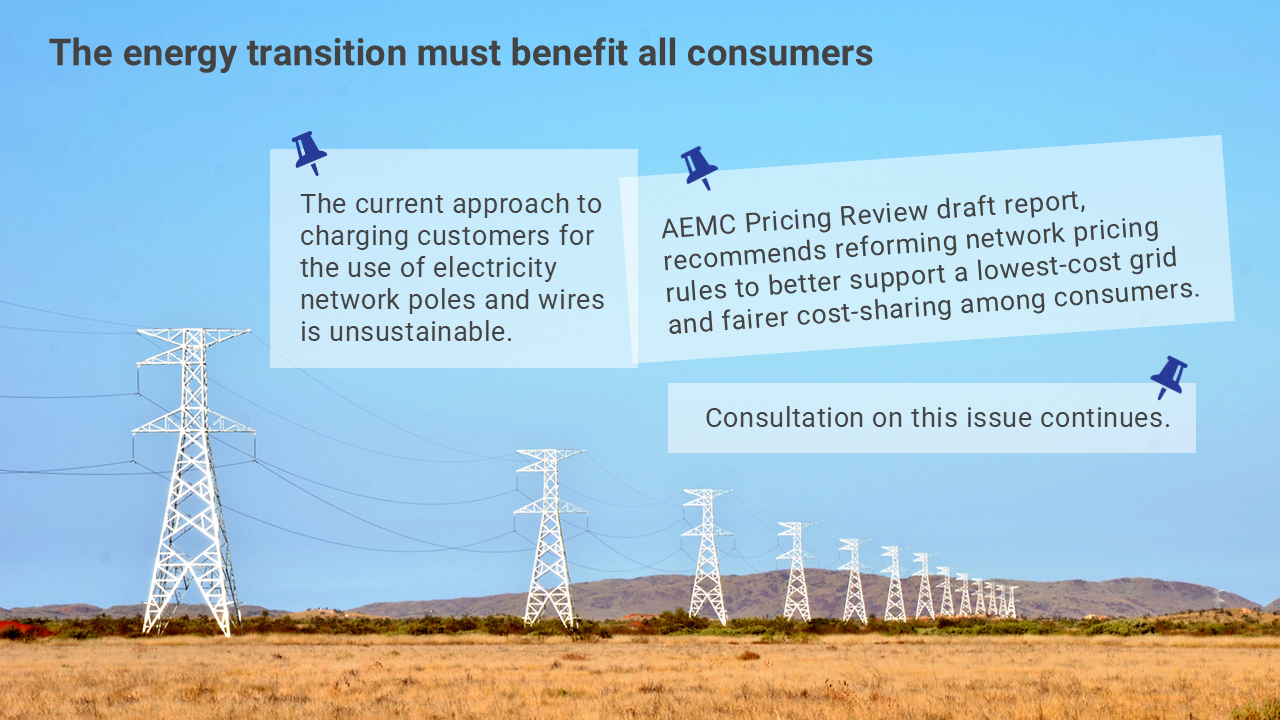

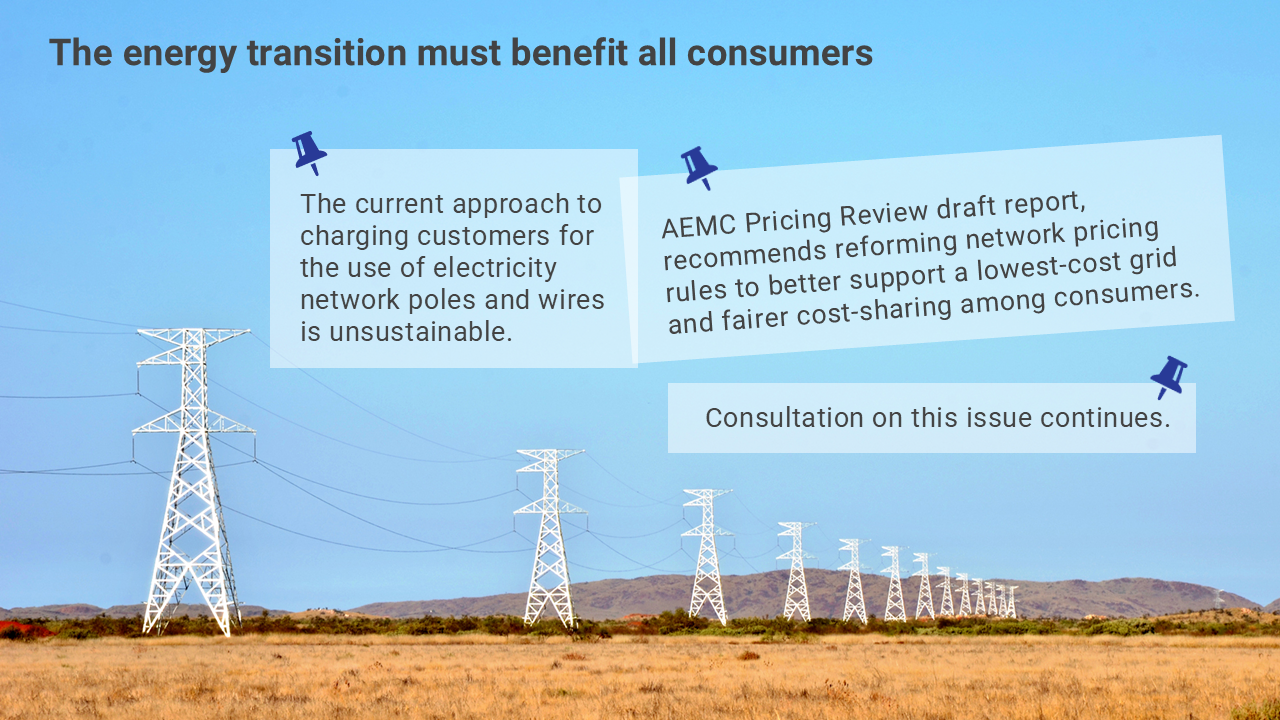

The energy transition must benefit all consumers.

The current approach to charging customers for the use of electricity network poles and wires is contributing to adverse outcomes for some customers amid rapid CER growth.

This is because network costs are largely recovered through usage charges, and when customers install solar and batteries, their grid electricity usage drops, along with their contribution to network costs. But the cost of the grid remains the same.

As this trend continues, a shrinking pool of customers without CER is left to pay a growing share of network costs.

How can this issue be addressed?

Currently, around 70 per cent of network costs are recovered via usage charges.

If fixed charges are raised to recover a greater proportion of network costs, all customers, including those with CER, would experience a relatively small increase.

However, if usage charges are raised instead, customers without CER that rely solely on the grid would pay much more, particularly those who can't shift usage away from high-demand times.

The current situation is unsustainable, and action is required to address rising equity concerns.

The AEMC Pricing Review draft report, released in December, recommends reforming network pricing rules to better support a lowest-cost grid and fairer cost-sharing among consumers.

A distributional analysis is currently underway to assess the impact of the proposed reforms across different customer types, and we also continue to engage with stakeholders to inform this important work.

Is the energy transition delivering?

So, is the energy transition delivering on the key indicators of reliability, cost, and sustainability?

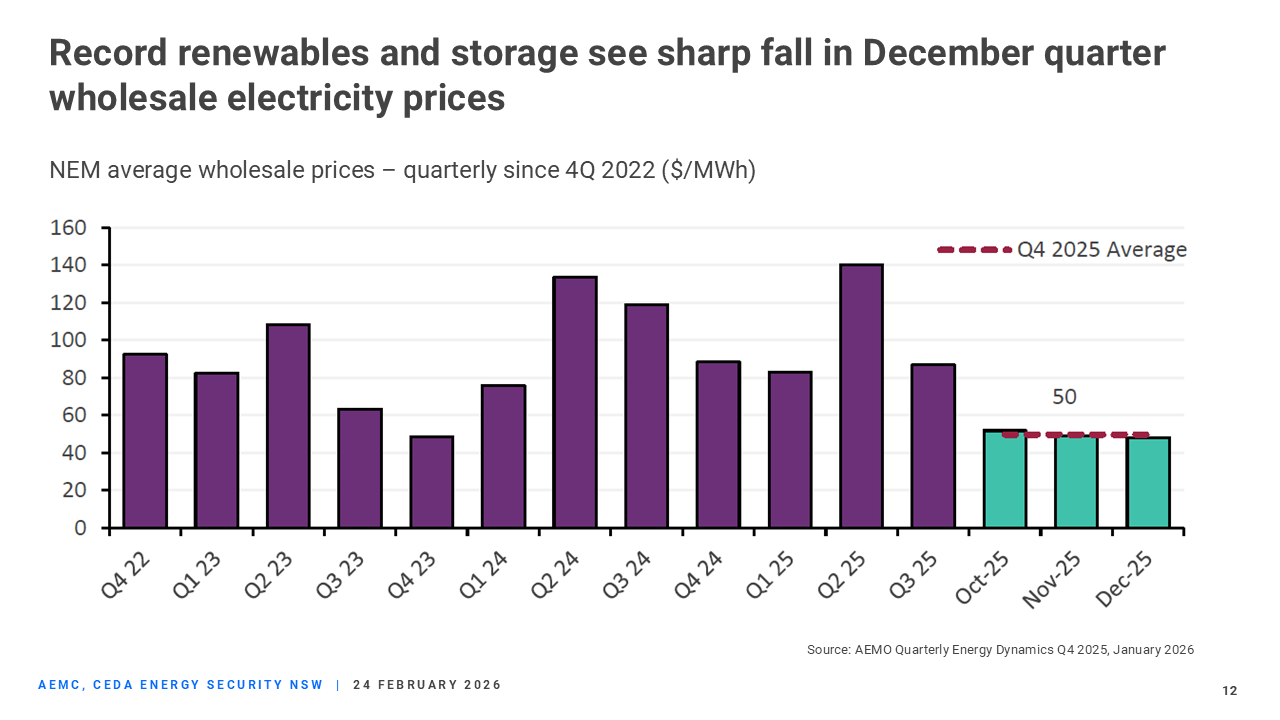

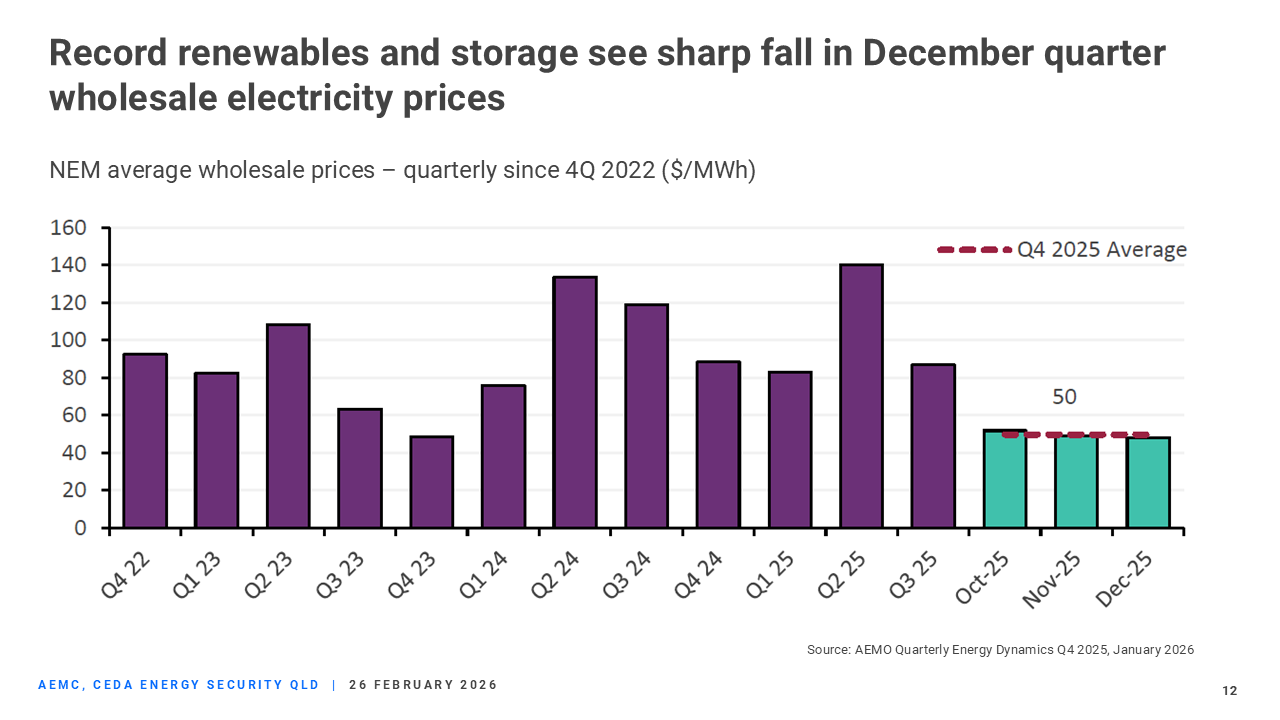

AEMO recently released its energy dynamics report for the December quarter of 2025.

The December quarter has been described as a "landmark moment", with wholesale electricity prices falling sharply, renewables meeting half of all NEM demand for the first time, battery output surging, and coal generation hitting a new low.

Average wholesale electricity prices nearly halved – compared to a year earlier – driven by record renewables and storage output.

Coal-fired generation was down 4.6 per cent year on year, falling to an all-time quarterly low. Gas-fired generation dropped 27 per cent to its lowest levels for 25 years.

These are positive signs that we are heading in the right direction on cost and sustainability.

What about energy security? Reliability and system security are tested under system stress: hot nights, low wind, high demand, or during major disturbances.

On Australia Day, South Australia endured a stress test during an unprecedented heatwave, including the hottest night ever recorded in Adelaide. While there were local outages in the distribution network, such as the one impacting my household that I mentioned earlier, the system overall maintained reliability.

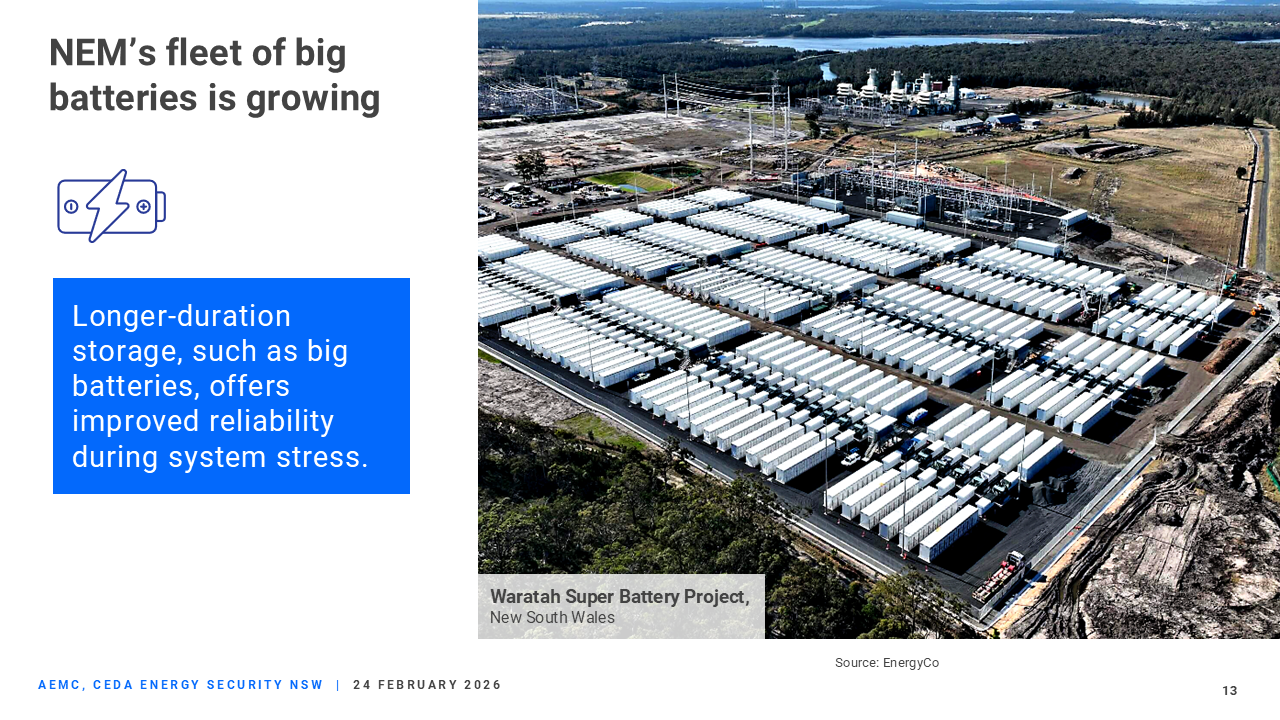

When the sun went down and batteries were discharged, peaking gas plants and diesel generators provided backup.

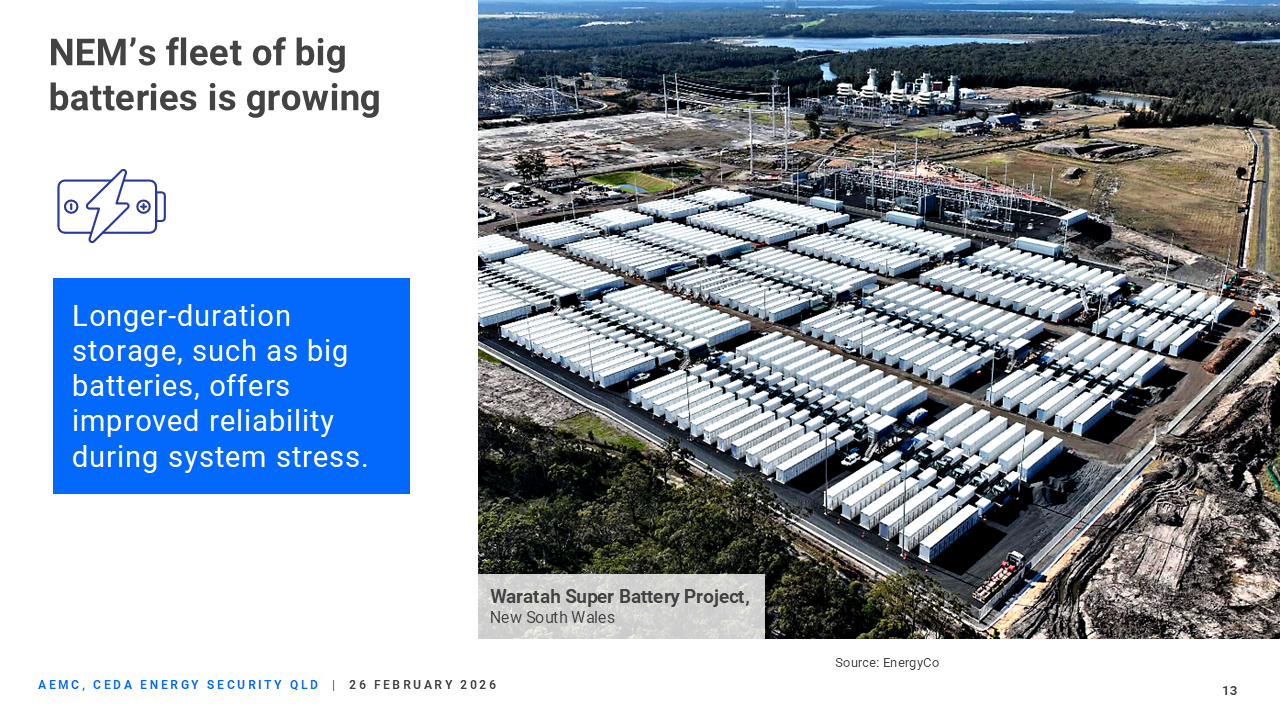

This highlights the need for more and longer-duration storage, as well as the value of the growing fleet of big battery projects underway in South Australia and across the NEM.

In 2025, Australia installed more battery storage per electricity consumption than any other country worldwide.

Recent big battery operational announcements in Queensland include the 250 MW and 500 MWh Swanbank Battery near Ipswich and the Stanwell 300 MW and 600 MWh Tarong Battery. Batteries such as these help drive down power prices by storing renewable energy for use during peak demand. They can also provide essential services to support system security.

The Australia Day stress test in South Australia also highlights the important role of gas-fired generation in supporting the energy transition.

South Australia is a global leader in integrating wind and solar, with an average share of about 75 per cent over the last year. Wind and solar generation regularly exceed 100% of electricity demand, with rooftop solar alone exceeding 100% on multiple occasions.

South Australia is demonstrating what a high-renewables-penetration grid looks like and that it can be operated to deliver the reliability and system security we expect.

So, we have a plan and are making real progress with the energy transition. Renewables are lifting their share, storage is scaling, and new essential system services are emerging. But we must accelerate investment, invest early, and maintain a clear line of sight to the essential system services that keep the system stable.

Energy security cannot be an afterthought — it is a key enabler of the energy transition.

Every reform, every investment, every rule change is ultimately about ensuring that Australians can rely on their energy system, no matter how hot the night, how high the demand, or how fast technology evolves.

The energy transition is challenging, but it is achievable. And if we get it right, we will deliver a system that is not only secure but also the lowest-cost, lowest-emissions, and equipped to support the industries and communities of the future.

Thank you.